10 AI Personal Finance Assistants Helping You Save

Table of contents

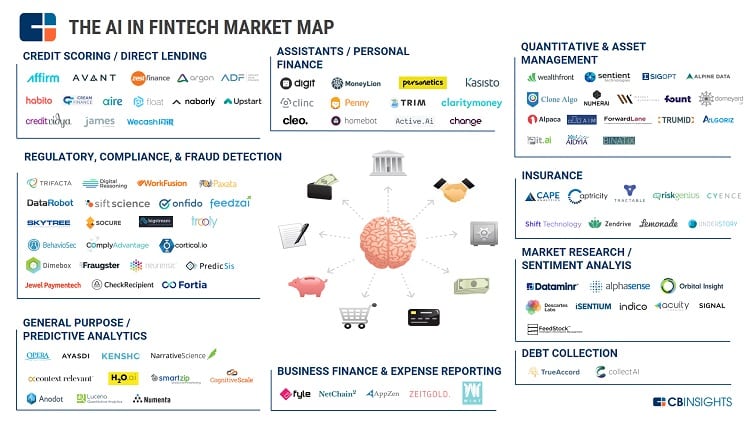

You got to have money to make money as the old saying goes. We recently looked at how the big robo advisors out there are offering a very low-fee way for you to invest in your future which everyone can access easily. Now what you need to do is start saving money so that you have something to invest. Since artificial intelligence (AI) is being used for everything from detecting Alzheimer’s disease to selling you weed, why not enlist these powerful algorithms to help you save some money or at least provide some insights into all the stuff you spend your money on. We took this excellent market map from CB Insights on AI in Fintech and found 12 AI personal finance assistants they’ve identified:

If your amazing AI-powered personal finance assistant startup isn’t on that list, email them and complain about it. Nobody ever does that and they love the extra work. Just kidding, they do their best with these market maps and your startup didn’t make the cut. You just need to start failing harder and faster. Here’s the list of 10 AI personal finance assistants that did make the cut (we only covered the 10 American startups because the Asians don’t have a problem with saving and the Europeans have other things to worry about right now).

Save Money Without Thinking About It

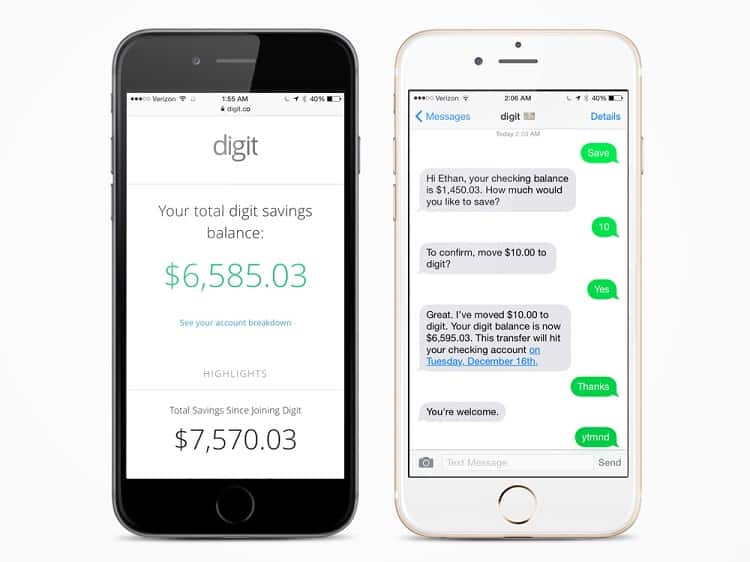

![]() Founded in 2013, San Francisco startup Digit has taken in $36.3 million in funding from investors that included Google Ventures to develop a platform that analyzes spending habits to safely set aside small amounts of money for you. Every 3-4 days, a random sum of money (say like $2 to $50 as an example) is moved over to a savings account (held over at Digit). You use SMS or their app to communicate with Digit (not offered via website) and the whole thing costs $2.99 per month.

Founded in 2013, San Francisco startup Digit has taken in $36.3 million in funding from investors that included Google Ventures to develop a platform that analyzes spending habits to safely set aside small amounts of money for you. Every 3-4 days, a random sum of money (say like $2 to $50 as an example) is moved over to a savings account (held over at Digit). You use SMS or their app to communicate with Digit (not offered via website) and the whole thing costs $2.99 per month.

