Is Schrödinger Stock Coming Under Pressure From AI?

Table of contents

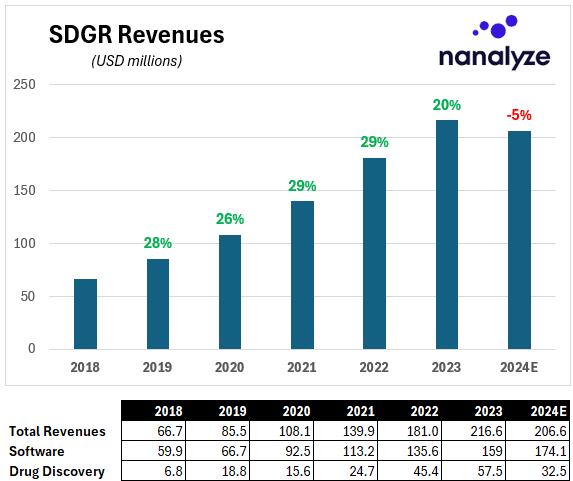

Let’s be clear about one thing. Schrödinger (SDGR) isn’t an AI stock. That’s what they emphatically told us the last time we implied such a thing, and it’s admirable in an environment where every single company is plastering “generative AI” across their investor decks in hopes of attracting more dollars. What Schrödinger does is utilize software simulations to help drug developers better predict which novel molecules will successfully pass the FDA drug approval gauntlet. Their business model captures value from software licensing annual contracts (software), and downstream royalties and milestone payments (drug discovery). After showing strong double-digit growth for the past five years, Schrödinger may now see negative growth based on the middle of their 2024 guidance.

And that coincides perfectly with our annual check-in with one of the 37 disruptive tech stocks we’re currently holding.

Software Growth Stalls

The drop in revenue growth is a concern, especially considering that everywhere we look software is transforming how companies do business. In SDGR’s year-end earnings call, the first analyst out of the gate nailed it with an excellent question. How should investors think about SDGR’s software guidance of 6% to 13% given a) the company’s past strong revenue growth and b) the recent industry-wide AI momentum?

These questions are important because we can’t answer them looking in from the outside. While drug discovery revenues should be lumpy, software is Schrödinger’s bread and butter, yet its growth has been on the decline over the past several years. That becomes apparent when we isolate software revenue growth over the past six years (2024 estimates reflect midpoint of guidance).

The ground truth of any disruptive technology is always revenue growth which is a proxy for market share being captured. During their recent earnings call, Schrödinger’s opening remarks pointed to back-loaded software contracts in 2023 as a reason for soft growth in 2024, but the much bigger question is why software revenues have been steadily declining over time.

Schrodinger’s answer was all about “confidence” and “opportunities.” Those and $5 might get you a large fry at Mickey D’s. They talk about upselling customers spending more than $1 million but less than $5 million, so retention rate is a key metric to watch here (more on this in a bit). A focus on milking more revenues from top customers makes lots of sense when you consider the following statement:

In 2023, all of the top 20 pharmaceutical companies, measured by 2022 revenue, licensed our solutions, accounting for $71.8 million, or 45%, of our software revenue in 2023.

Credit: SDGR 10-K

The pervasiveness of Schrödinger’s solution is a double-edged sword. On one hand, it shows their platform is a must-have for the world’s largest pharmaceutical companies, but on the other, it implies they’ve already sold their product to everyone who matters. This is why it’s important we see they’re able to extract more revenue from existing clients, especially large ones.

Net Retention Rates

A deeper dive into SDGR’s retention metrics shows a decreasing emphasis on smaller customers and a focus on upselling larger ones. That’s not by design since apparently smaller customers have been having issues paying the bills.

…we are seeing some of the turmoil associated with companies running out of capital, shutting down R&D, getting merged, acquired, etcetera. We think that that’s been a drag on our growth in 2023. We think we’re planning on that consisting in 2024…

Credit: SDGR Q4-2024 Earnings Call

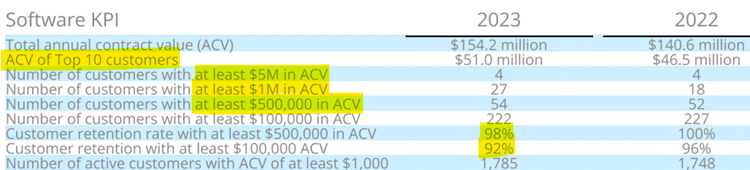

Perhaps this led to Schrödinger’s decision to break out “retention rate” into two different buckets as seen below (this is the equivalent of gross retention rate in the SaaS world – in other words, percent of customers who didn’t cancel).

