Investing in The Metaverse with Event Streaming

Table of contents

They say an average human driver needs about half a second to react to an unexpected event while driving. “In athletics, anything under a tenth of a second is considered unhuman and therefore a false start.” That’s according to a study by Sky Sports that measured F1 driver Nico Hulkenberg’s reaction time at less than a tenth of a second when he won the 2017 Austrian Grand Prix.

The ability to analyze data in real-time is critically important in nearly every use case where data is used to produce insights. If the metaverse envisioned by Jensen Huang of NVDA (NVDA) comes to fruition, we’ll have a digital twin of every enterprise that will be monitored in real-time as we moved towards eliminating all possible inefficiencies. Today, we’re going to look at a company that wants to dominate real-time data processing (also known as stream processing or event streaming) and has a plan to do it – Confluent Inc (CFLT).

About Confluent Stock

In our previous piece on Real-Time Data Analytics and The Metaverse we talked about how an opensource software platform called Apache Kafka is being used by 80% of the Fortune 500. The origins of Kafka are found within LinkedIn where it was developed, and where Kafka deployments recently surpassed 7 trillion messages per day. The three engineers who developed Apache Kafka – Neha Narkhede, Jun Rao, and Jay Kreps – left LinkedIn to start Confluent with their employer as one of their investors. With $6.9 million in funding, the trio managed to create a $20 billion company in just seven years.

Referred to as “stream processing,” the pure software-as-a–service (SaaS) platform offered by Confluent is richly priced and selling like hotcakes. For those of us who speak nerd, here it is from the horse’s mouth:

Our idea was that instead of focusing on holding piles of data like our relational databases, key-value stores, search indexes, or caches, we would focus on treating data as a continually evolving and ever growing stream, and build a data system — and indeed a data architecture — oriented around that idea.

Jay Kreps — Confluent Co-Founder

Being able to analyze streaming data on the fly is a $50 billion market according to Confluent. The easiest way to visualize the potential of the Confluent platform is to imagine a lights-out factory that builds cars and has been recreated in the metaverse as a digital twin. You won’t want to hear about a problem a week after the signs started to appear, you need to know in minutes. If you’re using a platform like Augury that listens to the sound of your machines to hear when they need maintenance, or are about to break down, you need that information as quickly as possible to act on it immediately. They don’t call it predictive maintenance for nothing.

There are also implications around data infrastructure costs. Instead of storing all your events in an expensive data management platform like Snowflake, just send all that data exhaust over to Confluent so they can quickly analyze it, take action on it, then iterate. While platforms like Snowflake might have no problem performing the same set of analytics, they won’t be able to do it at the speed Confluent can. So, you’re getting improved latency at a lower cost, something every Chief Technology Officer (CTO) can get behind. These dual-pronged value propositions sell exceptionally well during times of economic turmoil when everyone gets told to “redouble their efforts” and do more with less.

The Competition

Our confidence in the Confluent platform stems from knowledge of how the opensource community operates. Software developers – the type who don’t try to advance their careers by complaining – have a talent for recognizing competency among their ranks. They know it when they see it. A rock star developer may be an arrogant prick, but they’ll usually give respect where it’s due, if not just because of peer pressure. Everyone who uses Apache Kafka – like all the engineers in 80% of the Fortune 500 companies where it’s used – will respect the creators of that program. When it comes time for Confluent to sell their platform to an internal audience of decision makers, that respect may make the difference between whose RFP gets picked. That’s especially true if your competition looks like this.

We couldn’t find a Gartner Magic Quadrant for “stream processing,” but we did find the above chart which is based on a report titled “Gartner, Market Share Analysis: Event Stream Processing Platforms, Worldwide, 2020” which is only available to paying clients. It might be one of the worse charts we’ve seen in a while. It’s a classic Y-axis stretch, and Microsoft’s 11% is suspiciously larger than the other two 11% values, but let’s just roll with the punches here.

The chart appears to be produced by Informatica, a company that’s said to have the second biggest market share in “streaming analytics,” and one that recently had an initial public offering (IPO) which tried to convince the masses they aren’t just a spent software company that’s fallen behind the times. The obvious question is, why doesn’t Confluent appear in the above “chart?”

The answer might lie in the Confluent S-1 document that accompanied their IPO this past June. The company believes their total addressable market (TAM) crosses four core Gartner-defined market segments. Here’s how they see their $50 billion TAM broken out across these four areas:

- $31 billion in Application Infrastructure & Middleware

- $7 billion in Database Management Systems

- $7 billion in Analytics and Business Intelligence

- $4 billion in Data Integration Tools and Data Quality Tools

Furthermore, the above opportunity is expected to reach $91 billion by 2024, a compound annual growth rate (CAGR) of 22%. This breakdown suggests that Confluent might exist in a competitive landscape of its own, one that hasn’t been coined yet by overpaid MBAs.

