Investing in the Best Wind Turbine Stock

Table of contents

Disruptive growth doesn’t always equate to profits. If you would have invested in the Invesco Solar ETF when it debuted nearly 15 years ago you would have 66% less money compared to a Nasdaq return of +534% over the same time frame. So much for blaming the 2008 market crash for solar’s underperformance. Just because you see solar panels popping up on every roof doesn’t mean solar panel manufacturers are a lucrative investment, and the same can be said for wind turbines.

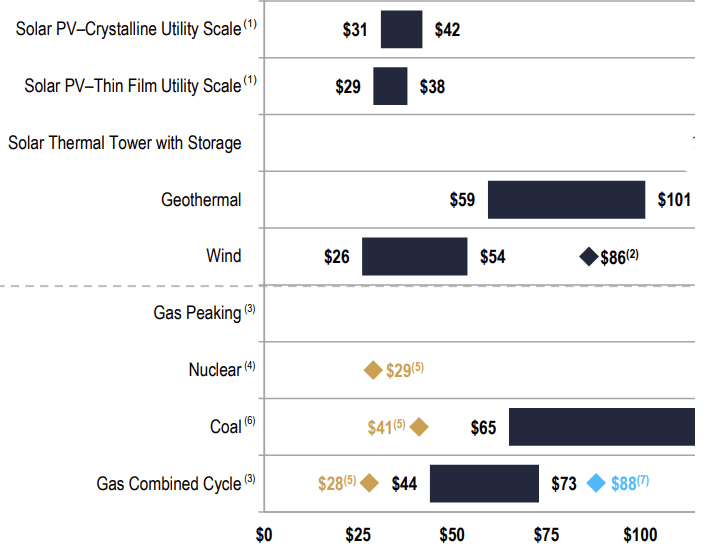

Renewable energy has become such a loaded topic that it’s tough to discern what’s actually going on, so we’ve always looked to Lazard’s levelized cost of energy (LCOE) as an indicator of success. With all the penalties and subsidies removed, wind appears to be competitive with coal, and in some cases cheaper than coal.

Of course, we also need to consider the need for storage and whether wind energy deployments will play well with whatever infrastructure they attach themselves to. Regardless, the demand for wind turbines continues as wind energy adoption increases. Today, we want to find the leading wind turbine manufacturer and see what that investment thesis looks like.

The Biggest Wind Turbine Manufacturers

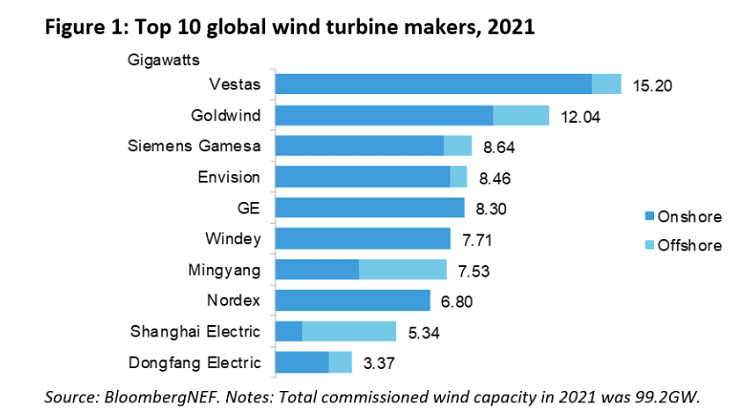

BloombergNEF produces a research report every year that ranks wind turbine manufacturers based on capacity being brought online, the latest of which can be seen below.

While the rankings vary from year to year, the past three years have seen the following five companies vying for leadership in the wind turbine space:

With Envision being a private company we’re left with four contenders.

This summer, General Electric announced their portfolio of energy businesses – GE Renewable Energy, GE Power, GE Digital, and GE Energy Financial Services – will come together as “GE Vernova” and be spun out as a separately traded entity in early 2024. But until that happens, there’s not much to discuss. That leaves three remaining stocks which provide distinctly different exposures based on their locales – Spain (Siemens Gamesa), Denmark (Vestas), and China (Goldwind). Here’s how these three firms compare based on market cap, 2021 revenues, and simple valuation ratio.

| Company | Market Cap | 2021 Revenues | Simple Valuation Ratio |

| Vestas | 25 | 15.6 | 2 |

| Siemens Gamesa | 12 | 10.2 | 1 |

| Goldwind | 8 | 6.4 | 1 |

Vestas is the leader by size and revenues, something that irks Siemens. You see Siemens – an $85 billion German industrial conglomerate – owns 35% of Siemens Energy which owns 67% of Siemens Gamesa, a company that trades on a Spanish exchange. If Siemens Energy can increase their ownership to 75%, they’ll be able to delist Siemens Gamesa and realize a whole bunch of synergies. In short, Siemens Energy believes Siemens Gamesa could be a lot more competitive when whipped into proper shape. The deal is expected to close in the second half of this year, so that leaves us with two companies remaining – Vestas and Goldwind.

