A Twilio Stock Analysis: It’s Complicated

Table of contents

Gene editing is a great example of an extremely difficult concept that’s easy to understand. The recipe of life is DNA. Changing the recipe of life allows you to fix defects or create new and exciting things. Understanding the technical details of how that happens isn’t necessary to understand the value proposition, and screening the 27 gene-editing stocks out there seems manageable.

In the computing domain, programming software is also an exceptionally complicated domain that can be difficult to understand based on the problems it’s trying to solve. The emergence of software-as-a–service (SaaS) business models means that you can compare and contrast various businesses using common metrics without having to understand what they do. On a spectrum of understandable SaaS firms, you might put DocuSign (DOCU) on the “easier” side and Alteryx (AYX) on the “harder” side. Generally speaking, we’re trying to avoid harder-to-understand businesses because they’re less accessible for retail investors.

Whether you analyze companies for a living or you’re a weekend warrior, it shouldn’t be difficult to figure out what any given company does. Here’s what you need:

- Latest investor deck

- Latest financial filing – 10-Q or 10-K

- Quarterly or annual earnings deck

- Transcript of latest earnings call

After reviewing these artifacts for Twilio (TWLO), we still didn’t have an intuitive understanding of what they do.

About Twilio Stock

Understanding a company is not about parroting their buzzwords in hopes that someone else can find meaning in them. With Twilio, it’s a buzzword extravaganza. The company’s mission is to “unlock the imagination of builders.” We always thought construction workers were quite creative thinkers, but perhaps not.

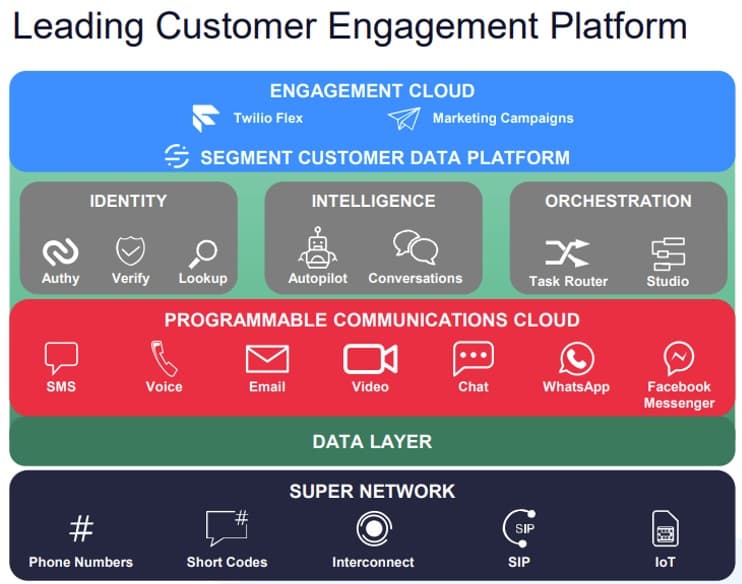

A FAQ that appears to be produced by a competent developer does a great job describing how the company works. The internet isn’t connected to the thousands of telecom providers spread across the planet’s 194 countries. Twilio does the hard work of providing a bridge between the carriers and the internet per the below diagram.

Companies need to communicate with their customers, and popular methods of communication will differ by country and include methods such as:

- Local phone numbers in 194 countries – SMS, Voice

- Communication apps: WhatsApp, FB Messenger, Viber, KakaoTalk, LINE, Telegram, etc.

- Email, chatbots, etc.

Twilio provides the infrastructure platform that lets developers embed communication capabilities into applications seamlessly. Here’s how we would describe what Twilio does in a concise manner.

Helping companies communicate with customers across all channels in a personalized manner.

