The Big Solar Debate: SolarEdge Stock Vs Enphase Stock

Table of contents

A surprisingly large number of retail investors ask Google which stock is the best to own. The response is about as predictable as asking the barber if you need a haircut. Any number of pundits out there will tell you which stocks they think you ought to buy. What most lack is a methodology to find which stocks are the most desirable to hold for any given investment thesis. Using solar as an example, here’s how we set about finding the best solar stocks to own from the perspective of a risk-averse investor.

- Find a subject matter expert who ranks investable solar stocks by revenue exposure

- Remove any stocks that present too much risk (a large exposure to California solar legislation, a variable interest entity structure, a David vs. Goliath business, etc.)

- Take the remaining names and try to find out which is the most compelling

We’ve already accomplished the first two bullet points in our piece on The 10 Biggest Solar Stocks in the World which looked at how solar presents a very compelling renewable energy thesis, even more so than wind. The only solar ETF out there – the Invesco Solar ETF (TAN) – tracks a “global passive solar energy index of qualified solar stocks.” The word “passive” is important to note because that means the index isn’t trying to select which solar stocks will outperform, it simply selects companies with the most exposure to solar revenues. Then you have “active” investment products like those from ARK Invest that try to outperform through stock selection and market timing.

After vetting the list of solar stocks from the world’s biggest solar ETF, we were left with the two biggest companies on the list – Enphase (ENPH) and SolarEdge (SEDG). As we always want to invest in market leaders, it’s fitting that we’re left with two solar companies that also make the top-five clean energy companies according to the iShares Global Clean Energy ETF (ICLN).

Both Enphase and SolarEdge have built their businesses around a simple piece of hardware – the solar inverter.

What are Solar Inverters?

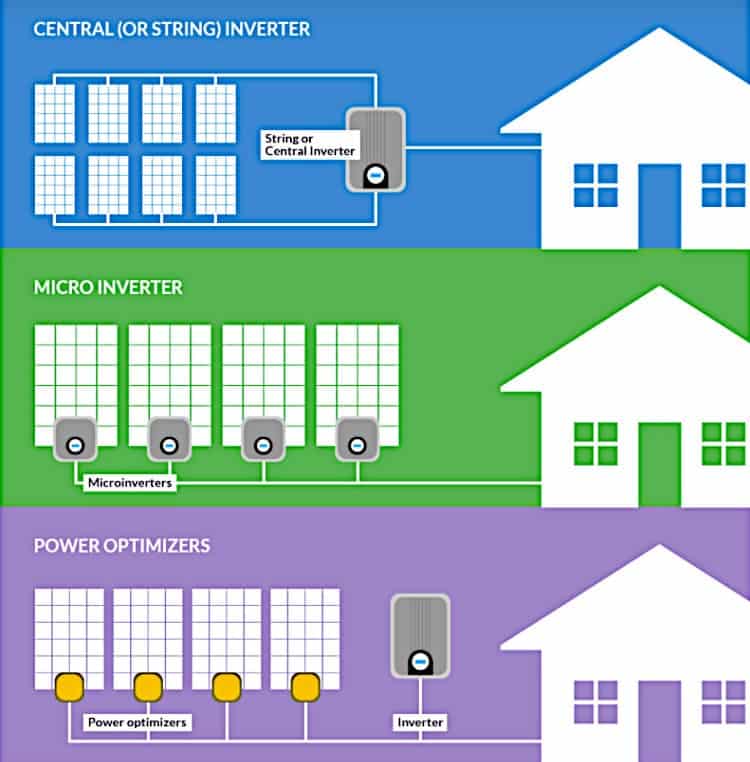

It’s worth taking a hot second to understand solar inverters from the 30,000-foot view. Simply put, inverters convert direct current (DC) into alternating current (AC). Otherwise, a solar system simply won’t function. Historically, inverter technology used central inverters in which the solar PV modules are connected in series strings. Apparently, there are a bunch of limitations to the technology. For example, because the modules are stringed together like Christmas lights, the entire output is limited by the lowest-performing module, and any module represents a single point of failure. In fact, a central inverter is the most likely component to fail in a solar system.

