Investing in Fintech Companies and Stocks

Table of contents

If a financial institution has ever asked you to fax them something, you’ll understand why fintech came about. The word fintech comes about from the words “finance + technology” and refers to companies that are using technology to reinvent significant chunks of the archaic finance industry. The fintech ecosystem is filled with innovative business models that go well beyond mobile banking or some website that tells you which bank has the best interest rate. Top fintech companies are enjoying success because they are solving pain points found in the traditional bank, a place where financial technology isn’t seen as a competitive differentiator. Look no further than Tifin, a fintech incubator that starts with the customer, not the asset manager.

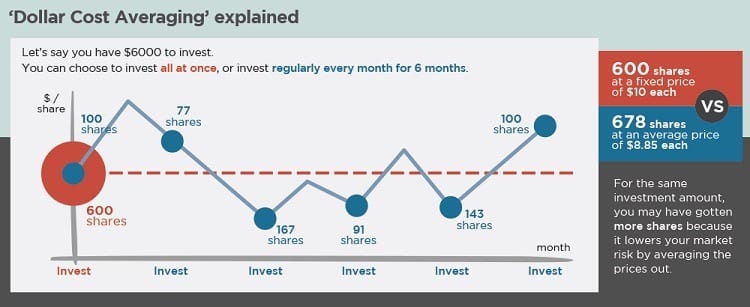

Fintech is creating disruption at a massive scale. For example, you may have heard of Robinhood, a fintech company that lets their clients trade stocks for free, but also sells them extremely risky products. In response to that competitive threat, retail brokerage firms have largely dropped all trading fees and the industry underwent consolidation following those announcements. For investors, the lack of fees makes it easy to engage in best practices like dollar-cost-averaging. Free trading seems to be the norm now, and they even have free trading for algo traders.

Some areas of fintech are more mature than others, and consequently have quite a few competing startups trying to do the same thing. For example, at least nine fintech startups are working on transferring money across borders as an alternative to Western Union. Another example would be point-of-sale payment technologies, an area where we identified at least eight startups dabbling in. If you plan to do business with China, startups like Revolut offer free currency exchange services.

What may surprise you is just how creative some fintech business models have become. Such examples of fintech innovation include:

- Motif Investing – Allows investors to create their own ETFs. (Acquired by Folio.)

- Affirm – Offers point-of-sale financing for consumers

- Avant – Issues personal loans using an AI-powered credit score that considers 10,000 variables and predicts default rates.

- Fundbox – Offers business loans for startups that have little or no credit because they’re so new.

- Blooom – Scans your 401K holdings and figures out how to reduce the fees you’re paying.

- Kasisto – Resolves finance-related customer support queries 82% of the time without needing a human.

- Ocrolus – Keeps humans from having to do the dull work of manually scanning through financial documents.

- Addepar – From the maker of Palantir, a financial operating system used to manage money for the world’s wealthiest people.

- Revolut – Offers free currency exchange services undercutting the steep fees most banks charge.

- Remitly – Helps overseas workers send remittances home to their families.

- SoFi – Reinventing online banking via app

- DraftKings – Helping people gamble more (okay, maybe not that innovative)

These are just some examples of innovative fintech companies out there. While all the companies we’ve listed above are startups, some, like Upstart (and soon Pagaya), are publicly traded, though you may want to consider the risks before investing. Today, we’ll dive into some of the major themes in the fintech space like alternative data and alternative asset classes. (If you’re new to investing, you should read our Complete Guide to Buying Stocks for Beginners first.)

Investing With Alternative Data

The amount of data humans are now producing is mind-boggling. You’ve probably heard the old adage – 98% of all data was created in the past two years – and that’s probably still the case. That’s because new technologies like the Internet-of-Things will bring billions of sensors online that all produce data. Just look at how much data there is on the Internet now. All that data can be used to produce insights. In no domain can information prove more lucrative than in the wide world of investing. We call these new data sets “alternative data.” From counting Tesla’s using satellite imagery to monitoring the movement of corporate jets, alternative data is often used by traders to generate alpha. Here are just some examples of alternative data that’s being harvested, cleansed, and sold to people who use it to generate profits.

- Sentiment Data – RavenPack’s alternative data platform scours the Internet for sentiment data, a must-have in the systematic trading space given the proven value of gauging investor emotion.

- Geopolitical Risk – Startups like Geoquant are building AI-driven political risk intelligence platforms that measure, analyze, and forecast political risks in real time

- Personal Wealth Data – Knowing who out there has amassed the most wealth can be useful when you’re trying to sell investment products. A startup called Windfall Data offers “wealth screening” services that mine publicly available data to find wealthy prospects.