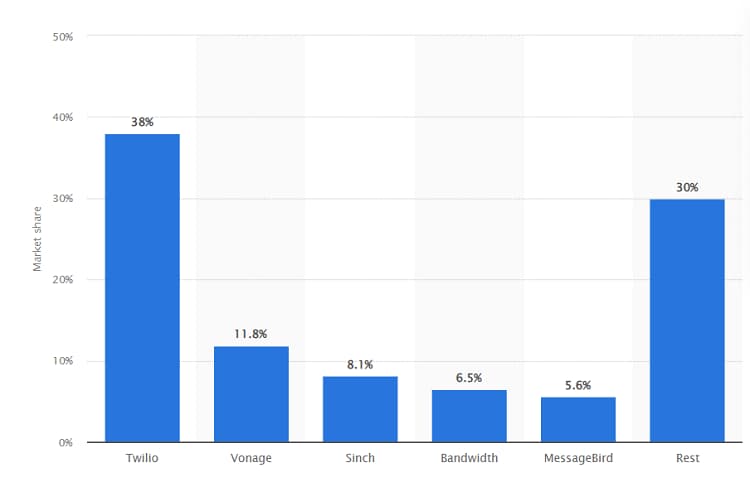

A more official name for what Twilio offers is Communications Platform as a Service (CPaaS), and Statista places Twilio in the lead for this category with a 38% market share as of Q2-2021 with IDC also reporting Twilio as having a similar leadership position.

However, when you look through Gartner’s relevant Magic Quadrants such as Unified Communication as a Service, Twilio is nowhere to be found. Perhaps that’s because their platform applications have become too broad as result of all the acquisitions that have been made to expand the capabilities of their core platform.

The SendGrid acquisition expanded Twilio’s email capabilities, while the Segment acquisition allows for personalized communication. The end result is a $13 billion company with $5 billion of goodwill on their balance sheet. As we saw with Teladoc and Livongo, having a large balance of goodwill on the balance sheet can be problematic.

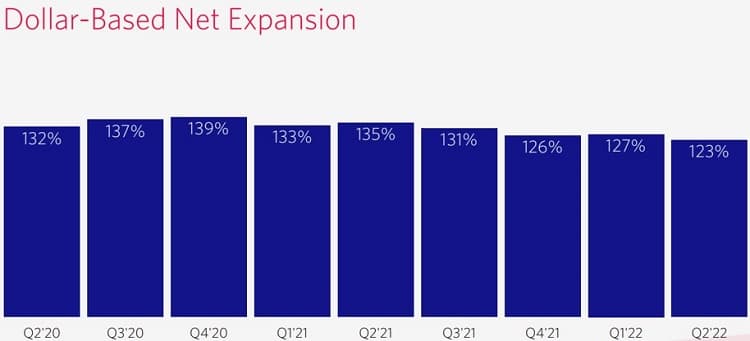

Companies are moving to digitize their communication platforms and reduce costs. In an environment where getting contract signatures is becoming exceeding difficult, there’s an appeal to an offering that starts at $5 a month and then goes upwards from there based on usage. Intuitively, Twilio’s platform seems resilient in the face of today’s bear market. Companies will always need to communicate with their customers, and once they’ve embedded Twilio into their applications, switching to another vendor could be difficult. While net retention rate appears to be on the decline, it’s still healthy at above 120%, which means existing customers are spending more over time.

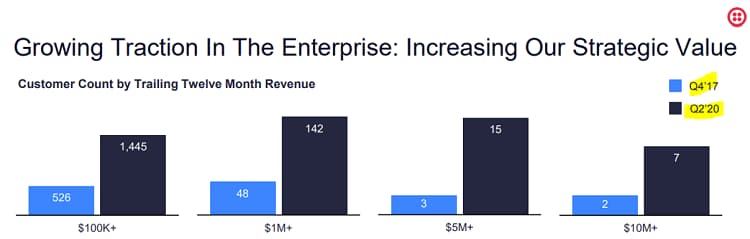

Companies of all sizes use Twilio to communicate with their customers, and they’re managing to increase spend across various revenue buckets with seven customers paying more than $10 million a year as of Q2-2020.

