8 Startups Offering On-Demand Insurance

Table of contents

Our recent article on 10 Artificial Intelligence Startups in Insurance has been receiving all kinds of interest from our readers which shows we’ve touched on a hot topic. In that article, we talked about how auto insurance companies are not operating in a sustainable fashion and the only way we can resolve that is through technology. It’s important to note that since the insurance industry is so far behind the times when it comes to technology, you don’t even need to do anything that advanced to add value. A simple concept like “on-demand insurance” can go a long way to improving things. Nonetheless, this hasn’t stopped a whole bunch of the +2,000 AI startups out there trying to cater to the insurance industry. The below “AI deal tracker” from CB Insights demonstrates this.

![]()

You see that bright red square in the above heatmap? That shows us that “Fintech & Insurance” AI startups received the most funding out of any category seen above (yes, the font sucks, but it takes a 10K a month subscription to fix it). Remember how we talked about following the money? In this case, a great deal of the money is leading to insurance.

According to The Boston Consulting Group, the 3 critical dimensions of customer satisfaction in insurance are transparency, quality, and speed. Customers need to understand where they are in the application or claims process and they want transparency just as much as they do speed and quality. Savvy consumers are no longer satisfied with the error-free processing rates of 70% to 80% which insurers are currently able to deliver. In terms of speed, customers are not yet expecting real-time processing but they do expect turnaround to be at least in hours not days.

Waiting time typically consumes at least 95% of insurance application processes. (“Customer-Centricity in Insurance“. The Boston Consulting Group)

In the below diagram, BCG shows how speed in the insurance application process varies across different types of insurance coverage:

One way to decrease this “waiting time” is through reinventing the entire insurance process like Lemonade has done for home and rental insurance. Another example we gave before was Metromile: Pay As You Go Auto Insurance which can be used to quickly offer insurance coverage for drivers who are not driving frequently. On-demand insurance is an innovation making insurance coverage literally a snap or swipe. Surprisingly, these startups don’t seem to be competing with existing players in the industry. They are either reselling or enabling the value proposition of existing insurers. Here are 8 more examples of “on-demand insurance” offerings.

Trōv, Inc.

Founded in 2012, Danville, California startup Trov Inc. has taken in $87.8 million from 6 rounds of funding to develop on-demand insurance app for valuable possessions like camera equipment for example. The app allows you to turn-on and turn-off insurance coverage of items that truly matter to you through your mobile device with details derived by a simple picture using your smartphone. Some screenshots of the app’s coverage, price quotes, and claims process can be seen below:

Founded in 2012, Danville, California startup Trov Inc. has taken in $87.8 million from 6 rounds of funding to develop on-demand insurance app for valuable possessions like camera equipment for example. The app allows you to turn-on and turn-off insurance coverage of items that truly matter to you through your mobile device with details derived by a simple picture using your smartphone. Some screenshots of the app’s coverage, price quotes, and claims process can be seen below:

Over $10 billion worth of items have been added to the Trov app, items such as televisions, smartphones, sports equipment, and even musical instruments. This on-demand insurance offering is currently available in the United Kingdom and Australia but will be available in the US this year.

Verifly Insurance Services

Founded in 2015, New York startup Verifly Insurance Services has taken in $4.86 million in funding to create an on-demand insurance offering for drone operators. In 2015, 270 thousand drones were being used for recreational reasons with the consumer drone market expected to grow to $4.19 billion by 2024. Verifly provides an insurance product available on-demand for drones weighing 15 lbs or less which protects you against liability arising from accidents while operating your drone, including operational mistakes:

Founded in 2015, New York startup Verifly Insurance Services has taken in $4.86 million in funding to create an on-demand insurance offering for drone operators. In 2015, 270 thousand drones were being used for recreational reasons with the consumer drone market expected to grow to $4.19 billion by 2024. Verifly provides an insurance product available on-demand for drones weighing 15 lbs or less which protects you against liability arising from accidents while operating your drone, including operational mistakes:

We’re not entirely sure what sort of damage you could cause with a drone that would run up to $1 million, but it’s probably only a matter of time before you’re mandated to have liability insurance in order to fly a drone (in much the same way you need liability insurance to drive a car). Verifly doesn’t underwrite the policies themselves, but acts like a matchmaker to provide coverage now available in 49 states (mainly through Global Aerospace Inc.).

