SomaLogic Stock: A Significant First-Mover Advantage?

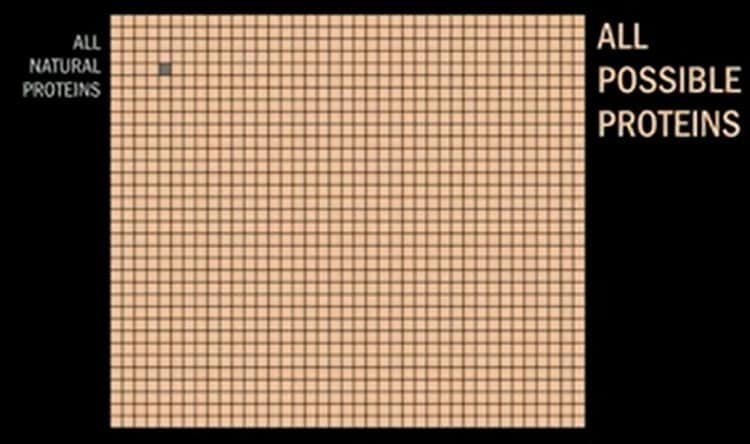

Proteomics – the study of proteins – is incredibly complex stuff. That’s why fund managers often hire subject matter experts to navigate such topics. We disagree with this approach. You cannot invest in what you know if you need an interpreter to do so. A simple understanding of the opportunity can suffice in most cases. For example, this basic chart sums up the proteomics thesis quite well.

Think about all the things we can accomplish by harnessing the power of nature through engineering proteins that don’t exist in nature yet, something that falls squarely under the umbrella of synthetic biology. That’s why we published our piece on A List of 7 Proteomics Stocks For Investing in Proteins and invested in just one of those companies – Quanterix (QTRX). Today, we want to check in with a proteomics company that claims to have the leading proteomics platform on the market with “a significant first mover advantage.”