Wanted: A High-Growth Energy Storage Stock

Table of contents

In a world of gene editing and AI-powered brain-computer interfaces, energy storage hasn’t changed much. Sure, advances have been made in density, leading to the miniaturization of lithium batteries, which has popularized drones and electric vehicles. The growth of renewable energy has also led to an increased demand for energy storage solutions. The icing on the cake? President Biden’s Inflation Reduction Act promises to channel funding and tax credits to developers of green energy solutions. This has led to a strong interest from retail investors keen to find exposure to battery stocks and energy storage solutions.

While most of the attention gets paid to lithium batteries, that’s just one component of the energy storage thesis which we’ve divided into the following categories:

- Lithium battery manufacturers

- Energy storage solutions providers

- New battery technology developers

Our tech stock catalog contains 16 companies which fall into the above categories which we’ll examine today in our search for an attractive high-growth energy storage play for our own tech stock portfolio. We’ll start by looking at companies that manufacture batteries – the picks and shovels of energy storage.

Lithium Battery Manufacturers

Our article on The 8 Biggest Lithium Battery Stocks of 2028 vetted the largest (projected) manufacturers of lithium batteries and found several names that may merit further examination such as BYD and CATL (both Chinese firms). While we don’t invest in VIE structures, BYD actually trades as an H share which means that risk is eliminated. Though some geopolitical risks remain, we’re due for an update on BYD since our last piece in 2017. As for CATL, they’ve been hinting at an IPO in Hong Kong, but they’re off our radar until they trade as an H share.

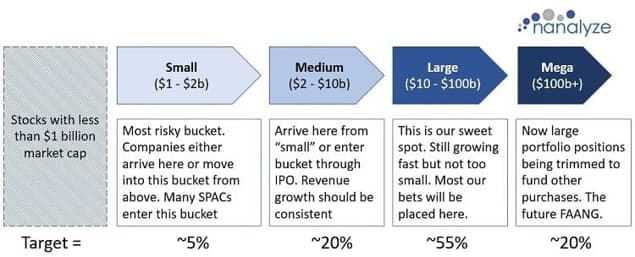

With a market cap of $100 billion, BYD also manufactures electric vehicles, which means they’re not a pure play. Ideally, we’re looking for a pure play to invest in. The same is true for Tesla, a $576 billion electric vehicle behemoth that well exceeds our optimal size target of $10 billion to $100 billion.

There are some midcap battery manufacturers to consider, one being EnerSys (ENS), a company we uncovered in our piece on 3 Mid-Cap Global Battery Manufacturer Stocks. (More on this company in a bit.) In that same article, we looked at Taiwans’ Simplo (6121.TWO), a firm that’s too difficult to follow for your average retail investor who doesn’t read Mandarin. The third company, Germany’s VARTA (VAR1.DE), has too heavy a reliance on Apple for wireless headphone batteries. Those chickens apparently came home to roost as that segment recently saw a 25% drop in revenues:

The current challenging economic situation and restrained consumer demand are compromising demand for lithium-ion batteries for True Wireless Stereo Headsets (TWS) in the area of Lithium-Ion CoinPower.

Credit: Varta

Newcomers to the scene include Microvast (MVST), a company we covered earlier this year in a piece titled Microvast Stock is a Pure Play on EV Battery Technology. Sure, they’re selling lots of batteries and equipment, but they’re having a hard time making a profitable business out of it. Gross margins for Microvast have barely been in the green over the last four quarters.

We noted a heavy dependency on China where nearly all their operations are located. It’s a geopolitical risk that can’t be ignored as relations sour between two of the world’s most economically powerful countries. Bulls will point to the recent $200 million grant Microvast received in partnership with General Motors, and indeed that sounds good on the tin. Perhaps one could look past the China dependencies, but what’s impossible to get past are those dreadfully low gross margins.

The last time we looked at Enovix (ENVX) was back in July 2020 shortly after they raised $45 million to complete their fully automated commercial production line by year-end. Things are off to a slow start. Here’s a comment from the most recent shareholder letter:

We are continuing to push the boundaries of what’s possible with our technology while developing a world class manufacturing line to fuel our growth and satisfy our customers

Credit: Enovix

Most investors would be happy to trade some boundary pushing for some battery sales. This $1.9 billion company’s glossy SPAC deck said we should expect to see revenues of $11 million for 2022 and $176 million for 2023. If they hit that 2022 goal, we’ll come back for a second look.