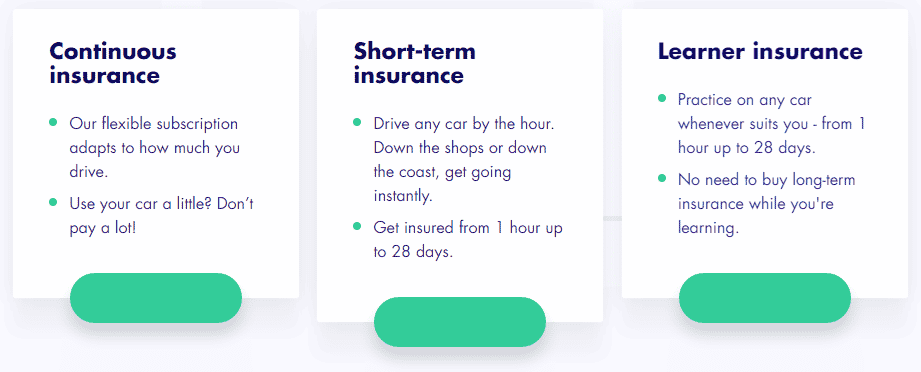

Cuvva

Founded in 2014, London startup Cuvva has taken in $2.63 million from 4 rounds of funding. Cuvva auto insurance allows you to pay for just what you use based on the exact number of hours you’re driving, offering a competing value proposition to Metromile with a slightly different twist. You can insure yourself to drive in any vehicle for durations as little as a single hour:

Founded in 2014, London startup Cuvva has taken in $2.63 million from 4 rounds of funding. Cuvva auto insurance allows you to pay for just what you use based on the exact number of hours you’re driving, offering a competing value proposition to Metromile with a slightly different twist. You can insure yourself to drive in any vehicle for durations as little as a single hour:

You got your friend’s car covered on this one and you can turn-on or turn-off coverage based on how many hours or even days (from 1 to 28) you want to use someone else’s car. Before you Yanks get too excited, it’s only available in the U.K. for now.

Update 12/03/2019: Cuvva has raised $19.6 million in funding to launch a new monthly auto insurance product in early 2020 that it says could cut average annual bills for car owners “significantly.” This brings the company’s total funding to $23.1 million to date.

Slice Labs

Founded in 2015, New York startup Slice Labs has taken in $3.9 million to provide a tailored insurance offering for home-sharing hosts who are at risk of vandalism, theft, excess utility usage, or insect infestations. The hosts pay only for insurance equivalent to the guest’s length of stay and the offering is available as a beta offering in 13 states for AirBnB, VRBO, HomeAway, and FlipKey.

Founded in 2015, New York startup Slice Labs has taken in $3.9 million to provide a tailored insurance offering for home-sharing hosts who are at risk of vandalism, theft, excess utility usage, or insect infestations. The hosts pay only for insurance equivalent to the guest’s length of stay and the offering is available as a beta offering in 13 states for AirBnB, VRBO, HomeAway, and FlipKey.

Slice Labs is also testing an app for an insurance product to protect against liability associated with ridesharing commercial activity such as injury, liability, lost income, at fault, and uninsured drivers. Munich Reinsurance (one of the world’s leading reinsurers) invested in Slice Labs (they also happened to invest in Trōv as well).