While the mention of “AI” is a nice marketing touch, it’s hard to imagine this whole thing couldn’t be setup using traditional algorithms. Plus, how accurate do you need to be? Most people who live paycheck to paycheck (if they didn’t, then they wouldn’t need this app) adjust their spending based on what their remaining balance is. It’s just like when you wake up after a heavy night out at the pub and check your wallet. You always seem to have spent nearly all your money and still somehow managed to grab a kebab on the way home.

Boost Your Wallet

![]() Founded in 2013, New York startup MoneyLion has taken in $24 million in funding so far to offer a broad range of solutions like offering you quick loans, helping you reduce interest rates, and general personal finance stuff. The bigger picture of your personal financial situation is accomplished by connecting all your accounts (student loans, credit cards, car loans, etc.). They use machine learning and big data to regularly underwrite better loans at affordable rates (sound familiar?). Of course, it also helps that you’ve bared your financial soul to the company so they have a pretty safe understanding of what you can afford to pay and how “responsible” you are. They have a cool feature where you can invite your friends and then get “boosts” that lower your interest rates. They say 83% of users improve their credit using the app and they’ve saved people over $5 million in rate savings.

Founded in 2013, New York startup MoneyLion has taken in $24 million in funding so far to offer a broad range of solutions like offering you quick loans, helping you reduce interest rates, and general personal finance stuff. The bigger picture of your personal financial situation is accomplished by connecting all your accounts (student loans, credit cards, car loans, etc.). They use machine learning and big data to regularly underwrite better loans at affordable rates (sound familiar?). Of course, it also helps that you’ve bared your financial soul to the company so they have a pretty safe understanding of what you can afford to pay and how “responsible” you are. They have a cool feature where you can invite your friends and then get “boosts” that lower your interest rates. They say 83% of users improve their credit using the app and they’ve saved people over $5 million in rate savings.

Cognitive Banking Starts Here

![]() Founded in 2010, New York startup Personetics has taken in $18 million in funding from investors that include Sequoia to cater “personalized customer experiences” for financial institutions to reduce operational costs for the institution – like 55% fewer live agent requests. While the buzzwords come quick and heavy, they provide AI algorithms and chatbots that big banks can use to look like they’re staying on top of technology. They already serve more than 30 million customers and half of the top-12 banks in North America and Europe have signed up.

Founded in 2010, New York startup Personetics has taken in $18 million in funding from investors that include Sequoia to cater “personalized customer experiences” for financial institutions to reduce operational costs for the institution – like 55% fewer live agent requests. While the buzzwords come quick and heavy, they provide AI algorithms and chatbots that big banks can use to look like they’re staying on top of technology. They already serve more than 30 million customers and half of the top-12 banks in North America and Europe have signed up.

They Have Your Financial Back

![]() Founded in 2016, New York-based startup Clarity Money has taken in $14.5 million in funding from investors that include Citibank to develop an app that aims to decrease bills (you can also do this by not buying stuff), cancelling unnecessary accounts (first world problem), transferring money, saving money and working on that credit score. They went live in January of this year and 3 months later, over 100,000 people had signed up and on average saved $300 from canceled subscriptions. As you would expect, they’re personalizing the whole experience with AI, particularly natural language processing or NLP (understands your questions), anomaly detection (spots outliers), and spectral analysis (haven’t the foggiest).

Founded in 2016, New York-based startup Clarity Money has taken in $14.5 million in funding from investors that include Citibank to develop an app that aims to decrease bills (you can also do this by not buying stuff), cancelling unnecessary accounts (first world problem), transferring money, saving money and working on that credit score. They went live in January of this year and 3 months later, over 100,000 people had signed up and on average saved $300 from canceled subscriptions. As you would expect, they’re personalizing the whole experience with AI, particularly natural language processing or NLP (understands your questions), anomaly detection (spots outliers), and spectral analysis (haven’t the foggiest).

Siri for Financial Services

![]() Founded in 2013, New York startup Kasisto has taken in $11.45 million in funding so far to develop a conversational AI platform called KAI that aids in banking and personal finance management. Investors include Harvard Business School, Mastercard, and banks like Wells Fargo, BBVA, and DBS. We talked recently about chatbot companies for enterprises, but Kasisto considers themselves a platform which communicates with you across multiple channels – like Facebook (horrible idea people). It’s all about “intelligent conversations” and “actionable recommendations”, so banks are lining up to license it and replace “John in Mumbai“.

