Why Is indie Semiconductor Stock So Popular?

Table of contents

Since our foray into YouTube a few years back we’ve noticed something. The barriers to entry for financial gurus are nada. Anyone with an opinion can start talking about stonks on social media and attract an audience. Bonus points if you post relentlessly about the Holy Trinity – Palantir, Sofi, and Tesla. Most of these instant analysts have no original thoughts or tenured methodology behind their investment process (chasing clout doesn’t require that), so they’re quick to latch onto tickers and pass them around like trading cards. That brings us to today’s topic – Indie Semiconductor (INDI).

Editor’s Note: Some marketing person over at Indie told management it was a good idea to not capitalize the “i” in the company’s name. Clever right? No, it’s annoying. Aside from the title of this article, we’re capitalizing the company name because that’s what 99% of companies do. They use proper capitalization. And now back to your regularly scheduled programming.

Why Cover Indie Semiconductor Stock?

Semiconductor stocks are very popular among retail investors, but they’re also a can of worms. This is a mature industry with lots of selection, and our decisions have always been easy. We’re longtime NVIDIA (NVDA) holders and don’t need any more semiconductor exposure. Were we to exit NVDA, we’d look at names like Synopsys and ASML for reasons we’ve discussed in previous research pieces. So, when the name Indie came up in a recent piece on investing in EV chips, we decided it was worth a deep dive for three reasons:

- It’s probably been raised on our Youtube channel more than any other stock

- It’s not overly obvious what they do so many might find this analysis beneficial

- And most importantly, our Premium subscribers asked us to cover it

Let’s dig right in.

What Does Indie Do?

The first slide of Indie’s investor deck says the following:

A pure-play automotive fabless semiconductor company developing technology that supports best-in-class in-cabin experience, accelerates electrification and enables the pursuit of the uncrashable vehicle.

Credit: Indie Semiconductor

We’re less excited about the “in-cabin experience” which is a nice-to-have that’s increasingly found in all vehicles and more interested in their contribution towards electrification. As for the “uncrashable vehicle” comment, that refers to advanced driver assistance systems (ADAS) which we already have exposure to. The next step is to figure out how much exposure we’re getting to each of these three themes, how fast they’re growing, and how potentially profitable they are (gross margins). At a broader level, total revenues are growing at a great clip.

The above chart shows their growth since the company’s 2021 public market debut along with a gross margin that’s moving in the right direction. We found it on probably the only slide in their recent investor deck that contain anything useful, not unlike their glossy SPAC deck. That’s right Little Johhny. Indie went public in 2021 during the SPAC craze, and the fact their share price has only lost 30% of its value since is impressive when compared to the overvalued shite show that SPACs turned out to be.

What also makes Indie stand out in a sea of shite SPACs is their revenue forecasts. Turns out that they’ve been doing a great job of exceeding expectations with 2022 revenues of $111 (vs estimates of $91 million) and expected 2023 revenues of $226 million based on midpoint of guidance (vs estimates of $204 million). This is where we need to start distinguishing between organic growth and acquired growth.

Revenue growth is good, but let’s be honest about what’s happening here. It sounds like the Desktop Metal game plan. Sell a story to the market that you have a great growth engine, then when said money is raised, go out and acquire that growth. Acquiring growth is a lot different from organic growth, and a quick look at Indie’s balance sheet shows $309 million in goodwill and $156 million in long-term debt. So, what exactly did they acquire?

Indie’s Acquisitions

Here are the three acquisitions made by Indie Semiconductor last year (total consideration reflects cash and the value of shares spent on these acquisitions in millions).

What’s notable about these acquisitions is the terms at which they were made which all include certain performance incentives (what they refer to as contingent considerations). These provide some useful information about what each might accomplish in terms of future revenue growth.

- Silicon Radar – a revenue performance threshold of $5 million is given for last year and $7 million for the coming year (implied potential growth of 40%)

- GEO – mentions a revenue threshold of $50 million for the twelve-month period ending on March 31, 2024 and a revenue threshold of $30 million for the six-month period ending on September 30, 2024 (implies future annual contribution of $60 million with implied growth of 20%)

- Exalos – states a revenue threshold of $19 million for the twelve-month period ending on September 30, 2024 and a threshold of $21 million for the twelve-month period ending on September 30, 2025 (implied growth of around 10%)

As these are all performance targets, they assume best-case scenarios for each business. If Indie is expecting 2023 revenues of $226 million, we might conclude that the acquisition of GEO really moved the growth needle while the others not so much. It’s very hard to tell what organic growth looked like prior to these acquisitions, but the performance terms imply an expectation that organic growth will be strong going forward.

Bulls will point to 1+1=3 synergies. Fair enough, just remember that after an acquisition is made the acquirer gets to look past the window dressings and see where the bodies are buried. Research shows that most acquisitions don’t realize the synergistic benefits expected.

Comments on Indie

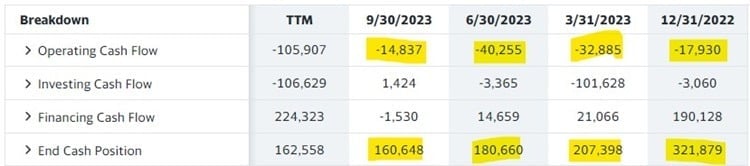

Here we see the usual story unfolding. SPAC raises lots of easy money and then decides to acquire growth they promised investors because they have tons of cash laying around. It enables Indie to exceed investors’ expectations, but we also need to watch dilution and cash burn. Operational cash burn isn’t horribly bad, but acquisitions are making a dent.

Given their strong gross margins Indie should be able to pull back on overhead expenses and achieve positive operating cash flows rather soon to avoid taking on more debt or diluting shareholders by selling more shares to raise capital.

We consider customer concentration risk to be a showstopper, though there’s no concrete cutoff number. In 2022, Indie’s top customer accounted for 37% of total revenues, down from 39% the year prior. The strong growth predicted for 2023 should dilute that number considerably, and when that gets closer to the 10% mark then we’d be able to overlook it. What’s more difficult to overlook is not knowing exactly what we’re getting exposure to.

Trying to guess what the company’s revenue segmentation breakdowns might look like would involve looking at what they’ve acquired and what management implies in their earnings call. It seems like ADAS is a key focus for the company, and that’s where they expect gross margin expansion to come from. If that’s the case, then our methodology says skip the laggard and go right for the leader in this space by a country mile – Mobileye (MBLY) with 70% market share in ADAS solutions.

When it comes to valuation, Indie’s simple valuation ratio (SVR) shows us that the stock is not currently overvalued with an SVR of just below five compared to our tech stock catalog average of six.

Indie’s popularity isn’t just about weekend warrior analysts passing the ticker around, it’s about strong revenue growth with nice margins. Where that revenue growth is coming from remains vague.

Conclusion

We left this analysis with more questions than answers. Indie’s SPAC deck talked about three focus areas, then they went out and bought a bunch of stuff. ADAS seems to be their primary focus now, but why not invest in the ADAS leader, Mobileye, instead? Non-recurring contract revenues aren’t attractive (same holds true for most hardware plays), and we’re left wondering why they spend so much on R&D when they’ve been acquiring all their growth lately. Or have they? We don’t know because we’re not given organic growth vs acquisitive growth.

Based on our tech investment methodology we apply consistently across all companies we’ll be avoiding Indie Semiconductor until they reduce that customer concentration risk (may happen soon). We’d also like them to provide more specifics as to what exposure we’re getting from an investment in their company. What do you think? Let us know in the comments section below.

Share