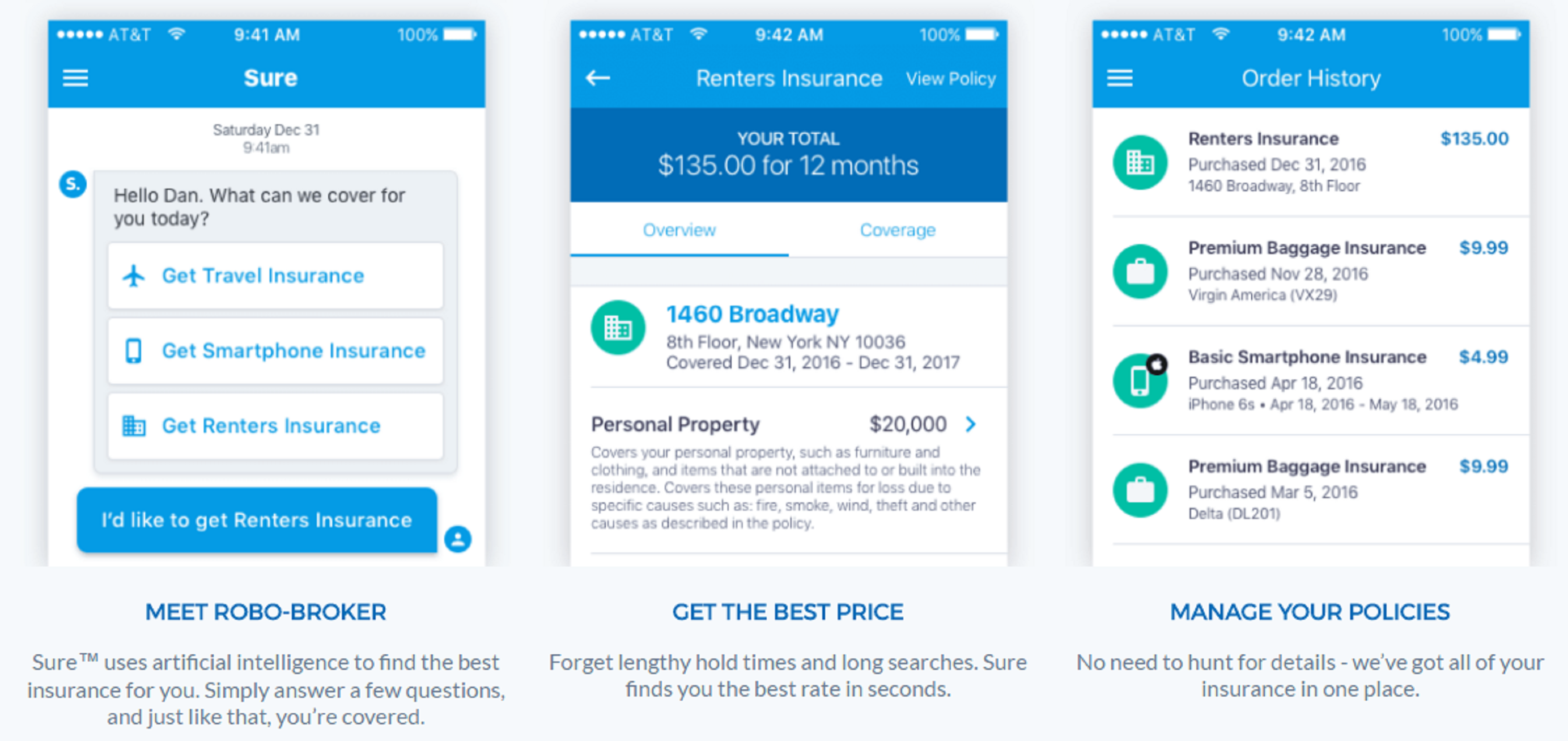

Sure Inc.

![]() Founded in 2014, New York startup Sure Inc. has taken in $2.6 million to introduce their on-demand renter’s insurance, baggage insurance, and they even have your smartphone covered. According to an article by DigitalInsurance, the tech “relies on machine learning for risk analysis to a small degree, but it is its distribution engine that is at the forefront“. That “distribution engine” is in the form of an easy-to-use app which can be seen below:

Founded in 2014, New York startup Sure Inc. has taken in $2.6 million to introduce their on-demand renter’s insurance, baggage insurance, and they even have your smartphone covered. According to an article by DigitalInsurance, the tech “relies on machine learning for risk analysis to a small degree, but it is its distribution engine that is at the forefront“. That “distribution engine” is in the form of an easy-to-use app which can be seen below:

Sure uses geo-location to determine your eligibility for various policies by state and has partnered with 20 insurance providers so far who will underwrite the policies on offer.

