A Caribbean Desalination Stock to Invest In

Table of contents

Water is one of the most important prerequisites for life. It can’t be created nor destroyed, but it can be damaged or unusable to begin with. While the Earth has lots of water, only 2.5% is freshwater that we can use for drinking. Around 70% of that freshwater is contained in glaciers, ice, and snow, so this leaves less than 1% of Earth’s water useful and accessible to humans. The distribution of that precious resource isn’t evenly allocated across inhabited regions. According to the UN’s Food and Agriculture Organization, 33 countries depend on other countries for over 50% of their renewable water resources.

Right away we can see that India is in some serious trouble with 21 major cities slated to run out of groundwater next year. At the moment, 844 million people or 11% of the global population lack access to safe freshwater, something that costs the global economy around $260 billion every year. The investment thesis for water pretty much spells itself out, and perhaps the most obvious solution is to look towards desalination – the process of turning seawater into freshwater. The technology has been available since the mid-20thcentury but it only became widespread in recent years.

Growth of the Desalination Market

Several factors are responsible for the recent rapid growth of desalination. Rising population in water-stressed areas combined with severe droughts in previously well-supplied regions drive demand while the costs of desalination have come down as the technology matures. Freshwater from desalination plants is still expensive (about double the cost of natural freshwater in the case of a plant near San Diego), but in many cases, the population doesn’t have a choice. At the moment, 4% of the global population get their water from desalination plants so it’s still a relatively small contributor. This means there is lots of room for growth.

The global desalination market is expected to grow by 7.8% annually between 2018 and 2025, surpassing $27 billion by the end of the period. We’ve previously looked at the top-10 and top-20 engineering, procurement, and construction contractors for desalination plants to see if any of them provide pure play exposure to this emerging industry. We concluded that most of these companies were major global construction, engineering, or water treatment players with many other divisions, so none of them qualified as pure play in the desalination business. Looking further, we’ve found three companies specialized in the field: AquaVenture Holdings, NanoH2O, and Oasys Water. NanoH2O has been acquired by LG Chem, and Oasys hasn’t made it to IPO yet, which leaves AquaVenture as the only pure play stock for retail investors. Today, we’re going to talk about a NASDAQ-listed pure-play desalination stock called Consolidated Water.

A Pure-Play Desalination Stock

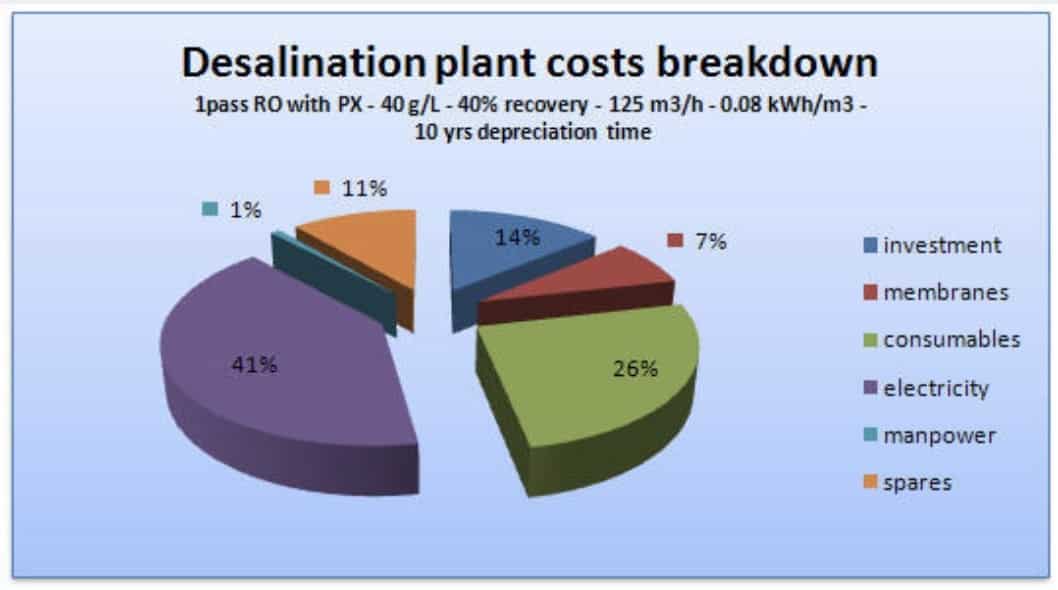

![]() Consolidated Water (CWCO) was founded in 1973 as a private water utility company in Grand Cayman, the largest island in the Cayman Islands group. The company installed its first reverse osmosis desalination plant in 1989 and went public on the NASDAQ stock exchange in 1995. Reverse osmosis, the technology that CWCO now uses in all its operations, involves pumping saltwater through one side of a purification membrane after which freshwater comes out the other side. This technology is the gold standard for the desalination industry and on average produces one gallon of freshwater from every two gallons of saltwater used. The downside is that the process requires a great deal of electricity to pump the saltwater through the membrane, something that’s clearly reflected in the cost breakdown for a desalination plant.

