Toast Stock: A Pure Play on U.S. Restaurant Receipts

Table of contents

Long before Anthony Bourdain became a household name, he was a cult figure among restaurant workers everywhere because of his first work – his magnum Opus One – Kitchen Confidential. Finally, someone adequately captured what happens behind those swinging doors. The illegals in the dish pit, the convicts in the kitchen, the pervasive drug use across the entire house, it was all laid bare for everyone to see. Don’t order a steak well done, don’t send food back to the kitchen, always treat your waiter with respect, these bits of advice are common sense for anyone who’s toiled in a restaurant kitchen in any capacity. For everyone else, it was an eye-opener.

The restaurant industry is one of the largest, most complex, and most competitive markets in the world, with an estimated 22 million restaurant locations globally generating greater than $2.6 trillion in annual sales in 2021. We don’t need Anthony Bourdain to tell us that most restaurants use technology sparsely, if at all. It’s a massive opportunity that’s being tackled by a company called Toast which recently filed for an initial public offering (IPO).

Luck is not a business model

Anthony Bourdain

About Toast Stock

Founded in 2011, Bahstun’s own Toast raised $902 million in disclosed funding from investors that include Amazon. T. Rowe Price, and Google Ventures. All that money was spent building a technology platform that an entire restaurant can run on. It starts with hardware – point of sale (POS) systems that can be used by cashiers or guest, terminals for the back of the house where chefs can fill orders, and handhelds for the waiters to see their plates coming up, or to quickly know what’s been 86’d.

Powering Toast’s platform is software that enables everything from contactless ordering to online ordering to marketing to payroll and team management. With over 48,000 restaurant locations using their platform, Toast is experiencing some remarkable traction. In June 2021, they processed an average of over 5.5 million guest orders per day. While you may be tempted to think the business model is largely software-as-a–service (SaaS), that’s hardly the case.

Toast’s Business Model

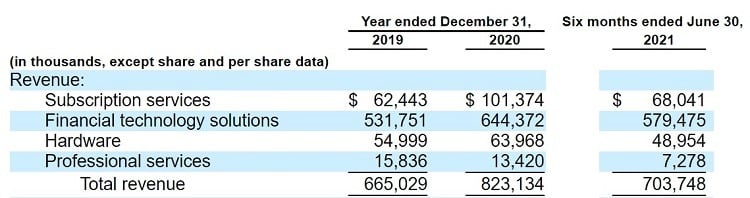

Toast has four main revenue streams: subscription services, financial technology solutions, hardware, and professional services. Revenues for the first half of 2021 are showing remarkable growth with the company on track to clear over a billion dollars in 2021 revenues.

In looking at the above chart, we see around 10% of Toast’s revenues come from subscriptions – the SaaS component of their business. More than 80% of revenues come from “Financial Technology Solutions” which represents fees they receive from payments made to restaurants by customers. For the first half of 2021, Gross Payment Volume (GPV) was $23.4 billion from which Toast was able to receive around 0.579 billion in commissions – about 2.5% of GPV.

While Toast also facilitates loans to restaurants with a single bank partner, revenues received from servicing loans account for less than 1% of the “Financial Technology Solutions” segment. Given the revenue stream is so miniscule, it’s puzzling why Toast is “subject to credit risk on the loans extended by [their] partner bank.” Having exposure to underperforming restaurant loans is not a good place to be right now.

The Corona Elephant

Let’s talk about the elephant in the room – The Rona – and its effects on the restaurant industry. In our piece on Silvergate Capital, we noted how their commercial loan portfolio was impacted by underperforming loans, 62% of which came from the hospitality industry. It’s no surprise that restaurants are being punished right now, from labor shortages to restrictions on how many people can dine at any given time. As investors, we’re very concerned with how Toast may be weathering this storm given their entire business surrounds hospitality. So far, so good, as the below chart shows minimal impact from the pandemic.

Given the revenue segment breakdown we discussed earlier, Toast could give their technology platform away and simply recoup the costs through commissions on payment volume. In fact, over $20 million in direct SaaS relief credits, as well as additional access to loans through Toast Capital, were provided to restaurants as a form of relief from the pandemic. One reason Toast has enjoyed the success they have is because they’re restaurant people helping restaurant people. Around two-thirds of Toast employees have previously worked for a restaurant.

Should You Buy Toast Stock?

Whenever you’re thinking about investing in a stock, consider what you’re getting exposure to, and how that exposure compliments your current portfolio. For us, Toast is pure-play exposure to restaurant receipts in the United States, a business that’s strictly dependent on how much money people in the United States spend on food from restaurants. Surprisingly, more than half of restaurant expenditures in 2021 were on takeaway.

Euromonitor projects that, in 2021, 40% of food service revenue in the United States will be from dine-in, 51% will be from takeout and drive-through, and 9% will be from home delivery.

Credit: Toast

It’s reasonable to suspect that economic turmoil might be looming in the not-so-distant future. If you believe that the American consumer might fall on some hard times soon, then you should avoid companies that rely on discretionary spending. Sure, we can argue whether restaurant spending is in fact discretionary, but what happens to all those takeout orders when times get tough? The success of Toast rests on the ability of consumers to keep spending as they have been. As we’ve said before, we’re reluctant to invest in any company whose success depends solely on the American consumer’s spending habits.

Then, we need to consider how Toast compliments what we’re already holding. The mechanics of their business model resemble a payments company more than a restaurant technology company. We’ve already placed our bets on one payments company, and we don’t need another in our portfolio at the moment, especially one that derives all its revenues from a single industry in a single country.

Conclusion

Restaurants typically see operating margins of 4-5%. By adopting the Toast platform, they can expand those margins, and have a better chance of surviving in a viciously competitive space. We love what Toast is doing for restaurant owners, but dislike how their success relies heavily on discretionary consumer spending by the Americans.

Should the IPO go through as planned, shares of Toast will trade under the ticker TOST.

Share