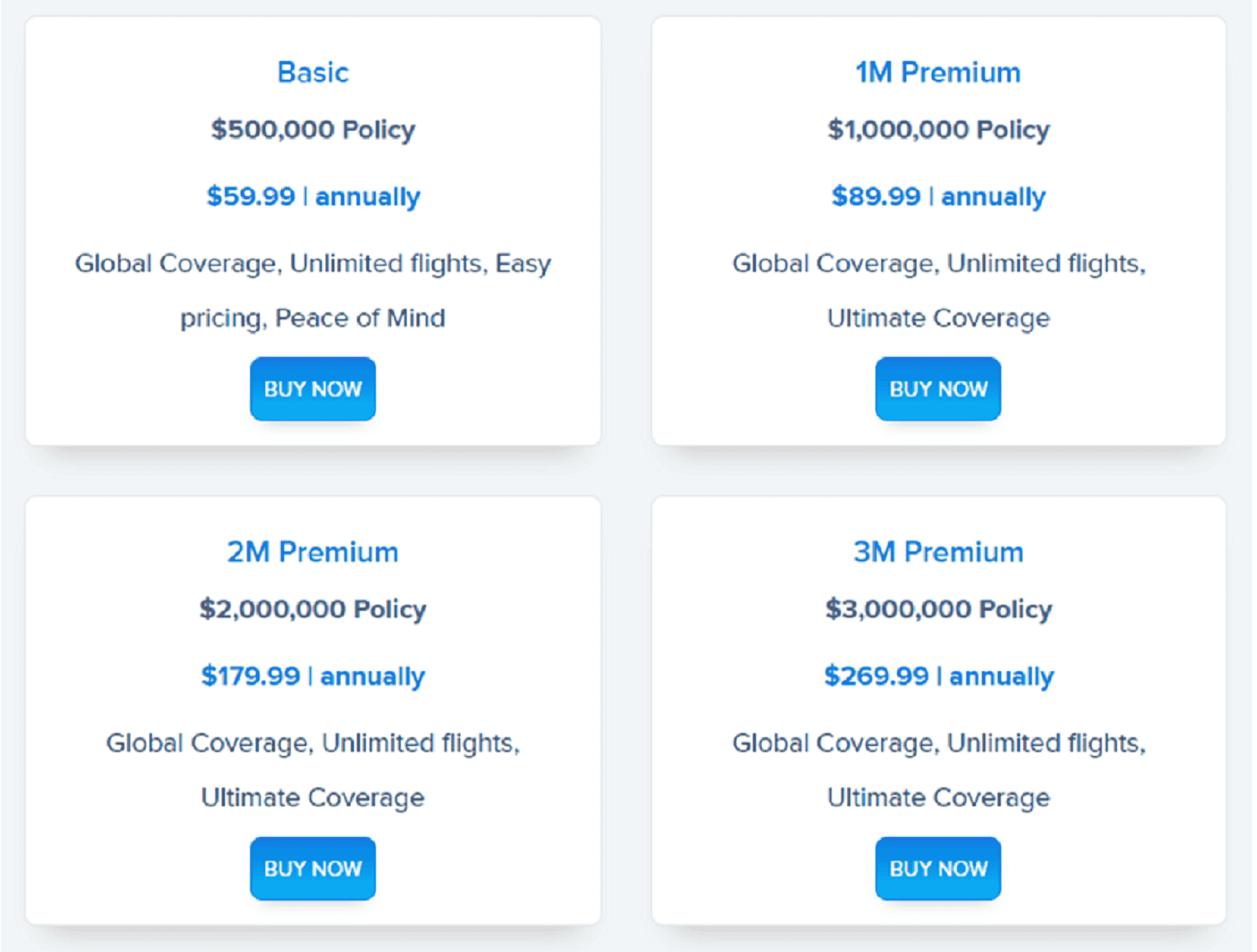

Airsurety, Inc.

![]() Founded in 2015, New York startup Airsurety has taken in an undisclosed amount of funding to focus almost exclusively on accidental deaths that take place during air travel. The odds of dying in a plane crash sit at 1 out of 11 million, compared to 1 in 5,000 odds of dying in a car or traffic accident, so this is clearly a product for

Founded in 2015, New York startup Airsurety has taken in an undisclosed amount of funding to focus almost exclusively on accidental deaths that take place during air travel. The odds of dying in a plane crash sit at 1 out of 11 million, compared to 1 in 5,000 odds of dying in a car or traffic accident, so this is clearly a product for people who worry to much people who want that extra peace of mind. Here are the four policies on offer by Airsurety:

Coverage can be availed of by simply entering your full name, email address, and making a credit card payment. The airline you choose should have a safety rating of 5 or higher to be covered so that pretty much scratches off any domestic airline in Indonesia, Air Koryo, and probably most airlines operating exclusively in Africa.

