ABB vs FANUC vs Yaskawa – The Winner Is?

Table of contents

The more mature a theme becomes, the more likely it is that one or more leaders will emerge. Our recent article on A List of 14 Promising Robotics Companies uncovered three names – FANUC (6954.T), ABB (ABB), and Yaskawa (6506.T) – that are considered to be the top producers of industrial robotics solutions. Today, we’re going to vet these three firms to see which might find a home in our own tech stock portfolio. Before peeking under the kimono, it’s important to recall why we’re looking to swap out Teradyne (TER). It’s because we’re not getting sufficient pure-play exposure to robotics. Consequently, this article will largely be focused on examining the “purity” of industrial robotics exposure on offer from these three firms. All numbers going forward are in USD unless specified otherwise.

China accounts for more than half of all new robotics installations and we expect the global robotics market to grow from around $80 billion today to $130 billion in 2025.

ABB 2022 Annual Report

The Big Three

Leaders typically emerge as large firms that sell lots of stuff. Below you can see how these three companies stack up by size, revenues, and simple valuation ratio (SVR).

ABB may be the biggest of the lot, but that doesn’t mean they’re the best option. What’s most important is the actual exposure we’re getting to industrial robotics, and how fast that exposure is growing. Let’s start by looking at ABB’s industrial robotics segment.

ABB

Perusing ABB’s latest earnings deck shows a company that’s quite mature and diversified, one that fits the profile of value more than growth. That’s evident in their “above 5%” revenue growth target for 2023 and low SVR number (our catalog average is six). That meshes well with the firm’s annual target of 4-7% revenue growth, a goal that wasn’t met in 2022 with revenue growth of just 2%. While ABB flaunts their “comparable” revenues growth in 2022 of 12% (essentially organic growth), we keep things simple and focus on one number – annual revenues reported to the SEC in the 10-K.

ABB’s revenues can be broken down into four segments with Robotics & Discrete Automation making up just 11% of total revenues in Q4.

| Business Segment | Q3-2022 | % of Total |

| Electrification | 3.66 | 46% |

| Motion | 1.85 | 23% |

| Process Automation | 1.55 | 20% |

| Robotics & Discrete Automation | 0.89 | 11% |

A few reasonable arguments can be made in support of ABB, one being that “Process Automation” might be considered an attractive segment. So might Electrification, and ABB is self-described as being “global number 1 and 2 position in electrification and automation.” An article by electrive talks about how ABB is focused on its “sustainable transport product portfolio” which is also reflected in their Robotics segment which is said to be “the second-largest supplier of technologies for assembling the drives, batteries and bodies of electric vehicles, as well as for painting and sealing them.” Growth of the Robotics division stagnated over the past several years with a resurgence in growth seen during the past several quarters of 2022.

ABB is a decent company to invest in, in fact, it checks lots of boxes when it comes to geographically and functionally diversified businesses that align with large trends like electrification and automation. That said, our inclination is not to fall into another Teradyne trap. Industrial robotics is only a small component of ABB’s business, and it represents another “skate to where the puck will be” opportunity that’s anything but certain. Contrast this to our next company which has a dominant robotics segment that’s seeing nice consistent growth.

