What’s a Fair Valuation for Snowflake Stock?

Table of contents

Warren Buffet once said, “it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” This suggests that quality companies don’t often trade at a discount. Mr. Buffet also said that technology stocks aren’t on his radar because he only invests in what he understands, so his investment in big data company Snowflake raised some eyebrows. It implied that Mr. Buffet not only understands Snowflake, but he believes it’s a good company being offered at a fair price.

The billionaire investor’s company shelled out $250 million for about 2.1 million shares in a private placement immediately after Snowflake’s IPO. It spent another $485 million to buy 4 million shares at the IPO price of $120 from former Snowflake CEO Robert Muglia in a secondary transaction.

Credit: Markets Insider

Sure enough, the latest quarterly report from Berkshire shows 6,125,376 of Snowflake still being held by Mr. Buffet. According to the above paragraph taken from Insider, his cost basis would be around $120 a share or roughly what Snowflake’s initial public offering (IPO) was priced at. When the stock opened for trading on the NYSE at $245 in Sept 2020, it was the largest software IPO in history. Shares of Snowflake went on to trade over $400 a share until settling back down and hitting an all-time low of $110 a share several weeks ago. Is now the time to buy a wonderful company at a fair price?

About Snowflake Stock

For information on what Snowflake does, look no further than our piece on Why Warren Buffett is Buying Snowflake Stock which we published in anticipation of the IPO. At that time, and for many months that followed, Snowflake remained overpriced according to our simple valuation ratio. Today, it’s still overpriced relative to its peers, but under our cutoff of 40 with a simple valuation ratio of 28. Here’s how Snowflake stacks up to a handful of names from our tech stock catalog:

| Asset Name | Market Cap (millions) | Last Quarter | Last Quarter Revenue (millions) | Nanalyze Valuation Ratio |

| Snowflake Inc | 46,975 | Q2-2022 | 422 | 28 |

| CrowdStrike | 42,205 | Q2-2022 | 488 | 22 |

| NVIDIA | 426,150 | Q2-2022 | 8,290 | 13 |

| Fortinet | 46,934 | Q1-2022 | 955 | 12 |

| UiPath | 11,646 | Q2-2022 | 245 | 12 |

| Palantir | 20,077 | Q1-2022 | 446 | 11 |

| Unity Software | 12,847 | Q1-2022 | 320 | 10 |

| Okta | 15,608 | Q2-2022 | 415 | 9 |

| Palo Alto Networks | 49,715 | Q2-2022 | 1,390 | 9 |

| Illumina | 30,535 | Q2-2022 | 1,220 | 6 |

| Splunk | 15,485 | Q2-2022 | 674 | 6 |

| DocuSign | 12,921 | Q2-2022 | 589 | 5 |

| Pure Storage | 7,862 | Q2-2022 | 620 | 3 |

Snowflake’s master plan is to achieve $10 billion in revenues by 2029, a compound annual growth rate (CAGR) of about 30%. If the firm magically achieved those $10 billion in revenues today, they’d have a simple valuation ratio of 4.7, and be in the company of names like Illumina, Splunk, and DocuSign. But today, Snowflake’s annualized revenues come in at $1.69 billion, which gives them a valuation ratio of around 28. That’s under our cutoff of 40, but seems too rich given we’re in a bear market. How can investors justify paying such a lofty valuation for Snowflake shares? As usual, it comes down to growth prospects.

Product revenue is a key metric for us because we recognize revenue based on platform consumption, which is inherently variable at our customers’ discretion, and not based on the amount and duration of contract terms.

Credit: Snowflake S-1

Snowflake’s Net Retention Rate

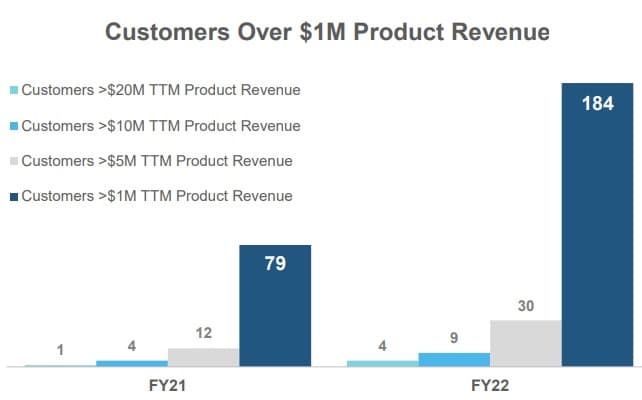

The above paragraph helps explain why Snowflake was able to achieve a net retention rate (NRR) of 174% last quarter, a best-in-class number that’s been consistently increasing over time. It has to do with how Snowflake prices their product – by usage. So, customers start using Snowflake’s platform based on an initial usage contract (averaging 2.4 years in Fiscal 2022), and it takes an average of 210 days before they’ve exceeded the initially agreed-upon usage numbers. After that, any additional spend is reflected in the NRR number. That’s just one of many interesting metrics Snowflake provides their investors including the below chart which shows how spend for their biggest customers is increasing over time.