Digital Risks

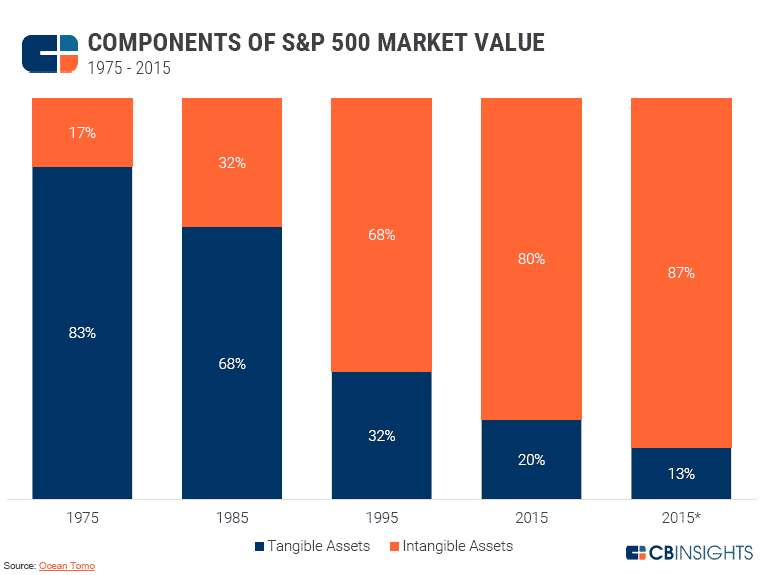

Founded in 2014, yet another UK startup is Digital Risks which has taken in an undisclosed amount of funding to develop an on-demand insurance offering for startups and small businesses with a focus on digital assets. Digital Risks covers digital businesses against loss due to employer’s liability, public liability, professional indemnity, cyber liability, directors & officers’ liability, content & equipment, commercial legal protection, and media liability. According to the great minds at CB Insights, more than 85% of the S&P 500’s current value may be attributed to intangible assets such as intellectual property, brands, data, etc. as seen below:

Founded in 2014, yet another UK startup is Digital Risks which has taken in an undisclosed amount of funding to develop an on-demand insurance offering for startups and small businesses with a focus on digital assets. Digital Risks covers digital businesses against loss due to employer’s liability, public liability, professional indemnity, cyber liability, directors & officers’ liability, content & equipment, commercial legal protection, and media liability. According to the great minds at CB Insights, more than 85% of the S&P 500’s current value may be attributed to intangible assets such as intellectual property, brands, data, etc. as seen below:

These insurance products can be managed online, you can get a quote in minutes, and pay on a month-to-month basis with no commitments.

Neosurance Srl

![]() Founded in 2016, Italian startup Neosurance has taken in just $230,000 to develop a “virtual insurance agent as-a-service” to insurers which is available via a cloud offering called Neosurance. The platform offers “contextual insurance coverage” to customers via hyper-targeted policies based on their profile, behavior, location, and the context under which they are requesting insurance. The idea is to make purchasing insurance a quick and painless experience that takes place on your smartphone with no paperwork and zero hassle. The Neosurance business model is to sell this accessible and convenient platform as a service to all insurance companies.

Founded in 2016, Italian startup Neosurance has taken in just $230,000 to develop a “virtual insurance agent as-a-service” to insurers which is available via a cloud offering called Neosurance. The platform offers “contextual insurance coverage” to customers via hyper-targeted policies based on their profile, behavior, location, and the context under which they are requesting insurance. The idea is to make purchasing insurance a quick and painless experience that takes place on your smartphone with no paperwork and zero hassle. The Neosurance business model is to sell this accessible and convenient platform as a service to all insurance companies.

