10 Artificial Intelligence Startups in Insurance

Table of contents

With somewhere around 2,000 artificial intelligence (AI) startups out there, applications have been identified across every single sector you can think of. While few industries are as mundane as insurance, it starts to become interesting in the context of using AI in insurance. On one hand, the predictive powers of AI threaten to all but replace human actuaries resulting in reduced labor costs and more accurate predictions. On the other hand, autonomous cars threaten to decimate traditional auto insurance premiums.

The insurance industry is roughly divided into Life, Health, and Property & Casualty (P&C). We’ve thinly touched on technology innovation in P&C with an article about Metromile with its “pay-as-you-go auto insurance coverage”. Metromile’s technology automates the collection of statistics like distance traveled or driver behavior to rationalize auto insurance coverage. Why is this so meaningful? Take the below excerpt from a recent report by McKinsey titled “Time for insurance companies to face digital reality“:

US auto insurers have already lost on average $4.2 billion in underwriting profit a year over the past five, with expenses and losses consistently outweighing premiums. They should expect further annual profit declines of between 0.5 and 1 percent if they fail to use digital technology to improve efficiency and effectiveness.

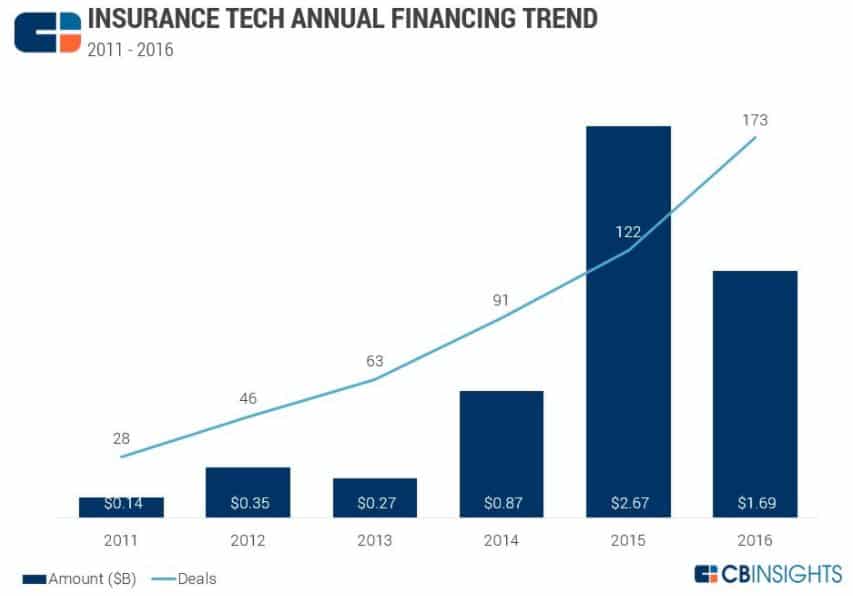

So essentially, auto insurance companies are not operating in a sustainable fashion and the only way we can resolve that is through technology. Maybe that’s why venture capitalists are pouring money into Insurance Technology or “InsurTech”. Startups like Metromile are part of the growing trend of investments into “InsurTech” as seen below:

Let’s have a look at some examples of startups that are leveraging artificial intelligence across all areas of the insurance industry.

Instant home insurance

![]() Founded in 2015, New York-based startup Lemonade has taken in $60 million in funding so far from the likes of Google, Allianz, and Sequoia Capital. Lemonade is a licensed insurance carrier offering insurance to renters and homeowners exclusively through a chatbot app for smartphones. It takes about 90 seconds to get insured and about 3 minutes for claims to be paid. The economical subscriptions of just $5 monthly for renters and just $25 monthly for homeowners are attracting clients from other insurance carriers like these:

Founded in 2015, New York-based startup Lemonade has taken in $60 million in funding so far from the likes of Google, Allianz, and Sequoia Capital. Lemonade is a licensed insurance carrier offering insurance to renters and homeowners exclusively through a chatbot app for smartphones. It takes about 90 seconds to get insured and about 3 minutes for claims to be paid. The economical subscriptions of just $5 monthly for renters and just $25 monthly for homeowners are attracting clients from other insurance carriers like these:

Lemonade uses premiums pooled from each peer group to pay for the group’s claim and gives the leftover money to the customers’ common cause. Reinsurance is used to cover cases of claims exceeding whatever is left in the pool. Big data and machine learning algorithms help combat fraud.

Update 04/11/2019: Lemonade has raised $300 million in Series D financing to help Lemonade expand beyond the U.S., with sights set on Europe as a first step. This brings the company’s total funding to $480 million to date.