FANUC

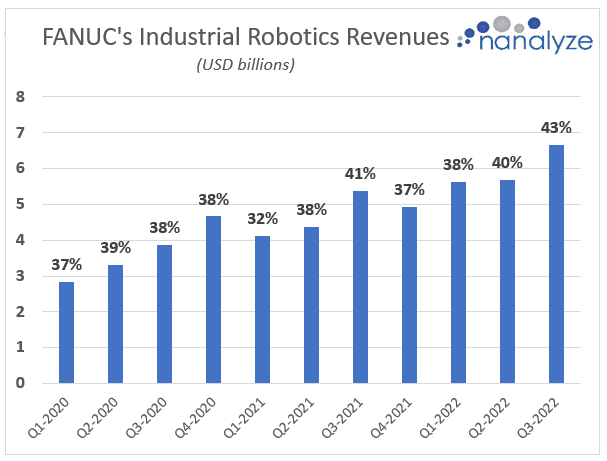

Now is the time for Americans to visit Japan given the Yen hit a 32-year low against the U.S. dollar last fall – 147 yen to one dollar – while today it trades at around 135. In other words, U.S. tourists in Japan will enjoy a 30% discount compared to what prices were several years ago. This should bode well for Japanese companies exporting products that now appear much cheaper to foreigners, but this is hardly time for discussing the macroeconomic intricacies of foreign trade. We’re here to talk about FANUC’s industrial robotics division which is enjoying consistent growth and an increasing percentage of total revenues.

With more than 100 models, FANUC claims to offer the widest range of industrial robots in the world. The company’s other segments include Factory Automation (CNC machines), Services, and a category called Robomachine which includes three primary products:

- ROBOCUT – A wire-cut electrical discharge machine is typically used to cut plates as thick as 300mm and to make punches, tools, and dies from hard metals that are difficult to machine

- ROBODRILL – A vertical high-performance machining center that makes quick work out of any milling, drilling, or tapping jobs.

- ROBOSHOT – An all-electric plastic injection molding machine that uses some artificial intelligence

The above machines may employ automation, but wouldn’t fit within the category of industrial robotics we’re seeking exposure to. To summarize, about 38% of FANUC’s revenues give us the exposure we’re looking with “Services” providing some incidental exposure. The remainder of the exposure comes from complex machinery used in manufacturing.

Yaskawa

Last, we have Yaskawa Electric, a company that created an investor deck last month for foreign investors which firmly adheres to early 1990s design principles. Similar to FANUC, Yaskawa has a robotics division that accounts for around 40% of total revenues.

Around 30% of Yaskawa’s robotics revenues come from China with 40% coming from automotive with an overall market share of 12%. The company seems to be a smaller version of FANUC that’s more difficult to follow. While FANUC’s investor decks contain basic commentary and Q&A sessions for each earnings period, Yaskawa sort of dumps all the metrics out there leaving the investor to arrive at their own conclusions. Investors will want to compare the ex-robotics exposure on offer from both FANUC and Yaskawa to see which fits best. In our minds, the customer overlap between robotics and the other divisions is important. FANUC offers industrial manufacturing equipment, a domain that seems to mesh well with industrial robotics equipment. Yaskawa offers motion control equipment which also seems to have a good overlap with industrial robotics. We came away thinking that FANUC was an easier company to follow and was also the larger of the two in terms of size and revenues with marginally higher industrial robotics revenue growth.

The Best Industrial Robotics Stock

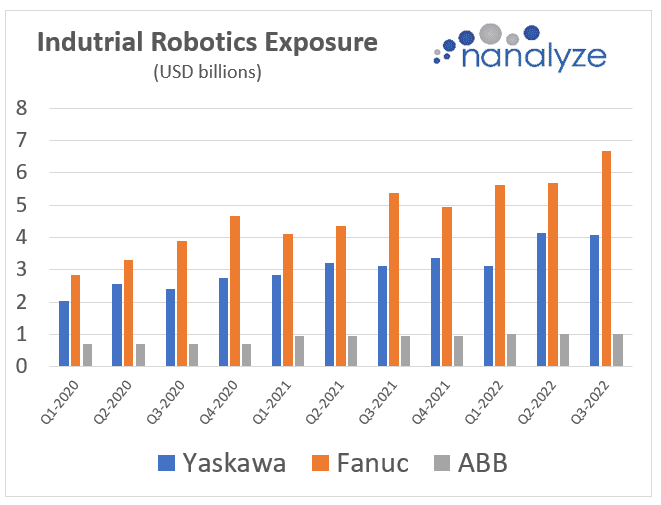

Every investor will define “best” differently, but our choice will revolve around which company offers us the most exposure to the growth of industrial robotics. Our MBAs pored through some of the most poorly constructed financial statements known to man and produced this coup de grace. Below you can find the last 11 quarters of industrial robotics revenues for each of these three companies. (ABB didn’t provide quarterly granularity so this was extrapolated from their annual numbers).

