Why is Upstart’s Stock Price Soaring?

Table of contents

Competent investors act with conviction. They don’t second guess their decisions when a stock price starts falling. Well actually, everyone does, but competent investors recognize the fear for what it is and manage that emotion. A subscriber recently said, “I like that you don’t sell beaten down stocks.” If our thesis hasn’t changed, why would we? It’s the perfect opportunity to buy some shares on the cheap.

The same can be said when you don’t buy a stock and it soars. That’s when FOMO kicks in for most newbie investors. They capitulate and decide to climb on board the money train – choo choo! Many eventually end up holding the bag. If you decide not to invest in a stock, then it climbs +790%, that doesn’t mean you made the wrong decision. If the reasons for avoiding the stock haven’t changed, then your decision shouldn’t either. One good example is a fintech stock called Upstart (UPST).

Why is Upstart’s Stock Price Soaring?

We last looked at Upstart in a December 2020 piece titled Upstart Stock – A Play on AI-Powered Consumer Lending. In that piece, we talked about why we weren’t going to invest in the company:

- Too much reliance on the American consumer

- Demand for unsecured loans can dry up quicker than secured loans

- Potential regulatory risks coming from “discriminatory lending”

- Customer concentration risk

- Lead provider concentration risk

Since we expressed those concerns, shares of Upstart have soared +790% in less than a year. Based on what we know about the efficient market hypothesis, it hardly seems likely that much value was created so suddenly. The impetus for the price surge appears to be the strong revenue growth they’ve been having over the past several quarters (more on this in a bit). Let’s look at why Upstart’s valuation is surprisingly cheaper now than it was before the stock’s meteoric rise.

Is Upstart Overvalued?

Several subscribers have reached out to us asking about Upstart. The first was someone who was thinking of opening a position. The other is someone who presently holds a large position. Each person needs to ask themselves, is a +790% stock price appreciation in a single year merited? One way to do that is by looking at valuation.

After the first day of trading after their initial public offering (IPO) in December of last year, Upstart ended up with a market cap of $3.26 billion. Here’s how our simple valuation ratio looked back then:

- Market Cap / Annualized Revenues

3,260 / 65.36 = 50

That’s way too rich for our blood as we won’t invest in any stock with a valuation over 40. But if we look at that same ratio today, we see it’s gotten a whole lot cheaper.

- Market Cap / Annualized Revenues

21,279 / 776 = 27

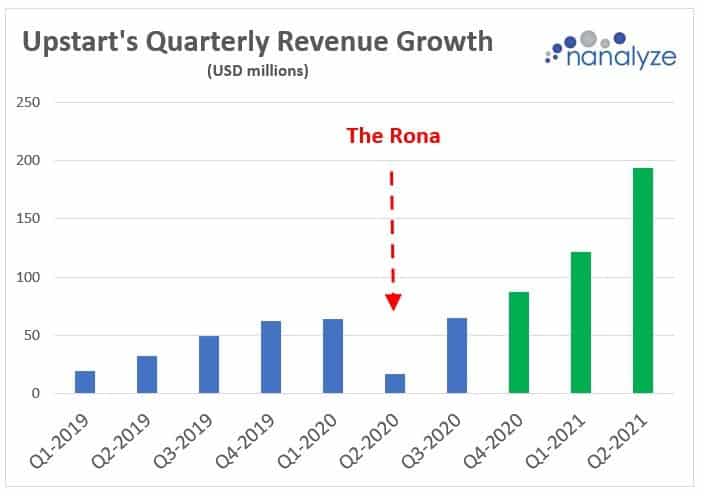

The recent run up in price is justified based on our simple valuation ratio which rewards sharp revenue growth. In the below chart, you can see the three quarters of revenue growth that followed our last piece on Upstart (in green):

What you see in the above chart is the American consumer being issued a whole lot of loans – over 280,000 in last quarter alone. Some of these loan recipients are the types who flock to Robinhood with their stimmy checks and a dream, only to have their asses handed to them by hedge funds. Their ability to exercise financial prudence is questionable, and we’re expecting that AI algorithms separated the wheat from the chaff. Still, we’re concerned with this sudden uptick. If lenders had to pick a time to loosen purse strings, now probably wouldn’t be the time.