Energy Storage Solutions

Notable names to watch in this space are Stem (STEM) and Fluence (FLNC), both of which we’re avoiding at the moment.

- Fluence Energy – COGS is greater than revenues meaning they don’t have a viable business. Siemens – a related party – accounts for more than half of their revenues. Nearly all revenues come from selling hardware. We might take another look at the company once they can show recurring revenues that constitute a meaningful percentage of total revenues.

- Stem Inc. – Around 96% of revenue comes from the United States and nearly half of 2022 revenues thus far have come from one customer. Nearly 80% comes from reselling hardware from manufacturers like Tesla, Sungrow, and Powin Energy. ARR is growing slowly (5% sequentially last quarter) and overall gross margins were an unimpressive 9%.

Both these business models sound good on paper – sell energy storage solutions, then generate recurring revenues over time – but the reality so far isn’t compelling.

New Battery Technologies

The emergence of special purpose acquisition companies (SPACs) provided a pathway for companies to go public at the peak of inflated expectations. Many promising battery technology companies are now publicly traded companies without a drop of revenue. Below are some names we’re avoiding along with links to articles discussing their technologies.

| Post-SPAC Returns | Market Cap (millions) | Cash & Equivalents (millions) | |

| QuantumScape (QS) | -30% | 3,217 | 1,155 |

| SES (SES) | -57% | 1,536 | 394 |

| FREYR (FREY) | +2% | 1,407 | 416 |

| Solid Power (SLDP) | -72% | 531 | 507 |

| Energy Vault (NRGV) | -72% | 450 | 250 |

| EOS (EOSE) | -89% | 84 | 38.4 |

The above names were all susceptible to hype and saw share prices soar before correcting along with the broader market. Leading the pack is QuantumScape, a developer of solid-state lithium metal batteries for electric cars that’s in bed with Volkswagen. Since its peak of $114 a share, QS shares have fallen -94% as everyone waits for production to commence in 2024. Following one simple rule would have protected investors from such dramatic fallout – never invest in companies unless they have meaningful revenues. No matter how low these stocks sink, there’s no value to be found unless traction has been proven. Raising capital is more difficult in bear markets so there’s also a risk of bankruptcy that needs to be considered now.

Perhaps the brightest star of the bunch is another solid-state battery producer named Solid Power which has handily beat their 2022 revenue estimates of $3 million with year-to-date revenues totaling $7.6 million. While the current market cap is well below our $1 billion threshold, we’ll likely revisit the firm sometime next year provided they exceed $10 million in 2022 revenues. As for FREYR (SemiSolid lithium-ion technology from 24M) and SES (AI, materials, and more), we’re not going to take a second look at either company until they realize more than $10 million in annual revenues.

EOS claims to have built the first commercially available battery that does not have a lithium-ion chemistry. For a company that began shipping systems in 2018, they haven’t made much progress having most recently brought in $6.1 million in revenues for Q3-2022 with a cost of goods sold (COGS) totaling $50 million. That’s not an economically viable business, especially when you consider this $83 million company has just $38 million in cash remaining and a share price that’s flirting with delisting.

Energy Vault has the most unique technology which involves hoisting blocks of concrete into the air and releasing them to create power, the end result being a primitive form of energy storage that competes with the world’s most popular – pumped storage hydro plants. Revenues have started coming in, a respectable $45 million so far this year. Problem is, 97% of that came from one of their investors as part of a $50 million licensing fee (seems like this should be stated as related-party revenues). We may come back around for another look if revenues start to grow outside of their arrangements with investor Atlas Renewable which is largely owned by a Chinese energy firm with plans to develop the project in China.

Our Battery Exposure

Pontificating about the merits of new battery technologies is futile. We’ve read hundreds of articles talking about nano-enabled cathodes, graphene materials, flow batteries, solid-state lithium batteries, and the list goes on. Many of these firms are private, and more examples can be found in our piece on How Lithium-Ion Batteries Will Continue to Improve. Too many battery technology companies have gone bankrupt over the years for us to waste time digging into the story du jour. When a battery tech company has meaningful revenues and appears to be on the cusp of a real growth trajectory, we’ll investigate. This rule applies to many of the stocks we’ve looked at today.