Handwritten paperwork to digital

![]() Founded in 2011, it’s a miracle that Oakland California startup Captricity hasn’t had the $52 million they raised jacked yet based on where they decided to set up camp in. We first talked about this amazing startup in a past article about “What Jobs will Robots and AI Do in The Future?” in which we remarked that Captricity has developed machine learning algorithms that can extract and transforms data from handwritten and typed forms at a +99.9% accuracy. Here are a few comments about Captricity’s value proposition from Forrester analyst Ellen Carney:

Founded in 2011, it’s a miracle that Oakland California startup Captricity hasn’t had the $52 million they raised jacked yet based on where they decided to set up camp in. We first talked about this amazing startup in a past article about “What Jobs will Robots and AI Do in The Future?” in which we remarked that Captricity has developed machine learning algorithms that can extract and transforms data from handwritten and typed forms at a +99.9% accuracy. Here are a few comments about Captricity’s value proposition from Forrester analyst Ellen Carney:

For one carrier, the company has digitized a half million new business applications, speeding up the quote-to-bind process and producing a 50% drop in staffing costs. For New York Life Insurance, Captricity extracted cause-of-death data from 10 years of paper death certificates that the insurer is using to refine its life actuarial models.

Capturing and analyzing historical policy data improves underwriting accuracy which is why 50% of the top U.S. insurers now use Captricity.

Quantifying cyber risk

![]()

Founded in 2014, Silicon Valley startup Cyence has taken in $40 million in funding so far to develop an analytics platform that can quantify the financial impact of cyber risks. Insurance is all about managing risk, and one of the biggest operational risks companies face is that of cybersecurity. A single hacker can steal information that might be worth billions of dollars to a company. As an insurance company, how can you offer a policy that covers such a problem if you have no way of assessing the risk that you’re taking? Cyence offers the industry’s first platform that quantifies cyber risk using probabilities and dollars. The volume of big data that would need to be analyzed in order to come up with such information is where the machine learning algorithms come in to play.

Monitoring drivers via smartphone

![]()

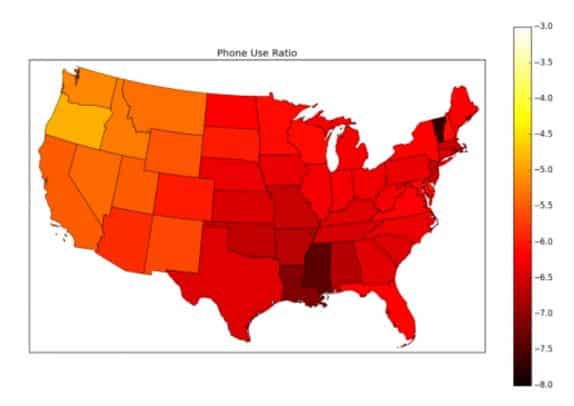

Did you know that 1 in 4 collisions result from phone use while driving? Founded in 2013, San Francisco startup Zendrive has taken in $20 million to develop a technology that uses sensors in your smartphone to measure and to improve driving behavior. “I’ll never install such an app” you might say. Well what if by installing that app you received a 25% discount on your insurance premiums? Since the app reduces the probability of collision, insurance premiums can be lowered and everybody wins. Machine-learning algorithms then turn that sensor data into actionable safety insights like “DON’T USE YOUR PHONE WHILE YOU ARE DRIVING!”. Zendrive did a 3-month analysis of 3-million anonymous drivers, who made 570-million trips and covered 5.6-billion miles. What they found was drivers use their phones during 88 out of 100 trips. Here are the states where the worst offenders reside:

For those readers who are geographically challenged or color blind, essentially this tells you to stay the fcuk off the roads in Mississippi and Vermont.

Property insurance aided by satellite pictures

![]() Founded in 2014, Silicon Valley startup Cape Analytics has taken in $14 million so far to develop a service for property insurers that combines machine learning with computer vision and geospatial imagery to do things like analyze roofs of houses for material type, condition, and building footprint. Anyone can plug into their data feed of comprehensive property attributes via an API and then use it to improve the underwriting process by increasing quote speed and refining quote accuracy. The existence of solar panels, skylights, or chimneys is also relevant to insuring a property and can easily be identified by the system.

Founded in 2014, Silicon Valley startup Cape Analytics has taken in $14 million so far to develop a service for property insurers that combines machine learning with computer vision and geospatial imagery to do things like analyze roofs of houses for material type, condition, and building footprint. Anyone can plug into their data feed of comprehensive property attributes via an API and then use it to improve the underwriting process by increasing quote speed and refining quote accuracy. The existence of solar panels, skylights, or chimneys is also relevant to insuring a property and can easily be identified by the system.