Both Yaskawa and FANUC saw revenues grow at a compound annual growth rate (CAGR) of about 7-8% over the past ten quarters while ABB saw robotics revenues rise 44% from 2020 to 2022. While producing the above chart, we suffered through one of the main pain points all investors will encounter when investing in Japanese companies – poor communication.

A Communication Problem

FANUC stands out as the company with the most pure-play exposure to industrial robotics (averaging 38% of total revenues over the past 11 quarters) along with an additional 30% exposure to robomachines for manufacturing that employ some levels of sophisticated automation. We find the firm attractive, but there are limitations to note when investing in any Japanese firm which include:

- Communication problems: Japanese firms communicate using Japanese and Engrish, the latter being equal parts endearing and confusing. FANUC does a decent job of translating key messages and provides simple investing deck supplements, so this is less of a concern.

- Foreign currency exposure: As mentioned earlier, buying shares of a Japanese firm on the native exchange requires purchasing Yen first, then buying shares in the local currency. Given Yen is close to all-time lows against the U.S. dollar, it’s not a bad time to do that, but that’s oversimplifying things. At a minimum, this foreign currency exposure helps provide portfolio diversification.

- Block trading: Shares of Japanese firms can only be traded in blocks of 100 shares which limits the ability for average retail investors to slowly dollar cost average their way into positions. Luckily, FANUC will be going through a split this month which helps alleviate the problem.

What FANUC does provide are very simple quarterly decks which are consistent across time and provide enough key numbers for us to properly analyze the company. That is, if we’re willing to accept that FANUC’s profile represents more value than growth, despite how much exposure they have to industrial robotics.

Growth vs Value

What all three companies have in common is that they represent more value than growth. For example, they’ve all been around for at least 35 years, are profitable, and pay a dividend.

| Gross Margin | Dividends | Founded | 5-Yr Revenue Growth | |

| FANUC | 40% | 2.2% | 1972 | 4.6% |

| Yaskawa | 35% | 1.1% | 1915 | 3.3% |

| ABB | 33% | 2.7% | 1988 | 2.6% |

Growth investors typically prefer that companies reinvest their profits to achieve more growth, but we’ve also noticed that foreign firms start paying dividends sooner. All three firms have healthy margins considering they’re selling hardware, and none of the above metrics – while interesting – would sway our decision in any way. We’re of the belief that FANUC most closely resembles the type of company we’re looking for in our own tech stock portfolio.

Conclusion

We’re adamant about getting exposure to proper industrial robotics solutions, something that Teradyne isn’t offering today, and not even four years from now if company management is to be believed. FANUC may not have the profile of a growth stock, but they’re a major player in industrial robotics that will incidentally offer some currency diversification to boot. If we decide to swap out Teradyne with FANUC, Nanalyze Premium subscribers will be the first to know.

Share

ADRs

FANUF or FANUY?

Great question. It’s always best to buy shares of a foreign stock on the foreign exchange its listed on using that country’s currency. Interactive Brokers is what we use to do that. If you choose to use the pink sheet market (the two tickers you listed), you’ll have very low liquidity and can choose between “foreign ordinaries” which end in “F” or ADRs which end in “Y.” Here’s an article from Schwab discussing the differences (https://international.schwab.com/investment-products/adr-stock-and-otc-stock). Again, we believe the best way to enjoy all the benefits of foreign stock ownership is to purchase foreign stocks on their primary exchange in local currencies. We talk about that here: https://www.nanalyze.com/2021/11/how-to-buy-foreign-stocks/