Credit: Snowflake

Large customers present a greater opportunity for Snowflake because they have larger budgets, a wider range of potential use cases, and greater potential for migrating new workloads to the platform. By 2029, Snowflake expects 77% of their revenues to come from 1,400 customers who pay an average of $5.5 million a year. Presumably, these are customers they’ve already landed. So, here’s a head scratcher for you. If Snowflake drove 93% of Fiscal 2022 revenues from existing customers, why did they need to spend $744 million in sales and marketing during the same year?

Snowflake’s Opportunity

Just over 80% of Snowflake’s revenues are from the United States, something that represents geographical revenue concentration risk. Fortunately, they’re moving to address that by increasing sales and marketing spend in Europe Middle East and Africa (EMEA) and Asia-Pacific and Japan (APJ) by 83% and 275% respectively.

What’s puzzling is why they’re expending so much effort on landing small customers – what they define as “corporate” – when their 2029 target revolves largely around harvesting larger customers. Speaking of which, no single customer accounts for more than 10% of total revenues and Snowflake has around 6,000 customers as they work towards capturing a piece of the total addressable market (TAM) opportunity which is estimated to be around $248 billion.

Credit: Snowflake

That’s not all blue ocean TAM, which means Snowflake still needs to continue displacing industry dinosaurs like IBM and Oracle while concurrently competing with hyperscale cloud computing providers like Microsoft, Google, and Amazon.

The Snowflake Premium

There are several things that make Snowflake stand out, the first being durability. When corporations adopt a data warehousing tool and use it far more than they expected, that shows the product works better than advertised. It also hints at durability, meaning it’s highly unlikely that a customer will decide to switch back to some legacy vendor. When times get tough and budgets are being cut, having a data warehouse with a lower total cost of ownership is appealing to new customers. It’s unlikely existing customers will curtail their usage of credits for computing and storage resources, though they may certainly try to maintain their spend at a particular level.

The other big story from Snowflake is the network effect they’re realizing from their “Data Cloud” product. In our recent piece on datacenter REITs, we talked about a business model called “interconnection” where companies shared corporate data amongst each other. Snowflake’s Data Cloud offering envisions a future where companies might seamlessly share data amongst each other, even offering it for sale at fixed prices or subscriptions. The more companies that join the cloud, the more compelling it becomes for those who haven’t yet joined (this is often referred to as “the network effect”).

Companies are now able to carve out their data and make it available on the marketplace as sources of revenue, or even build apps on top of data that lives in Snowflake’s cloud. This aspect of the platform extends beyond the traditional data warehouse into an entirely new ecosystem.

Finally, it’s important to look at survivability in today’s bear market where raising capital at favorable terms is becoming increasingly difficult. Fortunately, Snowflake made hay while the sun shined. Around $4.8 billion of cash, cash equivalents, and investments sit on their books, all of which can be used to fuel growth in the coming years. In Fiscal 2022, Snowflake saw losses of nearly $680 million, so at that pace, they’d have about seven years runway. More importantly, gross margins are expanding as time goes on which means they should be in decent shape once all that marketing spend is curtailed.

Credit: Snowflake

By 2029, Snowflake expects gross margins to reach 78%.

Buying Snowflake Stock

We’re looking for more exposure to the growth of big data and Snowflake largely fits the bill. We can look past the lack of geographical diversification and assume that will eventually happen. After all, the data cloud will eventually demand international participation in this global world we live in. We can also look past the TAM being occupied by legacy tech firms because Snowflake has proven they’re able to displace the best names in the business. But what we can’t overlook is the excessive valuation.

Considering the lofty expectations Snowflake is subjected to right now, what might happen were some bad news to come out? All it takes is one bad quarter for Snowflake’s shares to fall from grace and trade meaningfully below their IPO price, a target that’s already been breached. Or shares might keep trading lower because we’re in a bear market. Should that happen, we can try to set a simple valuation ratio target that we’d consider buying shares at.

We certainly don’t consider Snowflake’s growth prospects to be average, so we need to pay some premium. Just a few weeks ago, shares dipped to nearly $110 which represented a simple valuation ratio of just over 20. So that’s our line in the sand. If Snowflake shares trade at a simple valuation ratio of 20 or less, we’ll consider that a reasonable valuation and possibly go long the stock as a play on big data. That’s provided we have an open slot in our portfolio, our thesis hasn’t changed, and we haven’t found something more interesting – like that Databricks IPO that’s rumored to be happening this year.

Conclusion

We’d like more exposure to the big data theme, but it’s hard to justify Snowflake’s excessive valuation, even at recent lows. In today’s bear market, a black swan event could bring about some serious fear and volatility. It’s at times like these when wonderful companies can be bought at fair prices. We’ve decided on a simple valuation ratio of 20 or less for Snowflake, but the number doesn’t matter. What’s important is to have a rule in place which helps you identify bargains when the time comes. If the time never comes around, then that’s okay too.

Share

Q3 revenue: $557M, market cap: $50.8B. P/S = 22.8.

Looking ahead to the next quarter, Snowflake said it expects product revenue to be between $535M and $540M, a growth rate of 49% to 50% year-over-year, or well below the 67% the company saw in the third quarter.

Full-year revenue is forecast to be between $1.919B and $1.924B.

Would like to see that simple valuation ratio dip below 20 and we may add some shares.