What’s the Best Robot Stock to Invest In?

Those with very little capital to invest often look for ways to increase it exponentially while taking on loads of risk in the process. We call this “finding the next Tesla.” Usually, this starts with a theme that’s easy to understand and compelling. Robots are a great example. Then it’s off to ask the Ministry of Truth which robot stock is the “best” to invest in. Let’s go ahead and do that.

The first result is an ad – some crowdfunded pizza robot that you shouldn’t touch with a ten-foot pole. Never invest in any crowdfunding ventures because there is no market for your shares and they are worthless until that changes. Next on the list, an ETF from iShares which we covered in our piece on Which Robotics ETF is The Best One to Buy? The third search result is an article on 10 robot stocks from InvestorPlace written by a gentleman who describes this curated list as “our portfolio of robot stocks” but then tells us at the end that he hasn’t invested in any of them. It’s like the wealthy gentleman who drives to the bank in a Bentley taking advice from the fresh MBA graduate who took the train to work.

The title of our article is based on a genuine question we’re asking ourselves right now. What’s the best robot stock to invest in? We previously held shares of the Global X Robotics & Artificial Intelligence ETF (BOTZ) until we decided not to hold ETFs and liquidated our position. That left us with one robot-related stock, Teradyne (TER). So it’s off to consult with the Nanalyze Disruptive Tech Portfolio Report which contains three robotic stocks we like which we’re going to talk about today.

Robot-Enabled Surgeries

Images of robots performing surgeries should be replaced by robotic devices that assist surgeons to perform surgeries. That’s what’s on offer from Intuitive Surgical (ISRG), a company we wrote about earlier this year in a piece titled Intuitive Surgical Stock Leads Robot-Assisted Surgery. With a market cap of around $74 billion, ISRG is trading near 52-week lows with a simple valuation ratio of 12 which means it’s still a bit on the higher side compared to most tech stocks in the single digits. Between 2012 and 2018, use of robotic surgery for all general surgery procedures increased from 1.8% to 15.1% and Intuitive Surgical is considered the market leader with around 80% market share which is a moat we view quite favorably. If you believe robot-enabled surgeries are the way forward, this is the company to invest in.

Intuitive saw $5.7 billion in revenues for 2021 and the total addressable market is expected to reach nearly $10 billion next year which represents compound annual growth of 16% over five years. That’s according to a report by Informa UK which also provided this handy chart (although a bit dated now) showing what other companies are dabbling in this space.

In positions one and three on the above list are Stryker (SYK) and Medtronic (MDT), two companies we’re holding as part of our dividend growth investing strategy along with Johnson & Johnson which saw their robotic surgery platform face delays of several years. Our investments in SYK and MDT mean that about 3.5% of our total assets under management are exposed to medical devices. An investment in ISRG would also increase our tech portfolio exposure to life sciences which already sits at 15%, more than double our target weighting of 8%.

With gross margins of 69% and recurring revenues accounting for 75% of revenues, ISRG starts to look and feel a lot like Illumina (ILMN), another healthcare company we’re holding that’s the third-largest position in our tech stock portfolio. At half the size of ISRG, Illumina has the same gross margins, about the same recurring revenues, and a simple valuation ratio of six.

| Market Cap (billions) | 2021 Gross Margin | 2021 Recurring Revenues | Simple Valuation Ratio | |

| Intuitive Surgical | 74 | 69% | 75% | 12 |

| Illumina | 30 | 70% | 80% | 6 |

Intuitive Surgical may have dropped quite a bit but it’s still looking rich from where we’re sitting.