When constructing our tech-stock portfolio, we’ve occasionally chosen to include “placeholders” that are meant to provide exposure to an opportunity that might not yet manifest itself in sufficient form. EnerSys represents such a position, and it’s starting to be a deja vu of the recent piece we did on NextEra Energy: Growth Stock or Value Stock? While revenues may be growing over time giving the appearance of a growth stock, it’s actually a value stock under the hood. Paying a dividend and not giving investors any guidance on revenues (only earnings-per-share) is characteristic of a value stock, not a growth stock.

Holding EnerSys while we wait doesn’t seem like the worst idea. Management anticipates they’ll benefit from the Inflation Reduction Act, while the latest investor deck dedicates a meaningful amount of real estate talking about how they’ll be able to react positively to a possible recession. We’ve conducted our yearly checkup and will continue to hold shares until we find a better substitute. What’s that you say? You know of one? Keep on reading then.

Other Energy Storage Stocks

No energy storage article would be complete without mentioning the hydrogen economy thesis. While we’ve written extensively about the topic over the years, we’re currently working on a research piece that looks at hydrogen from a 20,000-foot view. The idea may not be as green or as economically viable as we’re being led to believe. Stay tuned.

Another idea getting lots of attention from investors is battery recycling. Li-cycle (LICY) dabbles in lithium battery recycling, a domain that’s likely to receive benefits from the Inflation Reduction Act. The most recent Q3-2022 revenues included a complicated downwards adjustment which reflects a strong dependency on commodity prices. We’ll probably wait for the 2022 dust to settle and see how they’re progressing sometime next year.

This article largely surrounds the 16 energy storage/battery stocks found in our tech stock catalog. Consequently, this piece will attract comments around companies we “missed” which is great. Please feel free to suggest firms we ought to look at with a few caveats. No pre-revenue companies, no over-the-counter companies, and no stocks with a market cap of less than $750 million (our market cap cutoff is $1 billion, but we’ll allow for some leeway). Eventually, we’ll find a good way to play the growth of energy storage. Until then, we’ll keep our placeholder – EnerSys – and keep on researching.

Conclusion

Some of our most popular energy storage content has been around solutions providers such as Stem and Fluence. Battery technologies always draw a crowd as well. While the bull thesis for energy storage is apparent, especially in light of the Inflation Reduction Act, what’s lacking is a compelling stock that represents a pure-play way to play the energy storage theme. EnerSys is a placeholder we don’t plan on adding to, nor do we plan on selling the stock until we find a suitable way to play the energy storage thesis.

Share

I see Solid Power shares lost 50% of value for the last month and now trades at $2.8 – very near 52 week low.

Part of it can be attributed to CEO and co-founder Douglas Campbell’s surprise resignation from the company and its board.

Important step for Solid Power will be getting automotive qualification.

Q3 2022 revenue: $2.8M If you annualize it, it makes $11.2M – above Nanalyze threshold of $10M.

We’ll revisit some time next year.

There is nothing new in this article, just some reuse of old info already written before in Nanalyze articles.

So this article is a wasted opportunity as the topic is actually very interesting.

When it comes to Energy Storage topic I like one earlier article:

“5 Energy Storage Systems for the Electrical Grid” (from May 2021).

Also worth mentioning other articles:

“Three Energy Storage Stocks Going Public in 2020” (Dec 2020) ,

“Stem Inc. Stock and Investing in Solar Energy Storage” (Jan 2022) ,

“Solid Power Stock: Pure Play on a Solid-State EV Battery” (Nov 2021).

It’s an aggregation of all the content we’ve created surrounding energy storage stocks so it’s useful to those looking at the bigger picture. We’ve published over 2,200 research pieces and it’s often helpful to aggregate information for any given theme and see where we’re at. And the articles you’ve mentioned are all linked to in this piece so people can dig deeper in areas they so choose. Thank you for the feedback Stan! Negative feedback is always appreciated more than positive.

I am investor in FLNC (Fluence Energy) since $5. Recent price is $21 which is 400% returns from their lows.

I am not sure what kind of research you guys do, you missed 400% returns on this company. And in your article you say “they don’t have a viable business”

Revenue surged to $442 from $188.2 million a year earlier, topping Wall Street estimates for revenue of $359.8 million, according to FactSet.And also their 2022 revenue is $1.2B

You decided to invest in Fluent, cool. We didn’t because of the facts and concerns raised in this article (https://www.nanalyze.com/2021/10/fluence-energy-stock/). We may revisit it at some point when their gross margin turns positive and they have a real business. Last quarter they barely eked out a positive gross margin so we’ll see if that lasts. And we don’t allow links unfortunately.