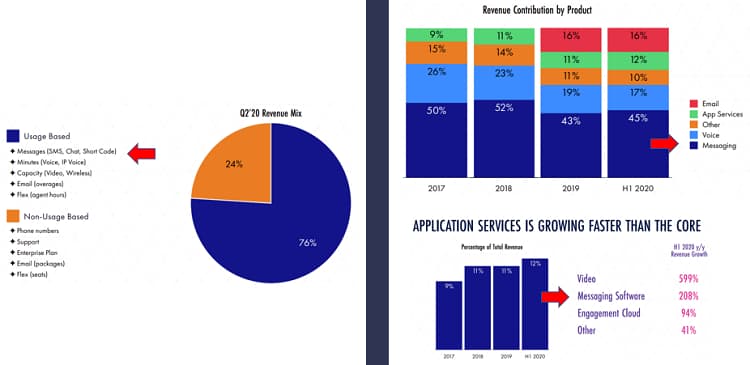

That’s the last time the company updated their investor deck, and next month’s investor day should refresh these metrics. The intermittent presentation of investor decks is characteristic of a firm that doesn’t do a very good job when it comes to investor relations. For example, the below three charts all refer to “Messaging” in a different context which makes it quite difficult to figure out what “Messaging” actually means.

There is usage-based messaging, then the messaging revenue segment, then messaging software that’s under the “Apps” revenue segment that’s grown 208% year-over-year, a number that means little without a baseline. The below chart shows their net retention rate over time, and appears to use a scale that minimalizes the impact of the decline.

Maybe those efforts could have gone into explaining why customers are spending less over time. It’s really no surprise though that Twilio’s revenue growth is lagging, because macroeconomic headwinds have been affecting all SaaS companies across the board.

Going Long Twilio Stock

If you’re thinking about going long Twilio, there’s no better time. Shares have risen +56% since their IPO compared to a Nasdaq return of +156%. That means the firm has underperformed the market while revenue growth has climbed upwards steadily. With a simple valuation ratio of three, it’s hardly considered overvalued relative to other SaaS firms. Our main point of contention surrounds the difficulty in understanding the value proposition following their acquisitions.

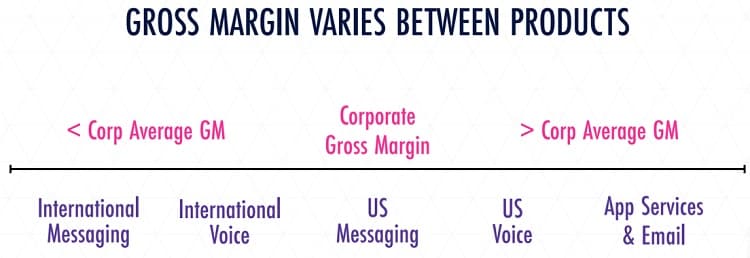

It seems like the core platform suffers from lower margins, so Twilio is adding on capabilities – apps as they’re called – which offer a much higher margin.

In 2021, Twilio’s gross margin was nearing 50%, so not half bad. At the same time, they’re burning through a mountain of cash – $500 million in the first half of this year alone. With $3.5 billion in cash on their books (net of nearly $1 billion debt), the company has a runway of about 3.5 years.

There are many components to the Twilio offering of which we don’t have any insights. For example, they talk about an IoT offering that was borne from the acquisitions of Electric Imp and Core Network Dynamics. How’s that coming along? To find out the current health of any product offering, you’d probably need an analyst to spend half a day poring through their collateral. The intermittent investor day decks don’t appear cohesive, and the earnings decks are rather sparse.

We came away from this research piece feeling like we still don’t have a sufficient understanding of Twilio’s value proposition, or what barriers to entry exist preventing companies like Cisco from encroaching on their turf. The acquisition spree makes their value proposition more complex, and the way they present this information in their sporadic investor decks doesn’t help. We don’t invest in companies we don’t fully understand, so we’ll be avoiding Twilio going forward.