Consolidated Water (CWCO) was founded in 1973 as a private water utility company in Grand Cayman, the largest island in the Cayman Islands group. The company installed its first reverse osmosis desalination plant in 1989 and went public on the NASDAQ stock exchange in 1995. Reverse osmosis, the technology that CWCO now uses in all its operations, involves pumping saltwater through one side of a purification membrane after which freshwater comes out the other side. This technology is the gold standard for the desalination industry and on average produces one gallon of freshwater from every two gallons of saltwater used. The downside is that the process requires a great deal of electricity to pump the saltwater through the membrane, something that’s clearly reflected in the cost breakdown for a desalination plant.

CWCO has a portfolio of 13 working desalination plants in the Caribbean and that famous Australian resort town called Bali, and is continuously looking for expansion opportunities in markets that are under significant water stress. For example, the Caribbean faces geographic, industrial, and infrastructural issues compounded by drought and extreme weather. As for Bali, the freshwater supply has been abused by its booming tourism industry.

Perhaps the most promising growth for CWCO can be found in Mexico where they’re currently constructing the largest desalination plant in the Western Hemisphere. Mexico is also stressed for water, facing simultaneous increase in water demand and water losses due to the rapid deterioration of its water infrastructure. At the moment, CWCO’s operating desalination plants have a total production capacity of 25.5 million gallons per day which is enough to supply 425,000 people with an average US consumption pattern, so roughly 10% of the Caribbean population of 44 million.

Stable Finances and Strong Revenue Growth

Most of CWCO’s revenues come from two main divisions.

- Retail Water Operations, responsible for 39% of revenues, produces and supplies water to end-users including residential, commercial, and government customers in the Cayman Islands and Bali.

- Bulk Water Operations, generating 47% of revenues, produces and supplies water to government-owned distributors in the Cayman Islands and the Bahamas.

The rest of the company’s income is generated by constructing, selling, and operating desalination plants and other water-related products for third parties. Based on its activities, it’s safe to say Consolidated Water is a pure-play desalination stock.

CWCO closed a successful year in 2018. The company has increased both revenues and operating costs by about 10% compared to the previous year. Thanks to keeping administrative expenses flat, CWCO has posted a net profit of $11.3 million for 2018, 84% higher than in 2017. Share prices of the $217.5 million market cap company have increased by 9.8% over the past rolling year (against the NASDAQ Composite’s +4.4%), and 36.6% over the past five years (against the NASDAQ Composite’s +84.8%). CWCO has been distributing dividends of varying frequencies and amounts since 1997 and the stock has a current dividend yield of 2.37% with a payout ratio of 46.58%.

Future Expansion

All things being equal, a low payout ratio means the remaining profits can get plowed back into growth. Over time, CWCO has accumulated profits to finance expansion. At the beginning of 2018, the company had $45.5 million in cash which means it doesn’t have to finance any debt and can invest in new desalination projects – like the massive multi-year desalination project in northern Baja California, Mexico.

In 2016, CWCO joined a consortium of water treatment and desalination companies to successfully bid for a government project involving the design, construction, financing, and operation of a desalination plant with a capacity of up to 100 million gallons per day – about four times the capacity of CWCO’s total portfolio. The new plant should be functioning at full capacity by 2024 with CWCO’s subsidiary acting as minority owner and operator. Depending on how other consortium members exercise their ownership options, CWCO will own 25-35% of the plant at the project’s conclusion.

While the new Baja California plant presents an attractive growth opportunity, it is also a business risk. The public-private partnership agreement will only become effective when the necessary payment trusts, guarantees, and credit lines have been established, water sale agreements and debt financing are in place, and the consortium has obtained all of the rights of way required for the aqueduct. In case the project falls through, the $51.4 million CWCO has already invested in land, rights of way, equipment, and development since 2016 will lose a significant amount of value.

Conclusion

We haven’t been able to find many companies offering the sort of pure-play exposure to desalination that CWCO does. Still, CWCO’s operations are small compared to the massive desalination projects that can be found in the Middle East. For example, the largest desalination plant near Riyadh, Saudi Arabia, has an output of 273 million gallons per day – about ten times CWCO’s entire capacity. Investors will be looking for CWCO to grow quickly given the ample growth opportunities in desalination across the globe.

If the pending construction project in Mexico materializes, CWCO will be joining the big leagues and executing it with the likes of French conglomerate Suez. Besides opening new plants, CWCO also renovates its old ones to achieve better production efficiency and lower electric power consumption, strengthening its bottom line. As the outlook on our natural water resources becomes increasingly grim, CWCO will provide a safe haven to both consumers and investors.

Share