Founded in 2013, New York startup Kasisto has taken in $11.45 million in funding so far to develop a conversational AI platform called KAI that aids in banking and personal finance management. Investors include Harvard Business School, Mastercard, and banks like Wells Fargo, BBVA, and DBS. We talked recently about chatbot companies for enterprises, but Kasisto considers themselves a platform which communicates with you across multiple channels – like Facebook (horrible idea people). It’s all about “intelligent conversations” and “actionable recommendations”, so banks are lining up to license it and replace “John in Mumbai“.

Ask the Unified Brain Anything

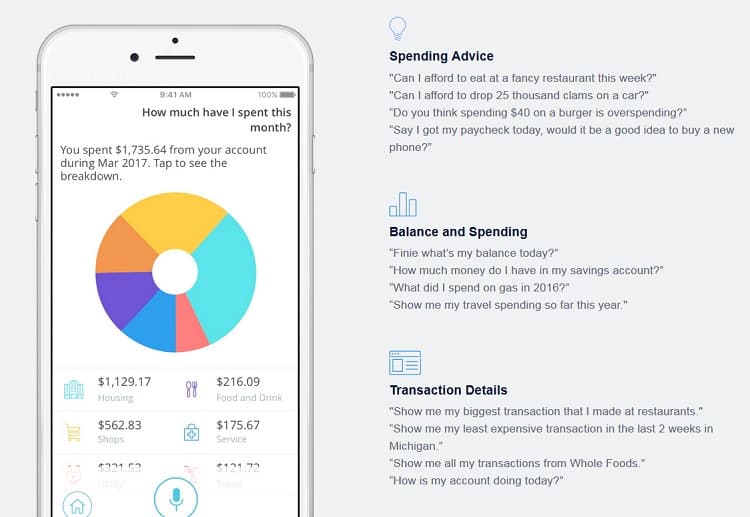

![]() Founded in 2015, Michigan startup Clinc has taken in $7.5 million in funding so far to develop a mobile and voice-activated platform that uses AI and machine learning to answer queries regarding finance and banking.

Founded in 2015, Michigan startup Clinc has taken in $7.5 million in funding so far to develop a mobile and voice-activated platform that uses AI and machine learning to answer queries regarding finance and banking.

Update 05/20/2019: Clinc has raised $52 million in Series B funding to expand its workforce to 140 people by next year and open a new 26,000 square foot office in Ann Arbor. This brings the company’s total funding to $59.8 million to date.

This startup was spun out of the University of Michigan, and more resembles an industry agnostic technology solution that’s first being sold to the finance industry. This shows in the fact that they’ve created an open source platform to develop complex AI systems called Lucida, a tool that’s used by companies including Diffbot which we profiled last year. Now they need to move fast to secure their place in helping answer personal finance questions like the ones below:

We don’t need AI to answer those first 4 questions. For people who actually need to ask an app for advice on how to manage their money, the answers to the first four questions are “no, cook at home“, “no, buy a used Toyota“, “fcuk yes“, and “absolutely not“.

Saving Money by Cancelling Subscriptions

![]() Founded in 2016, California based startup Trim has taken in $2.2 million in funding so far to develop a software-driven assistant that tracks all subscriptions and cancels the unused ones. Yes, this is the same business model used by Hiatus, a startup that made our list of “6 Startups Solving First World Problems“. As they say at Trim, “personal finance is hard”. People don’t cancel subscriptions because they’re too

Founded in 2016, California based startup Trim has taken in $2.2 million in funding so far to develop a software-driven assistant that tracks all subscriptions and cancels the unused ones. Yes, this is the same business model used by Hiatus, a startup that made our list of “6 Startups Solving First World Problems“. As they say at Trim, “personal finance is hard”. People don’t cancel subscriptions because they’re too lazy busy and even when you find you have unnecessary subscriptions, you then have to take 5 minutes out of your day to log into your account and cancel. Trim will do it for free, and they’ve already saved people $8 million. They make money by negotiating your bills for you and taking a cut of the savings. It’s hard to see AI being used for anything else other than the NLP used to understand what you’re typing.

A Financial Chatbot Named Penny

![]() Founded in 2015, San Francisco startup Penny has taken in $1.2 million in funding so far to offer solutions in finance and banking through an AI chatbot that has managed to score the absolute best name possible for a friendly sounding chatbot that helps you manage your money. “Whenever you open the app, she’ll chat with you about finances,” it says, and unlike your spouse, she gets smarter every day. It’s a free app to download, but you can’t use it without baring your financial soul and connecting your checking account. They make money from donations (rolls eyes) and by partnering with financial products she thinks you can’t live without.