Hello, I do enjoy reading your articles and analysis, don’t get me wrong. In the link (Energy storage news)

or from fluence website u can see their guidance. They are becoming profitable soon. So a great turnaround story. Some times if you wait until they are profitable, it is too late because stock is already moved 5-10 fold. Similar to Tesla story, it was good investment 3 years back, rather than now. Fluence guided huge revenue as well.

This is from their news.

Fluence yesterday initiated revenue guidance for the 2023 financial year in a range of approximately US$1.4 billion to US$1.7 billion, as well as the aforementioned adjusted gross profit guidance for the year of up to US$100 million

We don’t do the FOMO thing. Ever. If a company doesn’t have a positive gross margin, they don’t have a business. Period. One quarter showing a miniscule gross margin is not some great turnaround story. And whenever people start using Tesla comparisons, it’s a red flag in itself. That’s great you think this is a solid company. Cool. We’ll revisit it when they show some consistent positive gross margins that means they actually have a business. You cannot sell something for less than it costs to produce. That’s not a business.

That’s great they issued some guidance. When they start making some progress down that path, maybe we’ll come around for another look. Again, the FOMO thing doesn’t sell around here. Are we going to capture every bit of alpha known to man? No, and we’re perfectly fine with that. Some people are less risk averse than we are and that’s totally fine.

FLNC announced their quarter result today and increased their revenue guidance once again -$1.6 billion to $1.8 billion and also increased profit guidance and also stock price hit 1 year high.

Your comment about -“You cannot sell something for less than it costs to produce. That’s not a business” I don’t see any logic in it. Lot of growth/ipo companies that’s how they start including Amazon, Tesla were not profitable for years . They don’t make profits from day one.

The reason you’re confused is because we’re not talking about profitability. We’re talking about gross margin. You need to understand that distinction to get the point that’s being raised. Again, for the (checks notes) third time now, we’ll take another look at this stock – and all the other problems it has aside from the gross margin – once they show they’re turning their venture into an actual business.

Good article joe, interesting that you apparently favor solid power, over QuantumScape. I would like to read more of your research into both companies.

During QuantumScape last earnings call it was mentioned that quantumScape is pursuing consumer electronics, as well as the automotive industry. It would be great if they could do some to get some meaningful revenue flowing. I’m looking forward to there next earnings call.

On a different subject, has Nanalyze done any research on MP Materials? MP does kinda qualify as a green stock, but more the thing behind the thing. Rare earth metals.

-Billy E

When looking at any company, revenues are a must. QS still doesn’t have them yet? We’ll take a look once they start selling anything to anyone. As for rare earths or commodities, we don’t get involved in that stuff. They’re just too risky.

Good point in regards to solid power having revenue.

I still like quantumScape over Solid Power for other reasons, but l agree that it is not time to invest in the company. I’m hoping soon that QS Meaningful revenue.

On the topic of MP materials ie rare earth metals, what makes them more or less risky then Cannabis, or wine? Are these not also commodities?

I find MP Materials story, much more compelling.

Very good questions William. Wine is an alternative asset class, and commodities are as well. We’re holding gold which is a commodity. We’re just not interested in covering producers as it’s a massive rabbit hole and there’s too much risk. Exxon and Chevron are two commodity producers we hold and you can see how they react when oil prices become extremely volatile. Lithium, rare earth metals, copper, precious metal miners, this is all stuff we’re not going to be researching and writing about except perhaps occasionally (lithium we’ve covered several times). We hold both gold and wine and we’ve written one piece about wine and none about gold (we’re looking to replace gold with something more relevant to our audience). Art is also a rare commodity we hold as an alternative asset, and we may have written a couple pieces on that. Disruptive tech is largely what we publish articles on, though our YouTube channel gives us more leeway. But, William, you aren’t just some random person asking questions. You’re an annual subscriber, and that means your requests move front of queue. We’ve sent this over to our research queue to see if there’s enough interest to cover MP Materials in a video. We greatly appreciate your financial support!

Thanks Joe, that be cool if I could get your take on MP Materials. It seems to Trade with EV, and lithium stocks, but that may be just coincidence. I’ve been interested in the company for about three or four years. The mine is located across the interstate from a favorite Rock hounding site.