While we’re checking in with Upstart, let’s see if any of our prior concerns have been alleviated.

Some Concerns About Upstart

Upstart is heavily reliant on the American consumer, something that won’t be changing anytime soon. What may change are the types of loans being offered. In April 2021, Upstart acquired an e-commerce platform for car dealerships called Prodigy. Consideration of $89 million was paid, and now Prodigy will bring Upstart’s AI-enabled auto loans to dealerships across the country where a significant number of auto loans are transacted. (Over $1 billion worth of vehicles were sold through the Prodigy platform in Q2-21.) Offering more types of loans outside of just unsecured loans provides Upstart with a form of diversification.

Regarding potential regulatory risks coming from “discriminatory lending practices,” this is an unknown that isn’t going anywhere. It’s the same type of concern we have with insurtechs being told they can’t use big data to make decisions with.

Another concern we just can’t overlook is customer concentration risk. From the company’s most recent earnings report:

For the three and six months ended June 30, 2021, Customer A accounted for 63% and 62%, respectively, of the Company’s total revenue and a second customer accounted for 22% and 23%, respectively, of the Company’s total revenue.

Credit: Upstart

Let’s say that the economy goes into a tailspin and suddenly the loans Customer A purchased from Upstart start significantly underperforming. What’s the likelihood they’ll keep buying them? When two customers are responsible for 80% of a company’s revenues, that’s a huge concern.

Then there’s risk around Upstart’s key lead provider. Around 49% of loan originations Upstart produces are derived from Credit Karma traffic. Late last year, Credit Karma was acquired by Intuit. As we’ve learned, you always make more money selling your products than someone else’s. Will Intuit think the same for Credit Karma? With either party being able to terminate their affiliate agreement with 30 days’ notice, that ought to make Upstart quite nervous. With $600 million in cash on their books, they’ll likely continue diversifying their business to reduce some of these risks.

Conclusion

A few examples where being risk averse worked out well include Ali Baba, Zymergen, Metromile, View, SPACs in general, and just about every penny stock known to man. If there’s a potential game changer, and we’re a bit late to the game, we’re fine with that. 10X Genomics is a good example of a company we waited to invest in because we’re risk averse. And being risk averse means we’re perfectly fine missing some of the money trains leaving the station.

Tech stocks are risky enough. We don’t like investing in tech companies that immediately run into crisis when there are times of economic turmoil. The stock price volatility on display from Upstart can swing both ways. We still don’t like what we see and will continue avoiding the stock.

Share

Why do the four icons for Tweet, facebook, instagram and reddit always present on the screen? It make reading the articles extremely unpleasant. Please take them off the screen, or let me know how to do that. It’s so difficult unproductive to be able to read only two lines of text, that isn’t blocked by the 4 icons!!!!!!! It’s almost so annoying that I’m starting to regret I signed up! Blocking the screen will certainly discourage me from trying to read the articles.

Hi Kathleen,

You aren’t the first person to raise that, but hopefully the last. We’ve now moved the floating share buttons to appear at the bottom of the screen so that should solve the problem. Just let us know if it doesn’t.

Thank you for your financial support!

U.S.-Israeli fintech Pagaya is an artificial intelligence network helping consumers get credit approval.

Pagaya Technologies LTD. to become publicly traded company through combination with EJF Acquisition Corp (EJFA).

The business model is similar to Upstart’s, but with a more diversified revenue base.

Pagaya appears to be growing meaningfully faster than Upstart.

We’ve tossed this SPAC over the wall to our research team who will vet it for coverage. Thank you for raising.

Upstart price reached its top in October 2021 – around $400 (so quite soon after this article appeared) and since then it lost over 70% of its value (now around $117). So the article was right at that particular time.

They remain profitable, P/E is around 79 (based on the latest quarter) and they have high revenue growth.

Being right or wrong is all a matter of perspective – and time. The entire tech stock landscape is sliding so it’s no surprise Upstart is correcting.

Our simple valuation ratio comes in at 10.5 (9,616 / 912) so we wouldn’t say it was overvalued. We just don’t put much faith in the American consumer’s ability to pay back their debts.

Upstart -48% today pre-market ($39.80).

So that means it is -90% since October.

Wouldn’t touch it at any price. Too over reliant on the American consumer.