Conclusion

A common response to a bear thesis is the accusation of the critic “not understanding the business.” If you need someone to explain a business model to you, that’s probably not a good investment to make. We spent an entire day analyzing Twilio’s business model and we have more questions than answers. This isn’t a company that any retail investor could easily understand, and investing in such businesses means we need to spend a great deal of time trying to figure out how the company is progressing. As Warren Buffet would say, only invest in businesses you fully understand.

Share

Your comments are “spot on” . As a matter of fact quite a few of these type of companies – have the same problem like Twilio – un understanable figures to support their expansion. Its all pure hype to gain traction. Its really great to see someone like you disecting them up so that the common folk can understand.

Thanks.

Thank you very much for the feedback! We’ve analyzed over 400 tech stocks and this might be one of the most difficult ones to digest. It’s rare to come across a company that creates more confusion than clarity with their collateral. Glad we’re not the only ones finding this company difficult to follow.

Twilio’s CEO, Jeff Lawson, is adamant that in 2023, Twilio will be profitable :

“We have said, Hey, here’s what the carrier fees have done to our gross margin. And I think investors still have said, great, but what about profitability? And so, I think we’re in the mode where we need to show you all that we are going to be profitable in 2023 and beyond.”

Got to ask you Stan. Did you find the business confusing or does it seem intuitive? Thank you for the 2023 profitability target. That’s just over one year away now!

One year ago (21st Oct 2021) TWLO reached 52 week hight: $373 (earlier in Feb 2021 it reached all time height $435).

Now it is only just avove $67. So it is -82% in 1 year !

That is nuts. Thank you for the interesting factoid!

Looking at their financials I am happy with their revenue growth: they grow revenue very consistently each year and even each quarter. I guess the company was focused mainly on growth at the expense of profitability. That was fine in the bull market. Now they will have to adjust to the realities of the bear market and more expensive money. That’s why now CEO talkes about profitability being achieved in not a distant future, possibly even 2023. I think 2023 is unrealistic, but if they move in the direction of reducing net loss, the share price would respond very positively. I think there is a good chance the share price is going to do recovery quite soon, assuming restructuring plan works (btw: they are reducing workforce by 11%).

Good comment Stan, thank you for sharing your thoughts. Most tech stocks will probably follow the broader market. If the bear keeps biting, stocks will keep falling. As someone once said, real wealth is created in bear markets.

Value your insights as always. Would be interested in your reaction to this Reddit substack analysis: https://exitvelocity.substack.com/p/twilio-the-pendulum-swings-both-ways. It sites ICD MarketScape chart (similar to Gartner) as a leader in Worldwide Communications platform. TWLO is the clear leader in the CPaaS space. I do agree that it is worth being cautious re: TWLO. Like that management cut labor force 13% and trimmed 30% growth in the face of headwinds. Simple valuation of 3 for a clear market leader is tempting.

We usually don’t allow links but we’ll leave this one as it’s very detailed and rich in information. And that’s a double-edged sword. Most retail investors don’t have the time to conduct the sort of analysis presented in that piece in an attempt to try and understand the business. That article overwhelms the reader with information, albeit quality information. To follow a stock this complicated takes time and resources most investors don’t have. Our goal is to invest in companies that retail investors can easily understand and monitor themselves in case we get hit by a bus. The need to have someone provide a regular interpretation of what’s happening isn’t optimal. The stock is cheap, revenues are growing consistently, and many investors like ARK think this is a solid business. Indeed, it appears to be sticky as switching costs are high. That said, for all the reasons discussed in this piece, we don’t find this to be a stock we want to get involved in. Thank you very much for posting this as the author makes a very solid case for the bull thesis. Pull the trigger on some shares if you believe the bull thesis with conviction. We only have 40 maximum slots in our tech stock portfolio and we need to be quite selective, so this one is a pass. It may make sense for others who see value we don’t. Again, thank you for sharing John!