A Machine Vision Leader

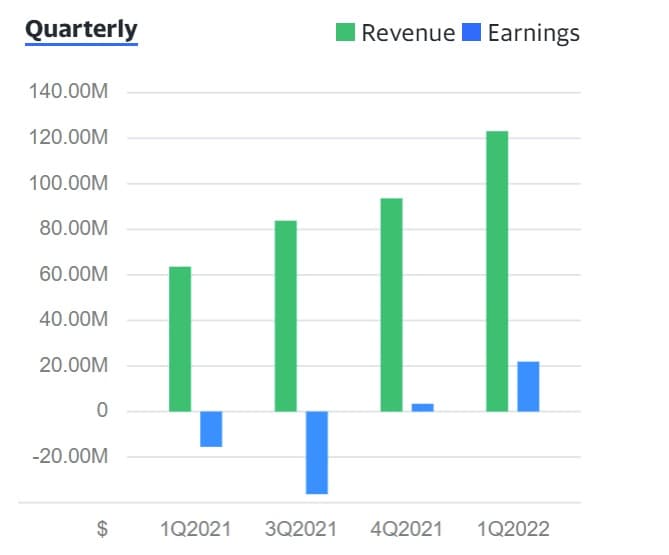

We first wrote about Cognex back in 2016 noting their leadership in computer vision and focus on factory automation which accounted for 82% of their revenues. Since then, the company has more than doubled their market cap – from $3.1 billion market cap to $7.7 billion – and when we last checked in our concern was around their stalling revenue growth. That was rectified in 2021 when the firm saw over $1 billion in revenues while the share price nearly halved in the past rolling year.

With a simple valuation ratio of 8, Cognex doesn’t appear to be overvalued, so we dug into their financials a bit to understand where the growth is coming from. That’s where things became problematic. Cognex doesn’t break down their segments – electronics, automotive, logistics, etc. – into segments so we can see where the growth is coming from or what overall exposure we’re getting. The last earnings call has a gentleman reading from a script and making vague comments about how these various verticals performed with no accompanying deck. Below is the most valuable slide in their generic investor deck which seems to say the total addressable market across all segments is $4.2 billion which is quite small.

While we love their gross margins of over 70% (quite high for a hardware company), we’re not overly stoked they’ve been paying a dividend for 19 years now (increasing for seven). We’d rather that money was spent investing in growing their business, but this should make for a compelling dividend champion in 18 years provided they keep increasing the dividend. The most interesting metric from last year is that logistics grew 65% to become their largest revenue segment at around 30%, so at least they’ve diversified their revenue streams since we last looked. That said, we don’t like investing in companies that provide vague statements about progress instead of hard numbers.

Warehouse Robots

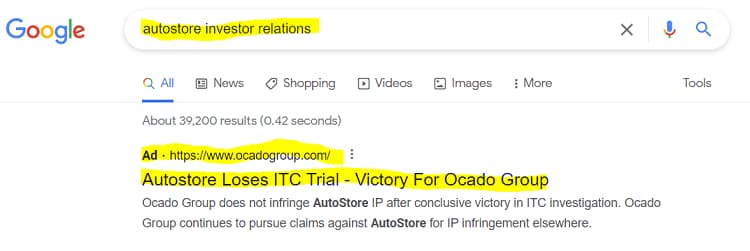

Of these three stocks, we’d probably find AutoStore the most compelling were it not for their pissing contest with Ocado Group. It’s something we last covered in a piece titled A Legal Showdown: AutoStore vs Ocado Group. The hatred must run very deep when you run ads targeted at your competitor’s investors boasting of how you bested them in court.

AutoStore’s Q1-2022 report mentions the name “Ocado” 45 times, so both companies seem obsessed with battling each other for reasons we can’t decipher. In their latest investor deck, AutoStore makes the following statement about potential downside in the Ocado spat.

At the current stage of proceedings, AutoStore has small downside risk from unfavourable decision, including in part by strengthening innovation and patent filing strategies

Credit: AutoStore

Should we trust the company’s assessment of “small downside risk” and invest anyway? Perhaps we can wait for the next milestone, the UK court’s decision expected sometime in Q3-2022. Since AutoStore’s half-year report will be released in the middle of Q3-2022 (about 5 weeks from now), maybe that will be a good time to check back in with the company. With annualized revenues of $492 million and a market cap of $5.3 billion, AutoStore’s simple valuation ratio of 11 is a lot lower than where it was at their IPO (33). Gross margins of 63% mean that AutoStore managed to eke out a small profit this past quarter, even after spending nearly $10 million battling Ocado. With $83 million in cash on hand, they don’t have much dry powder to incur losses, though the trend appears to be going in the right direction.

And on that note, we’ll call it a day. If we do decide to pull the trigger on one of these stocks, Nanalyze Premium annual subscribers will be the first to know via our trading alerts.

Conclusion

The three companies on our shortlist are all compelling ways to play robotics, aside from the reservations we’ve pointed out today. Given the current bear market, we’re planning on putting the 14% cash we have left in our tech portfolio to work, both adding to existing positions and potentially identifying new positions. Robotics is an area we’d like more exposure to, thus the reason for this article. If you have a robotics company you think we ought to consider, please drop it in the comment section below. Nothing under $1 billion market cap, please.