Meanwhile, SolarEdge (SEDG) and Enphase (ENPH) offer the latest and greatest solar inverter design technology.

- SolarEdge – Employs a combination of power optimizers with a central inverter. The power optimizers are installed on each PV module, turning them into smart modules to increase the energy output using algorithms.

- Enphase – Uses a semiconductor-based microinverter that converts energy at the individual solar module level.

Both systems are highly efficient at converting light into electricity, with SolarEdge enjoying a slight edge over Enphase – 99% versus 97%. However, based on our research, the comparison is not completely straightforward because the systems are based on different technologies. For example, microinverters are better at complicated rooftop layouts but notorious for overheating.

Now let’s briefly dive into each company before doing a head-to-head analysis.

About SolarEdge Stock

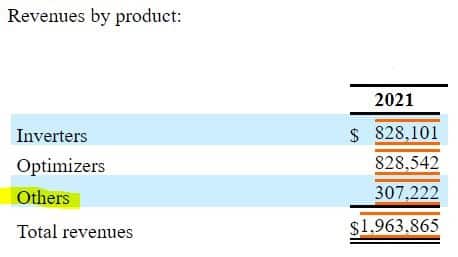

Founded in 2006, SolarEdge is an Israeli company that raised more than $117 million in funding from the likes of GE and Lightspeed Venture Partners before going public in 2015 at a valuation of less than $800 million. Revenues reached $1.96 billion last year, a jump of $500 million or 34.6%, from $1.46 billion in 2020. As you would expect, most of the revenues come from sales of its solar inverter systems – $1.79 billion to be exact. And 84.4% of that money is attributed to sales of optimizers and inverters, which are tracked separately. Other solar-related products include an electric vehicle (EV) charging inverter and residential battery storage, along with various software solutions for energy monitoring and management. SolarEdge is also developing products around decentralized grid services such as virtual power plants that cobble together everything from solar systems to EV chargers. None appear to be significant sources of revenue yet.

Since 2018, the company has ventured outside of solar into other ventures, mainly through acquisitions. A division now called SolarEdge Automation Machines, for example, manufactures automated machinery for industrial applications and SolarEdge e-Mobility develops, manufactures, and sells products for electric and hybrid motorcycles and light commercial vehicles. Powertrains kits supplied by SolarEdge e-Mobility added $55.5 million in revenue last year and were credited with helping boost the bottom line in 2021.

About Enphase Stock

Also founded in 2006, San Francisco-based Enphase raised about $106 million in private money before going public in 2012, with venture capital firm Kleiner Perkins the most notable name on the list of investors. The company IPO’d with a valuation of $235 million. Today, it has a market cap of more than $28 billion on 2021 revenue of $1.38 billion – almost doubling revenue of $774 million in 2020. One of the big drivers of growth is said to be the company’s battery storage system, which it introduced back in 2020. It also started production of its latest-generation microinverter, the IQ8, in 2021. The IQ8 solar microinverters can form a microgrid during a power outage using only sunlight, providing backup power even without a battery.

Enphase itself made a few acquisitions last year related to its solar business, particularly on the software side. For example, it acquired 365 Pronto during Q4-2021 to gain access to a predictive platform dedicated to “simplifying maintenance by matching cleantech asset owners to a local and on-demand workforce of service providers.” Another Q4-2021 acquisition, ClipperCreek, adds an EV charging solution to the company’s portfolio. Expect that the integration will involve leveraging the EV battery as a storage solution to both residential and commercial solar systems in the future. The acquisition is obviously an attempt by Enphase to match SolarEdge as both companies edge toward offering complete energy management and storage systems.

SolarEdge Stock Versus Enphase Stock

Now it’s time for the ultimate cage match between these two solar inverter titans. OK. You’re probably still not too excited by solar inverters, so let’s talk about the growth stories. In less than a decade, these two companies have come to dominate the U.S. residential inverter market with both companies commanding a nearly 90% market share of the U.S. inverter market (Enphase 48%, SolarEdge 40%). And that’s a good segue into why Enphase wouldn’t be a stock we would consider investing in.