Customers spending between $100,000 and $500,000 on the platform declined last year while customers spending more than $500,000 declined marginally. Schrödinger thinks the real upselling can happen between a $1 million and $5 million annual contract value (ACV), and that’s reinforced by their largest software customer spending just over $24 million in 2023 on software alone. We’ll assume that’s a big pharma company, and that the other 19 top pharma clients using Schrödinger’s platform might be capable of similar run rates. In other words, there seems to be plenty of upside from existing large customers.

Drug Discovery Revenues

Schrödinger provides a metric titled, “ongoing programs eligible for royalties” which dropped from 17 to 15 last year. Coincidentally, their “drug discovery” revenue guidance also fell by 43%. One analyst questioned if this drop was a “organic shift in expectations versus a systematic change,” citing a comment Schrödinger made in early 2023 about “a shift in the methodology and guidance” for drug discovery revenues. Looking at past guidance vs actuals provides some insights into this comment.

Historically, the company provided a broader range of possibilities while that range has now narrowed for 2024 guidance implying they’re more confident in the numbers. The 2023 miss (by 18% on the lower end of guidance) implies they weren’t capable of identifying a worst-case scenario and that this revenue stream is more unpredictable than imagined. Perhaps that’s the result of the two “ongoing programs eligible for royalties” disappearing. Better to set expectations narrow and realistic instead of broad and optimistic, right?

Schrödinger’s commentary affirms this when they talk about several changes in how they provide drug discovery guidance. Since it’s “challenging to provide guidance that incorporates the uncertainty associated with partners’ advancing programs that will trigger milestones to our benefit,” they’ve now taken these milestones out of guidance. Hopefully, that’s because of uncertain timing, not decreasing likelihood. They also stopped “including any allowances or estimates for new business development transactions, that is, new collaborations with new partners or partnering proprietary programs.” Current guidance therefore reflects, “the most likely range of outcomes at the beginning of the year.” If they revise guidance positively during the year, that can only serve to benefit their volatile share price.

Schrödinger and the AI Evolution

In our last article on Schrödinger titled Schrödinger Stock: Drug Discovery Platform Making Money we touched on a topic raised by our astute Premium subscribers, and also by an analyst in the latest earnings call. How will the recent AI evolution affect the competitive landscape? How will Schrödinger stay ahead of their competition when AI is expected to solve every problem known to man?

The CEO ran with that question and talked about “nice progress in AI on structural biology” which is resulting in a bigger supply of protein structures that are the primary input to SDGR’s “physics-based methods.” More inputs mean a larger number of targets of interest which helps fuel demand for Schrödinger’s software. As for staying competitive, the CEO seemed mildly exasperated when explaining – yet again – that AI algorithms have no value without training data, and that’s what Schrödinger’s platform provides. He goes on to say, “we see no efforts in the space that are competitive with our physics-based approaches.” Let’s certainly hope so.

Conclusion

Software’s declining growth rate is our biggest concern, more so than one year of declining revenues. The steady growth of larger customers is reassuring, but that’s being offset by smaller customers bailing for any number of reasons. The company’s hesitance to provide “drug discovery” revenue guidance is understandable – we can think of these as bonuses – but software sales need to start reflecting the supposed uplift Schrödinger’s CEO expects to see from today’s advancements in AI biology.

Share

Don’t I remember – would not bet on it – that these folks offered clients SaaS, based on computerized physics to ‘test run’ would-be therapeutic drugs. They’ve tried. They have failed. I think they are just an ‘add on’ which universities and Large-Pharma (some are dropping out) feel they should have.

Don’t tie your capital up for another 12 months. If you want to lose time and money look at OCEA.

Hey Mark. Always good to hear your thoughts. Double digit growth for the past five years wouldn’t be considered failing, but slowing growth is a concern – always. As risk-averse investors we move very slowly and thoughtfully when we make investment decisions so we’ll see how 2024 progresses for the company.