Auto insurance claims management

![]()

Founded in 2012, London based startup Tractable has taken in $9.9 million in funding so far to create deep learning algorithms that can give cost estimates for auto insurance claims. The collision repairer uploads an estimate and pictures to the claims management system and the AI algorithms compare the pictures and the cost estimate to make sure everything is in order. This reduces the cycle time from days and weeks to minutes, results in more consistency, and no longer requires an expensive human claims handler to be involved in the process.

Update 06/16/2021: Tractable has raised $60 million in Series D funding at a post-money valuation of $1 billion to help build out better, AI-based techniques of processing and parsing pictures that are taken on smartphones. This brings the company’s total funding to $119.9 million to date.

Comparing commercial policies

![]()

Founded in 2011, the RiskGenius product is the second to be launched by the ClaimKit team which has taken in $3.3 million in funding so far. The original product, Privity, is a claim document management tool built by two claim attorneys who were tired of messy claim files and bad software. The RiskGenius Platform uses machine learning to break down insurance policies from any number of providers so that they can easily be compared. Apparently, the traditional method of comparing commercial policies is a whole lot of manual labor. Don’t have time to go through all that fine print to look for clauses that might make a huge difference to your unique case? Now with RiskGenius, users can easily perform policy analysis without having to get the entire industry to agree upon some sort of strict formatting definition beforehand.

Identifying fraudulent claims

![]()

Founded in 2013, Paris startup Shift Technology has taken in $11.8 million in funding so far to develop an AI-powered cybersecurity solution to detect fraud in the insurance industry using big data and machine learning algorithms. In Europe, fraudulent claims are estimated at 10% of all total claims expenditures. As of today, the system has processed over 78 million insurance claims and is said to have a 75% accuracy which will only improve with time as AI tends to do. If the name sounds familiar, that’s because Shift Technology was also featured in our recent article on “6 AI Cybersecurity Startups Keeping You Safe“. The technology works on both health insurance claims and P&C claims.

Update 03/04/2019: Shift Technology has raised $60 million in Series C funding to further grow their solution that helps detect fraudulent insurance claims. This brings the company’s total funding to $99.8 million to date.

Claims management for insurers

![]() Remember the startup we highlighted earlier, Tractable, that lets the collision repairer upload photos of damage for machine learning algorithms to assess? Well, this startup wants to put the end customer in charge of the whole claims process for auto accidents. Founded in 2016, UK-based startup RightIndem has taken in $1 million in funding to create an insurance claims platform for insurers accessible via app. The service allows insurance customers to make claims and have them processed at their pace which shortens claim cycles and improves customer satisfaction. The service covers 3 main categories of the customer claims timeline which includes Notification (Virtual Damage Assessment & Electronic Notification of Loss), Core Claim (Total Loss, Repair, & Smart Repair), and Settlement (Payments & Replacements). They claim that their “AI engine performs millions of calculations a second to deliver the right outcome” so it should get better over time then as well.

Remember the startup we highlighted earlier, Tractable, that lets the collision repairer upload photos of damage for machine learning algorithms to assess? Well, this startup wants to put the end customer in charge of the whole claims process for auto accidents. Founded in 2016, UK-based startup RightIndem has taken in $1 million in funding to create an insurance claims platform for insurers accessible via app. The service allows insurance customers to make claims and have them processed at their pace which shortens claim cycles and improves customer satisfaction. The service covers 3 main categories of the customer claims timeline which includes Notification (Virtual Damage Assessment & Electronic Notification of Loss), Core Claim (Total Loss, Repair, & Smart Repair), and Settlement (Payments & Replacements). They claim that their “AI engine performs millions of calculations a second to deliver the right outcome” so it should get better over time then as well.

Learning about you from your face

![]() This last startup has taken in an undisclosed amount of funding to do something that sounds pretty far-fetched frankly. Founded in 2014, North Carolina startup Lapetus Solutions has taken in an undisclosed amount of funding to develop machine learning algorithms to read your face. You didn’t think you could just lie about smoking now, could you? Their platform CHRONOS combines event data with facial analytics and demographic information to allow for predictive analysis of life events. Lapetus Solutions’ technology is essentially assessing your health and life span by analyzing your face giving a whole new meaning to face value.

This last startup has taken in an undisclosed amount of funding to do something that sounds pretty far-fetched frankly. Founded in 2014, North Carolina startup Lapetus Solutions has taken in an undisclosed amount of funding to develop machine learning algorithms to read your face. You didn’t think you could just lie about smoking now, could you? Their platform CHRONOS combines event data with facial analytics and demographic information to allow for predictive analysis of life events. Lapetus Solutions’ technology is essentially assessing your health and life span by analyzing your face giving a whole new meaning to face value.