Enphase U.S. Exposure

While the percentage is slowly decreasing over time, 80% of Enphase revenues are generated from the U.S. market. The strong growth we’ve been seeing can be partially attributed to tax benefits from the Renewable Energy and Job Creation Act of 2008 which provides tax credits as follows:

- 26% for any solar energy system that began construction during 2020 through December 31, 2022, and 22% thereafter to December 31, 2023, before being reduced to 10% for commercial installations and 0% for residential installations beginning on January 1, 2024.

These benefits could be renewed, or changed, or any other number of regulatory benefits or risks could affect most of Enphase’s revenues. Contrast this to SolarEdge which has just 40% of their total revenues coming from the United States.

Analyzing Customer Concentration Risk

We also see some significant customer concentration risk with Enphase which isn’t improving over time:

- 2021 – one customer 34% of total net revenues

- 2020 – one customer 29% of total net revenues.

- 2019 – two customers 21% and 12% of total net revenues.

The firm doesn’t say who their biggest customer is, but it matters. At least they should disclose the type of customer. Having revenue concentration risk with a distributor is less concerning because they’re typically “distributing” products to multiple customers who help drive demand. Contrast this to a single end customer who consumes the product. For this reason, we see customer concentration risk with distributors to be less concerning than customer concentration risk with end customers.

That being said, SolarEdge says 30.9% of 2021 revenues come from two distributors – Consolidated Electrical Distributors (CED) and Sunrun (RUN). The former is one of the largest privately owned electrical distributors in the United States with 700 locations, while the latter is “an American provider of residential solar panels and home batteries” and the largest residential solar installer in the United States since their acquisition of Vivint. From our perspective, CED would be considered a distributor, while Sunrun wouldn’t.

Recurring Revenue Visibility

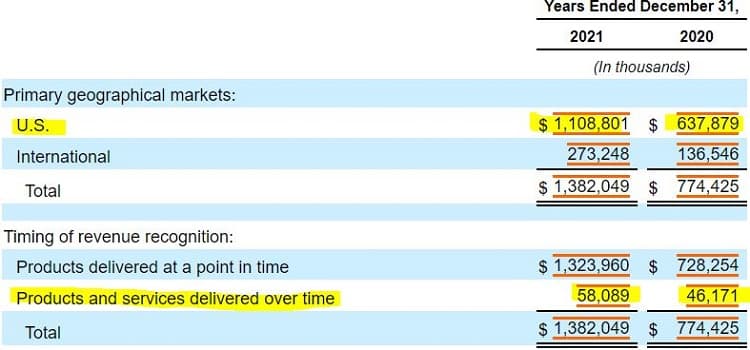

Another criticism we have surrounds any company that sells hardware products without having established recurring revenue streams to go along with them. In the below table we can see how – in addition to their U.S. concentration – Enphase also records 96% of their total revenues as “delivered at a point in time.”

While they talk about cloud-based management solutions, the above table gives us no assurance that they’ve developed a meaningful recurring revenue stream that accompanies the sale of hardware products. In looking at SolarEdge, we see a product breakdown that hints at hardware being separated out, but we can’t be sure.

We also noted that neither company provides any color on their exposure to utility solar vs. residential solar. According to a piece by Morningstar, SolarEdge is said to be evenly split between residential and commercial

Simple Valuation Ratio

Based on the analysis presented today, SolarEdge appears to be a more favorable investment choice than Enphase. While valuations can change quickly over time, it’s also worth noting the difference in simple valuation ratio (market capitalization / annualized revenues) between these two firms:

- SolarEdge

18,046 / 2,208 = 8 - Enphase

28,362 / 1,652 = 17

At least for right now, Enphase appears more richly priced than SolarEdge.