Let “Stream Processing” = “Event Streaming”;

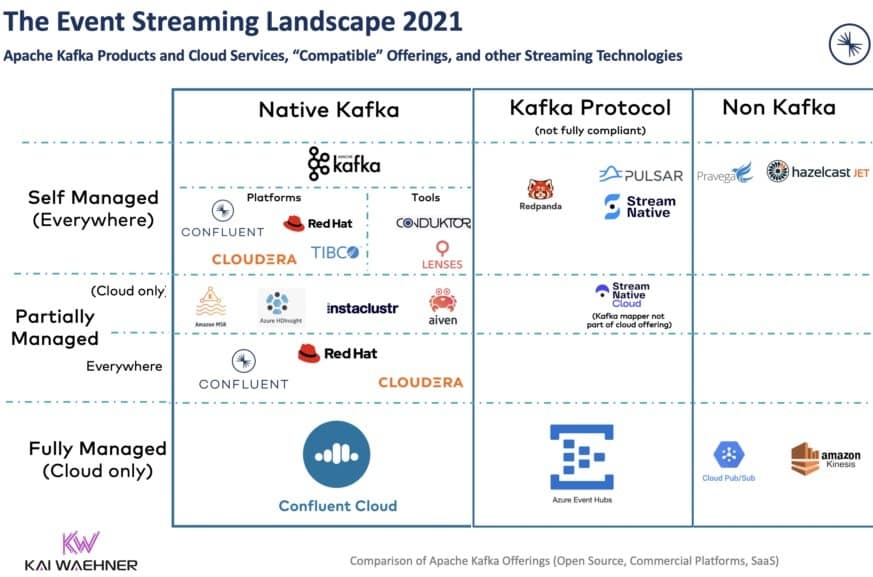

Kai Waehner may refer to himself as a Technology Evangelist but don’t hold that against him. Zee Germans often use titles like this to impress the Americans. Mr. Waehner’s actual title, Field CTO at Confluent, means he spends most his time outside the ivory tower speaking with clients, partners, and potential customers. Just weeks ago, Mr. Waehner penned an excellent piece on this topic which concludes that, “unfortunately, a Gartner Magic Quadrant or Forrester Wave for Event Streaming does NOT exist today.” He then proposed that the competitive landscape ought to look something like this.

According to the above image which we doctored and still isn’t legible, Confluent’s most formidable competitor might be a company we wrote about four years ago in a piece titled Cloudera – What Would You Say, You Do Here? Here’s how we described the firm back then:

So, there is this very popular open source software called Hadoop and people use it for storing and processing big data. A whole bunch of smart software dudes liked Hadoop so they went and started a company called Cloudera and brought with them the dude who actually wrote the Hadoop software back in 2004.

And that’s about as far as we got.

Both these firms have enjoyed success by originating from the opensource community, but we’ll save a proper comparison for another day and get down to brass tacks. Is Confluent stock a good way to invest in picks and shovels for the metaverse?

Investing in The Metaverse With Event Streaming

Props to one of our loyal readers who brought Confluent to our attention, and we’re now kicking ourselves for not sufficiently assessing the Confluent IPO that debuted in June 2021. (We have a process in place to vet all coming IPOs and it clearly needs some tweaking.) When Confluent shares debuted on the public market, they commanded a market cap of $11.4 billion. Here’s how our simple valuation ratio would have looked back then using Q1-2021 revenues of $77 million:

- Market capitalization / annualized revenues

$11,400 / 308 = 37

That’s just barely under our cutoff of 40. (We don’t invest in any company with a simple valuation ratio over 40, no matter how great their story is.) Today, shares are too richly valued based on Q3-2021 revenues of $103 million:

- Market capitalization / annualized revenues

$20,460 / 412 = 50

Several weeks ago, Confluent actually dipped enough such that the ratio would have been below 40. We’re hoping that won’t be the last time the ratio dips like that, and when it does again, we just might go long. If that happens, Nanalyze Premium subscribers will be the first to know. In the meantime, we’ve teed up a piece for our research team which will open Confluent’s kimono and make sure no red flags are lurking under there.

Conclusion

Confluent may represent a solid way to invest in the future metaverse where the world’s enterprises will largely be portrayed by digital twins. Confluent ticks all the boxes for us so far, a pick-and-shovel SaaS pure play that’s right in our size sweet spot with a $20 billion market cap and lots of room for future growth. Like Snowflake, shares are richly priced, but they’re also subject to volatility like any other tech stock. If that valuation drops enough, we just might go long on the exciting future of event streaming.

Share