Back Me Up

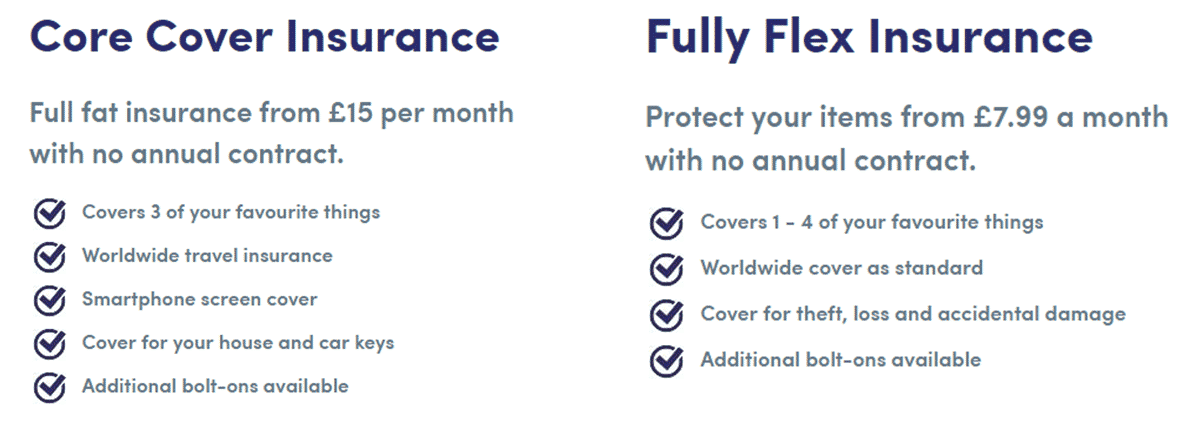

While this one isn’t a startup, we included it anyway as a freebie. Founded in 2016, Back Me Up is actually a subsidiary of Ageas Insurance, one of the largest insurance companies in the United Kingdom. The on-demand insurance offering provides coverage at two levels: Core Cover Insurance and Fully Flex Insurance. You can activate additional coverage “Bolt-Ons” to cover for an additional item, breakdown of your vehicles, adventure activities, and even landlord disputes.

While this one isn’t a startup, we included it anyway as a freebie. Founded in 2016, Back Me Up is actually a subsidiary of Ageas Insurance, one of the largest insurance companies in the United Kingdom. The on-demand insurance offering provides coverage at two levels: Core Cover Insurance and Fully Flex Insurance. You can activate additional coverage “Bolt-Ons” to cover for an additional item, breakdown of your vehicles, adventure activities, and even landlord disputes.

Back Me Up has a community of customers you can ask about Back Me Up services or insurance claims issues. The Company uses an AI solution for its claims management from Tractable, a startup we mentioned in 10 Artificial Intelligence Startups in Insurance, that can provide cost estimates for auto insurance claims using deep learning algorithms.

Conclusion

While these apps offer transparency, convenience, and generally less time spent waiting, there is one additional benefit. Insurance products are not only expensive and inflexible, but then you usually need to deal with some “agent” whose sole purpose in life is to jack you for as many dollars as humanly possible while he tries to act like he’s helping you. Ok, that might be a bit cynical, but plenty of insurance agents have their compensation tied to commission which directly correlates to how much money you spend. These apps stand to displace insurance agents and that may be just-in-time considering that insurance agents are apparently retiring left and right with nobody to replace them. Fortunately for everyone involved, it doesn’t look like they’ll need to be replaced.

Share

You forgot Insurescan, they allow a quick scan of driver license barcode, and a fast VIN scan, and poof… quotes. Typing increases time, and error rates are sky high, but not with them.

Hi Jason,

Thank you for pointing out Insurescan. We didn’t include all companies out there because that’s hardly possible.

We like the look of the app which is in beta and can be seen below:

http://insurescan.net/

Aegeas is one of the largest insurers in the UK so if Back Me Up is a trading name of theirs, this is not a start-up.

Thank you for pointing that out Paul. It looks like our writer exhibited some ethnocentric bias (as we Yanks are well known for) and failed to recognize the parent company. We’re going to add another startup and then also include “Back Me Up” so everyone wins.

Thank you for taking the time to point that out.

Insurance is NOT a Commodity! Of all the things said in the InsurTech vortex, the biggest misconception/lie is that all insurance policies are the same, that there is no real difference between policies issued from different companies. Yes, you can go to a website/mobile app, fill in a handful of fields, get a quote and coverage. But are the policies actually the same? Will you receive the coverage you need? Link to this article for more info;

https://goo.gl/Ud4ZCp

Hi Chet,

That’s a really good article you wrote. Thank you for posting that. We were blown away to read that there are +800 InsurTech startups. We’ve barely scratched the surface so far!

It’s quite surprising how complex the insurance industry is. As you are implying, just because on-demand insurance looks to be much simpler because it’s in a pretty app, it doesn’t mean that the underlying policies are not complex and wildly different between providers.

It looks like your firm is trying to digitize some of that complexity so well done there!