Chasing Performance

Many investors make the mistake of looking at past performance as some indicator of future performance. Enphase and SolarEdge have both crushed it against both TAN and the Nasdaq over the last five years. The former has returned more than +11,000% (not a typo), while the latter has increased more than +2,000% over the same time period. Compare that to about +275% for the one and only solar ETF and “just” +135% for the Nasdaq. That’s even better than Tesla (TSLA), which is up about +1,600% (peaking at about +2,250%) over the same timeframe. Incidentally, Tesla’s solar business, which accounts for only a small percentage of revenues, remains a money-losing one. Incidentally part deux: Before introducing its own inverter technology last year, Tesla had been a SolarEdge customer, so SolarEdge appears to have weathered the loss of a key customer in 2021 quite well.

Frankly, we were surprised to find these two high-growth solar stocks hiding in plain sight at the top of the Invesco Solar ETF portfolio. If these two firms have performed so well over the years, then why haven’t those returns translated into better performance for the ETF we’ve been holding? That’s a complicated question to answer which would require significant back-testing, and akin to mulling over sunk costs. Past performance is no guarantee of future performance, and investors who try to chase performance usually end up getting burned.

Conclusion

While researching this piece we came across lots of analysts comparing these two stocks based on the merits of their technology, or which company has a commanding market share in the United States (currently Enphase). Our focus is on risk, and we see Enphase being too dependent on a single country and a single customer. From this analysis, we can conclude that SolarEdge is a less risky investment than Enphase, but that doesn’t mean we find SolarEdge to be a compelling investment choice. We’ll need at least one more article to figure that out.

Share

Enphase stock showed resilience during the current market crash. Its share price is a bit higher than 1 year ago.

We could say the same about SolarEdge.

So if we take into account 2 factors: huge share price gains in the last couple of years and resilience during market crash – that makes these 2 stocks one of the best stocks one could have in the portfolio till now.

Solar revolution will continue and will accelerate, especially as we now have gas and oil energy crisis due to political situation.

Two of the best solar stocks, perhaps. Solar revolution continuing and accelerating is always subject to the whims of whatever alternative energy source is cheaper by country, or whatever regulation is stimulating or depressing demand in whatever country. Like any theme, there’s the risk alongside the reward.

“Enphase Energy shines after posting big Q2 beat, upside Q3 guidance”.

Q2 Non-GAAP EPS of $1.07 beats by $0.22.

Revenue of $530.2M (+67.8% Y/Y) beats by $24.8M.

GAAP gross margin of 41.3%; non-GAAP gross margin of 42.2%.

+12.8% today.

Cheers for that Stan. Looks like that had a trickledown effect on all green energy stocks.

MF, Sep 11, 2022:

“The past few weeks have been great ones for solar stocks, for a couple of reasons. One of them is June’s executive order from President Joe Biden, which facilitates an expansion of the United States’ solar panel manufacturing industry. And August’s passage of the Inflation Reduction Act provides tax credits to homeowners who install new solar power systems at their homes; the credit is even greater for those homeowners who purchase American-made solar panels and related equipment. Manufacturers, however, will also receive tax credits of their own simply for continuing to make what they’re already making.”

Enphase: “Analysts are calling for top-line growth of 62% this year, to be followed by 34% sales growth next year. The stage is set for even better earnings growth — from last year’s $2.41 per share, to $4.09 this year, to $4.98 per share in 2023.”

The impact that regulation has on this industry is concerning. Solar is able to compete on its own and that’s what government should let it do. The alternative creates volatility and artificial demand.

Enphase proved again it is one of the best stocks you could have in your portfolio. Q3 2022 results:

Enphase said quarterly revenues hit a company record of $634.7M, up 20% Q/Q and 80% Y/Y, and Q3 GAAP gross margin rose to 42.2% from 41.3% in Q1 and 39.9% in the year-ago quarter.

The company said Q3 revenues in Europe jumped ~70% Q/Q, as the region accelerates efforts to address rising energy prices and reliance on fossil fuels.

It’s all a tradeoff between risk vs. reward. There is no FOMO.