Conclusion

We wouldn’t be surprised if there are 100s of startups trying to create efficiencies in the archaic insurance industry using the powers of artificial intelligence. Since the industry is so far behind the times, it wouldn’t be surprising to see “InsurTech” firms create dramatic efficiencies using traditional technologies. This means that for startups that aren’t validated by a notable tech VC, just take all those “machine learning labels” with a grain of salt.

Share

How can I contact these companies about an investment ?

Hi John,

Looks like you’re a VC firm? In that case, you would need to reach out to each company and inquire. They’re all at differing stages of funding and it’s hard to say who is looking to raise next. Note that all these companies will read this article so it’s a good place to have your feelers out. Some might reach out to you proactively!

How can I contact these companies about an investment ?

Hi, I am the founder and CEO of Infinilytics. Our product which has been implemented in insurance companies ranging from life and P&C to Govt forensic analysis of fraudulent claims. Our product smartC is AI based advanced analytics solution that can quickly validate genuine claims while flagging questionable claims patterns using cognitive behavior analysis and has been saving insurance companies claim costs while improving speed to pay genuine claims. We were the pioneers of fast tracking claims using AI patent pending inbuilt algorithms that can match questionable patterns to common insurance fraud schemes. We also read data from forms and use with our analysis. We have been in the market a little longer than some of the companies above. We focus on our customers and our product development is done by industry practitioners and thought leaders making us very unique. We would like to be included in your research going forward

Thank you for the comment Sri! We appreciate you bringing your firm to our attention.

In this article we tried to get a flavor of what’s out there and what we found are TONS of startups attacking the insurance industry. We’ve noted your firm. Would you mind dropping us an email which lets us know about who is backing you? Thank you!

Hi, I am an business developer for Salviol Ltd. (not on the above list), however we have done AI based underwriting for large french based insurer and we have also processed over €4B claims for various insurers. We see that supervised AI has much better results as unsupervised. Clients usually give us policies and claims for several years – we build a model based on that. Then client gives us only policies and no claims for last year and we have to show which policies will turn to fraud. We usually catch around 50 % of policies with fraud elements. Client can easily check our precision and recall rate by checking real claims.

We have tried unsupervised AI but the results were poor.

Hi Matt,

Thank you very much for the comment. This is really interesting.

So how can you tell looking at a policy that it will have more fraud than other policies? You refer to these as “fraud elements”. This concept is fascinating but a cursory look at your website didn’t show any specific examples of how this works. The Tech Crunch article wasn’t overly edifying either. If you have a case study or you can spare any technical details then we’d love to possibly cover this in a future article once we understand how it works. Thank you for taking the time to comment!

Hi, I am the founder and CEO of Infinilytics. Our product which has been implemented in insurance companies ranging from life and P&C to Govt forensic analysis of fraudulent claims. Our product smartC is AI based advanced analytics solution that can quickly validate genuine claims while flagging questionable claims patterns using cognitive behavior analysis and has been saving insurance companies claim costs while improving speed to pay genuine claims. We were the pioneers of fast tracking claims using AI patent pending inbuilt algorithms that can match questionable patterns to common insurance fraud schemes. We also read data from forms and use with our analysis. We have been in the market a little longer than some of the companies above. We focus on our customers and our product development is done by industry practitioners and thought leaders making us very unique. We would like to be included in your research going forward

Thank you for the comment Sri! We appreciate you bringing your firm to our attention.

In this article we tried to get a flavor of what’s out there and what we found are TONS of startups attacking the insurance industry. We’ve noted your firm. Would you mind dropping us an email which lets us know about who is backing you? Thank you!

Hi, I am an business developer for Salviol Ltd. (not on the above list), however we have done AI based underwriting for large french based insurer and we have also processed over €4B claims for various insurers. We see that supervised AI has much better results as unsupervised. Clients usually give us policies and claims for several years – we build a model based on that. Then client gives us only policies and no claims for last year and we have to show which policies will turn to fraud. We usually catch around 50 % of policies with fraud elements. Client can easily check our precision and recall rate by checking real claims.

We have tried unsupervised AI but the results were poor.

Hi Matt,

Thank you very much for the comment. This is really interesting.

So how can you tell looking at a policy that it will have more fraud than other policies? You refer to these as “fraud elements”. This concept is fascinating but a cursory look at your website didn’t show any specific examples of how this works. The Tech Crunch article wasn’t overly edifying either. If you have a case study or you can spare any technical details then we’d love to possibly cover this in a future article once we understand how it works. Thank you for taking the time to comment!