- Tracking Cell Locations – Tracking the movement of cell phones can reveal remarkable insights that can be used for more than just marketing. Thasos Group website has a wealth of use cases that show how tracking cell phone locations can provide useful geospatial data that can be turned into insightful information.

- No More Bloomberg Terminals – Anyone else puzzled as to why archaic Bloomberg terminals are still being used? A startup called Sentieo is developing a replacement for Bloomberg machines that will use machine learning to gather data quickly and make it usable.

By now you’re probably starting to wonder about things like data privacy. Some applications of alternative data are controversial, like China’s new social credit score or the use of psychographics for consumer classification. The truth is, there are thousands of types of alternative data out there that can be used to generate value.

It’s clear to see how alternative data can be used by financial institutions to generate alpha or by corporates to learn how to increase revenues or reduce costs. For retail investors, there are ways to invest with fintechs that use alternative data to generate insights and increase returns across various alternative asset classes.

Investing in Alternative Asset Classes

Perhaps the most exciting things happening in fintech for retail investors surround the availability of new and exciting asset classes to invest in. The term “asset class” refers to a type of investment. Equities – both stocks and ETFs – are an asset class. Bonds are an asset class. So is real estate. When we talk about “alternative asset classes,” we’re talking about things to invest in that may have been historically off-limits unless you were an ultra-high-net-worth individual. For example, there are now fintech platforms out there that let you invest in fine art, wine, timber, farmland, commercial real estate, and the list goes on. You can learn more about the exciting area or alternative asset classes in our guide to Investing in Alternative Assets. Just be careful because Some Fintech Companies Aren’t Good For Investors.

The Many Types of Fintech

Legaltech

In 2018, more than one billion dollars of venture capital poured into legaltech startups, with 2019 surpassing that number at upwards of $1.2 billion. We looked at some of the biggest success stories in an Oct, 2020 piece titled 6 LegalTech Startups Disrupting the Legal Industry. One of those companies, LegalZoom, is now publicly traded. Another large legaltech company that’s publicly traded is DocuSign, a SaaS offering that’s a market leader. The legal profession involves sorting through loads of information. Sometimes that search is to find the gems that can be used to sway a decision one way or another. Other times, it’s simply a matter of process. Either way, startups are finding that technology such as machine learning can come in handy for lawyers. Some startups are using artificial intelligence to generate or read through legal contracts, or using chatbots to automatically negotiate smaller contracts. Other startups are simplifying legal procedures such that you can file for a divorce online cheaply. Other examples of legaltech startups can be found in our previous piece on Artificial Intelligence and Law – It’s Complicated. You will also find some overlap between legaltech and regtech. For example, there’s a legaltech firm that helps your website become GDPR compliant. That would probably fit best in our next fintech category – regtech.

Regtech

RegTech – It’s like FinTech but Spelled Differently. That was the name of an article we published which talked about how Deloitte said “Regtech is the new Fintech,” back in 2015, and the name stuck. That caliber of thought leadership is why Deloitte makes the big bucks and now we have a whole slew of regtech startups cropping up across a broad number of application areas. While FinTech is trying to eat financial institution’s lunches, RegTech is helping financial institutions make a healthier lunch. In a follow-on piece, we gave you 9 Examples of Regulatory and Compliance Regtech Startups doing everything from KYC to spotting insider trading to identifying money laundering. Another area of regtech seeing lots of interest from investors is digital identity verification.

Insurtech

Insurance is a fascinating business. You need to accurately predict outcomes in order to make insurance policies profitable. Sounds like the perfect application for some technologies like predictive analytics. We previously discussed how technology will transform the entire insurance industry, in good ways and bad. When self-driving cars finally come to fruition, accidents will plummet, and all those car insurance premiums will dry up. At the same time, insurance companies will benefit from the removal of archaic manual processes using robotic process automation and improved forecasting using artificial intelligence for predictive analytics. At least nine insurtech startups are using technology to improve the underwriting process. At least seven companies are using geospatial imagery in property and casualty insurance.

As for business models, pay-as-you-go insurance from Metromile means you pay according to how much you drive. On-demand insurance is an innovation making insurance coverage literally a snap or swipe. Being able to complete a marathon means you’re healthy by definition, so Health IQ offers runners a discount on life insurance. All you need to do is show that you have completed an organized running event(s). If you care about your body, you’re probably a safe driver. Insuretech startup Root offers a car insurance discount for safe drivers which they’re able to afford because they choose not to insure risky drivers. Speaking of insurance, it’s one of the areas that helped China’s Ant Financial become the biggest fintech company in the world.

