What is the Best Desalination Stock to Invest In?

Table of contents

Those of us who engage in the sport of doom scrolling are spoiled for news content these days. Headlines proclaim that the world is teetering on the precipice from any number of political, social, natural, and environmental disasters. The last one on that list has given rise to various green technologies that have attracted investors keen on greening their portfolios and saving the planet. But as we’ve repeatedly pointed out, many of these nascent industries are not ready for prime time. Hydrogen? Seems like a pipe dream. It’s still way too early to invest in emerging technologies like carbon capture. And even stocks in established industries like solar and wind are taking a beating these days.

A Quick Recap of Desalination Stocks

Yet many of our readers remain interested in investing in green technologies despite the risks. One of our most popular articles over time was a piece on investing in desalination companies that we wrote nearly a decade ago. Since then, we have often revisited the water tech investment theme from different angles but occasionally keep searching for pure-play desalination stocks. These are companies whose primary business is the design, development, and/or deployment of technology to turn saltwater into potable water. The number of desalination plants has grown tremendously over the last 60 years.

Most of the companies responsible for designing and constructing these facilities tend to be global engineering and construction firms; there appear to be very few pure-play desalination stocks. In 2020, the number dropped by one when Culligan Water acquired AquaVenture Holdings, which offered a water-as-a-service business model by retrofitting desalination plants. The only other pure-play reverse osmosis desalination stock still in play that we previously covered is Caribbean-based Consolidated Water (CWCO). The company has increased annual revenue by 27% to $94 million since that article in 2019, as well as nearly tripled its market cap to about $600 million. It recently scored a $200+ million contract to build its 24th desalination plant and first in the United States.

Despite the company’s growth, CWCO is still well below our $1 billion market cap cutoff before we will invest in any company. Consolidate Water also pays a dividend, which siphons money away from growth, which is largely what we’re chasing with tech companies. Fear not, fearless investor, for we recently came across another pure-play desalination stock that does (barely) cross that threshold. But first let’s revisit why investing in desalination technology is both appealing and risky.

Deconstructing the Desalination Investment Thesis

Earlier this year, the United Nations reported that the global demand for freshwater will exceed supply by 40% by 2030. A recent report by the New York Times found that many of the underground aquifers that supply 90% of United States’ water systems are being severely depleted. Blame climate change, blame industrial agriculture, or blame your crazy uncle. It really doesn’t matter at this point the reasons why the world is running out of fresh water. (Technically, the amount of freshwater in the Earth’s hydrological cycle never changes. However, our ability to access it and efficiently use it has been disrupted due to pollution, runoff, and population pressures, among other challenges.)

The appeal of desalination in the face of these challenges is obvious: About 97% of the world’s H20 resources is saltwater. Technologies like reverse osmosis (RO), which pumps seawater through semipermeable membranes to remove salts and impurities, are relatively straightforward. But such systems are extremely energy intensive and costly to build and maintain. For example, the high pressures required to make RO pump systems operate require a ton of energy, not to mention disposal of the brine left behind. One estimate is that a third of the lifetime costs of a desalination plant is energy. Thermal desalination, which works by evaporating out impurities from saltwater before condensing back into freshwater, requires even more energy.

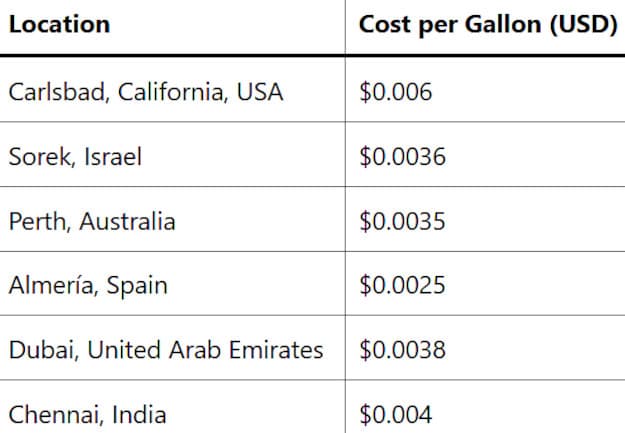

Unlike how cost comparison data between renewable energies and fossil fuels are readily available, we found it difficult to find reliable numbers that compare various desalination technologies and conventional water production. (The above table comes from a website that’s allegedly run by a PhD student studying sustainability, for example, who does not identify himself. The info seems legit.) Part of the reason is that costs are highly variable based on location, technology employed, and local energy prices. Another source claims U.S. consumers pay $2 per 1,000 gallons for conventional water vs $2.50 to $5 per 1,000 gallons from desalination. In some ways, the cost may not matter as people become more desperate for freshwater. Case in point: One fast-growing Arizona town is contemplating piping desalinated water (uphill) from Mexico.

About Energy Recovery Stock

There is obviously some economic incentive to make desalination more energy efficient aside from building ginormous golf courses in the desert. One expert out of Purdue said that “even small improvements to the process – a few percentage points of difference – can save hundreds of millions of dollars.”