Founded in 2015, San Francisco startup Penny has taken in $1.2 million in funding so far to offer solutions in finance and banking through an AI chatbot that has managed to score the absolute best name possible for a friendly sounding chatbot that helps you manage your money. “Whenever you open the app, she’ll chat with you about finances,” it says, and unlike your spouse, she gets smarter every day. It’s a free app to download, but you can’t use it without baring your financial soul and connecting your checking account. They make money from donations (rolls eyes) and by partnering with financial products she thinks you can’t live without.

Like Fairy Dust for Your Bank Account

![]() Here we see another excellent choice of names, an app called Change which uses artificial intelligence to help you spend your hard-earned money more wisely. Whatever happened to just using normal intelligence for that? Founded in 2015, New York-based startup Change Labs has taken in $800,000 in funding so far to aid consumers in financial tracking and personal banking matters through advanced predictive analytics and behavioral science. It’s free, they have an “auto-savings feature” (you hear that Digit?), and if you use the app, your 4th of July would have looked like this:

Here we see another excellent choice of names, an app called Change which uses artificial intelligence to help you spend your hard-earned money more wisely. Whatever happened to just using normal intelligence for that? Founded in 2015, New York-based startup Change Labs has taken in $800,000 in funding so far to aid consumers in financial tracking and personal banking matters through advanced predictive analytics and behavioral science. It’s free, they have an “auto-savings feature” (you hear that Digit?), and if you use the app, your 4th of July would have looked like this:

They make money by offering a free overdraft protection (7-day loan for $100) that incurs a one-time fee and through tips paid by users. Maybe they can use machine learning to estimate the amount of tips they expect to receive when they need to raise funding again.

Home is Where Your Wealth Is

![]() Founded in 2015, Colorado-based startup Homebot has taken in $125,000 in funding so far to develop a platform that offers solutions in financial planning in mortgage lending and real estate industries. The idea is that for most Americans, the vast majority of their wealth is tied up in home equity. The app can be used by homeowners, lenders, and real estate agents (yikes). Plug in all the variables and it will make recommendations about how you can make more money from your house “using the power of AI” we presume.

Founded in 2015, Colorado-based startup Homebot has taken in $125,000 in funding so far to develop a platform that offers solutions in financial planning in mortgage lending and real estate industries. The idea is that for most Americans, the vast majority of their wealth is tied up in home equity. The app can be used by homeowners, lenders, and real estate agents (yikes). Plug in all the variables and it will make recommendations about how you can make more money from your house “using the power of AI” we presume.

Conclusion

The question we had after reading about all these startups is how much real value is being offered by using AI here? We go back to our good old litmus test for any “AI company” which is that we expect to see performance demonstrated with some amazing metrics, scalability as people adopt because of above-average performance, and continuous improvement over time. Even if AI has a minimal impact, they’ve managed to secure the last frontier of big data – your financial soul – in exchange for saving you some money. For people who lack financial discipline, this sounds like a win-win.

Share

Nice article Nanalyze. FinArt Money Manager is recently launched android app to manage money and bills automatically. FinArt has addressed the data privacy and security concerns which each of us has, esp when dealing with financial data.

Check it out on Google play store

Thank you for the compliment.

We strongly advise people not to just start downloading apps and connecting them to their bank accounts. If you’re not funded by a big VC, we’re saying no. It’s just too dangerous out there.

You are welcome.

Its very true, connecting the third party apps to bank accounts is too dangerous .Because of this FinArt is designed to work without connecting to the bank accounts, it works completed based on SMS available on phone.

So you are saying teams and companies building apps that don’t get VC funding are not safe?

No, I don’t mean that. I think i did not put it correctly.

Whether company is funded by VC or not, does not make it less or more secure. It all depends on the core values of the founding team. If founding team is genuinely concerned about safety and privacy of its user’s data then they will always keep this aspect at center for every decision making while building the solution.

Matt, if above question was not meant for me, kindly ignore it.

Agree but guess what. All the core values in the world aren’t going to make me just open up my bank account to someone. We’d like to see some strong oversight from a third party and that’s where our VC comment comes into play.

Good question Matt. We’re saying we choose not to connect our bank account to just any old app. The business model for the app needs to have some oversight from individuals who can detect potential problems with the handling of such sensitive information. VCs would do that. Your bank isn’t backed by a VC but you trust your bank because you believe that they are governed by regulatory oversight.

nice article. just want to add one more fintech startup named BillTrim. They are also like trim but a better alternative to it.