Retail investors can check out Lemonade, a new publicly traded insurtech company that’s enjoyed success in building a list of youthful customers quickly, and now needs to show that they can do so profitably.

Other publicly traded insurtech stocks include:

The Biggest Fintech Company in the World

Considering that almost one out of every five people on the planet live in China, it’s no surprise that the biggest financial technology company in the world is Ant Financial which has taken in $22 billion in funding and is now worth – at least the last time we checked – more than Goldman Sachs and Barclays combined, with a valuation of $150 billion. This fintech unicorn offers a variety of different product offerings including an online payment platform, a comprehensive wealth management app, a private online bank, and of course, insurance products. Retail investors can get indirect exposure to Ant Financial by purchasing shares of Alibaba (BABA) which owns 33% of Ant.

Fintech Investing and Stocks for Retail Investors

In looking at fintech holistically, opportunities for retail investors aren’t so much in buying “fintech stocks” per se, but rather using the various fintech platforms to open up new avenues for investing in alternative asset classes, saving money using free personal finance apps, or even reducing 401K fees. If you don’t have any money saved up to invest, micro-investing apps can help show you the easiest way to save money. Many startups offer AI-powered personal finance assistants that can help you meet your goals in the same way a human advisor can.

When it comes time to invest, firms like Interactive Brokers enable investors to buy foreign stocks on international stock exchanges, something that now opens up opportunities like investing in China’s growth. There are now more ETFs than there are stocks, just be sure to check if the constituents actually give you exposure to the theme. For example, we recently looked at a few fintech ETFs you might consider owning, only one of which gives you exposure to global financial technology stocks. It’s all detailed in an article titled, “Global X FinTech ETF or Ark Fintech Innovation ETF?“

Fintech investors should also consider how payment gateways are disrupting multiple industries – from the global banking system to the $2.6 trillion restaurant industry. We look at three of the largest payments companies in our piece on Square Stock vs. Adyen Stock vs. Paypal Stock, though one of these it not like the others. Adyen appears to be the most promising way to play B2C payments while PayPal doesn’t provide enough transparency around where revenues are coming from. But the consumer payments opportunity is dwarfed by the $125 trillion B2B payments opportunity. We looked at 5 Pure-Play Stocks for the B2B Payments Thesis and narrowed it down to two – AvidXchange and Billtrust. One of those stocks we added to our own tech stock portfolio. We also looked at payments in emerging markets with our piece on StoneCo, dLocal, and NuBank. Only one of these companies stood out, dLocal, though Scorpion capital disagrees with us on that.

Also check out our other pieces on fintech and legaltech stocks including:

- A Pure-Play LegalTech Stock for FinTech Investors

- DISCO Stock – Using Tech to Strengthen the Law

- Intapp Stock – An Institutional Fintech Platform

One publicly traded fintech company melding legaltech regtech and insuretech is Clearwater Analytics which provides a cloud-based platform for asset managers.

Venture Capital and Fintech

As you would expect, some people have raised questions around how venture capital itself can be transformed. We might ask, why fix what’s not broken? The top venture capital firms on this planet have achieved that status because they know the optimal way to direct capital into potential success stories. Sure, some venture capital firms like InReach Ventures use machine learning to find potential investments. That may be a good way to scout startups, but you still need to vet them. Expert investors like Peter Thiel have a knack for selecting companies with the most potential. VCs are also looking abroad more often as Chinese venture capital firms start to fund deals in Asia where nearly 60% of the world’s population lives.

For retail investors, you can buy shares of the world’s biggest startups on secondary markets such as EquityZen, Sharespost (now part of Forge Global), or CartaX, but you’re not investing alongside venture capital firms. To do that, you’ll want to check out a little-known firm called Alumni Venture Group. For non accredited investors, there are some publicly traded venture capital firms. Check out Draper Esprit – A Publicly Traded European VC Firm, IP Group in the U.K, and a firm we really like – Scottish Mortgage. Whatever you do, never get involved in equity crowdfunding.

Penny Stocks Suck

Lastly, a word of warning. There is one sure way to lose money investing in stocks, and that is by dabbling in penny stocks or what they call over-the-counter stocks. We’ve seen countless examples of penny stocks that fail, so don’t be a sucker and let some clueless management team string you along with broken promises.