That brings us to Energy Recovery (ERII), a San Francisco Bay area company that has been around for more than 30 years. It develops energy recovery devices, pumps, and related equipment designed to lower the energy cost of desalination plants. The company claims its technology has saved customers nearly $4 billion in energy costs. Its products are used globally to produce more than 28 million cubic meters of water per day, which would be enough to provide the United States with 14% of its total daily water needs.

Average annual revenue growth since 2015 has been 16%, with 2022 revenues of about $126 million, though revenue growth this year is trending lower. In addition, Energy Recovery stock hasn’t exactly recovered a great return on investment since its IPO way back in 2008. Shares are up just +50% compared to +500% for the Nasdaq. Is there any reason to consider this company?

What Does Energy Recovery Do?

Let’s first figure out what Energy Recovery even does. We’re MBAs, not engineers, so we’ll keep this brief. The company’s flagship technology is the PX Pressure Exchanger, which uses a rotating wheel-like device that transfers pressure from a high-pressure fluid stream to a low-pressure fluid stream, without mixing the fluids or consuming any electrical power. Basically, it recovers the pressure energy that would otherwise be wasted to help power the desalination process.

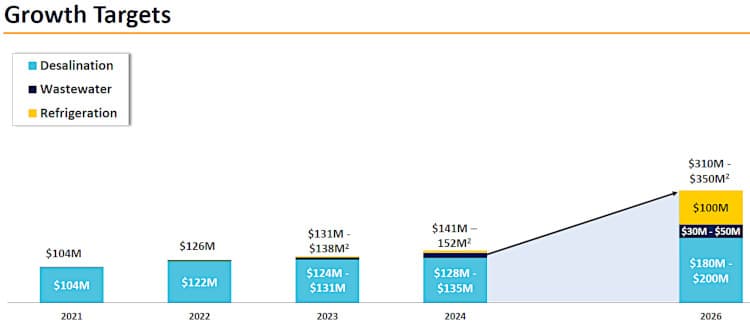

Energy Recovery also designs and manufactures other components of these desalination systems such as pumps and turbochargers. It sells these products across three different markets: megaproject, original equipment manufacturer, and aftermarket. As the name implies, megaproject customers represent large-scale projects with total capital investments of up to $1 billion. Revenue from megaprojects can range from about $1 million to $21 million, and accounted for about two-thirds of revenue in 2022.

In addition to desalination, Energy Recovery products are also used in wastewater facilities. In fact, recycling wastewater for agricultural, industrial, and residential uses is expected to be big business. One estimate says the cost of producing non-potable recycled water can be as low as $0.32 per cubic meter, and potable water $0.45, compared with more than $0.50 for desalination. While Energy Recovery expects to grow that segment of the business in the future, management expects much of its near-term growth to come from refrigeration.

The world is still trying to wean itself off of high-polluting refrigerants like hydrofluorocarbons. One alternative is a system designed around CO2 refrigerants. Energy Recovery is leveraging its PX technology to develop products for this market and recently rolled out the PX G1300 to help lower the energy cost of CO2 refrigeration systems. One of the initial use cases is supermarkets.

Should You Buy Energy Recovery Stock?

Energy Recovery is certainly an intriguing play on water tech and desalination investment themes, with additional exposure now to the more general “save the planet” vibe with the introduction of the PX G1300. However, we wonder how quickly this business will ramp up given how notorious companies are about adopting more rigid environmental standards without lobbying for waivers over the next few decades.

We are quite impressed with the company’s gross margin of nearly 70%, especially since it designs, produces, assembles, and tests its products in its one California facility, including what it calls advanced ceramics manufacturing. The closed-loop nature of its products is also reflected in how the company manufactures its high-purity alumina ceramic components. For example, the company collects powder created from their manufacturing to be reused. That seems like the sort of smart engineering approach that gets a hardware-centric company like Energy Recovery to a 70% gross margin. Also interesting is that the company is very much a Made in the USA outfit, but just 1% of its revenues come from the United States.

But we also have some concerns: Customer concentration is often a problem in niche industries like desalination, and we find that to be the case with Energy Recovery. Just three customers accounted for 44% of revenues in 2022 and nearly half of revenues the year before came from only four customers. Investing in Energy Recovery is really an investment in the company’s particular technology platform than more broadly on desalination. While it lists just three main competitors, one of them is Flowserve (FLS), a nearly $5 billion company by market cap that produces all sorts of pumps and pipes across industries that go with the flow, including energy recovery devices for desalination plants. The long-term upside here sounds like pumping water uphill.

Conclusion

The desalination market is potentially huge but we keep coming up high and dry when it comes to finding a pure-play desalination stock we would want in our Nanalyze Disruptive Tech Portfolio. Frankly, the technology itself is not really “disruptive.” One other option is to check out Xylem (XYL), a smart water technology company that we profiled last year which sits somewhere between growth and value. It now bills itself as the world’s largest pure-play water technology company after its $7.5 billion acquisition of Evoqua Water Technologies. Until then, fix that leak. We’re going to need all that water.

Share

Thanks for this well written overview. Do you know a German company which is called KSB? It passed the 1 bn-threshold marketcap early this year.

https://www.ksb.com/en-global

Your comment was very useful, thank you. Looks like KSB has quite small exposure to desalination equipment, but it’s an interesting business nonetheless. Didn’t know they had such a strong market share in pumps.