We recently wrote about The Danger of Chinese Stocks which extends beyond just risky VIE structures. Since Goldwind trades as an H Share we don’t have to worry about the VIE structure risk, but there’s country concentration risk to be concerned with – over 92% of Goldwind’s revenues come from China. The financial results are provided in an unaudited fashion – in RMB instead of USD – which means it’s far more difficult to monitor the company over time. Investing in China is appealing, and maybe there’s merit in digging into Goldwind, but we’re always looking for the market leader in any niche. When it comes to wind turbines, one company is the clear leader by market cap and revenues – Denmark’s Vestas.

Vestas Under Pressure

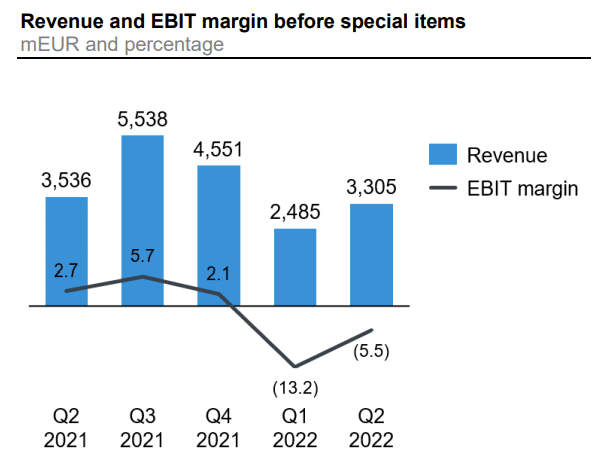

Several years ago we wrote about Vestas in a piece titled The Largest Wind Turbine Manufacturer in the World noting that pressure was being placed on their margins as the industry matured. That problem has only intensified as supply chain problems and inflation wreak havoc on their top and bottom lines. What was once a marginally profitable business is now a money-losing business, at least for the first half of this year.

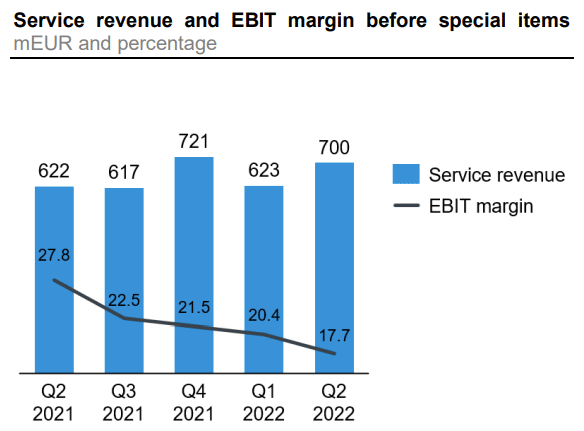

Understanding the profitability problem requires understanding the business model which is to supplement low-margin hardware (wind turbines) with a high-margin services offering.

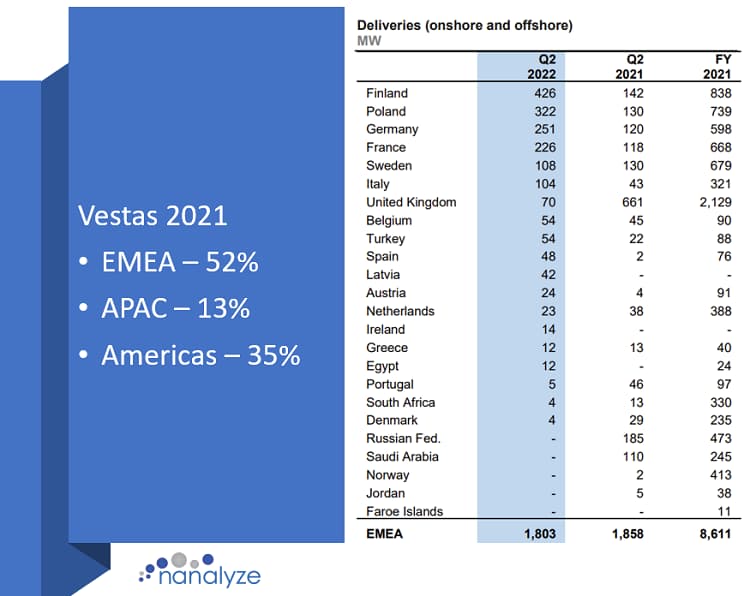

Vestas divides their business into two segments – Power Solutions (low margin hardware) and Services (higher margin services) – which constituted 79% and 21% of total 2021 revenues respectively. Combined, these two segments have historically realized a gross margin of around 10% over the past several years, a number that’s been on the decline over time. More recently, the margin for Services has been trending in the wrong direction.

Last quarter’s margin drop was attributed to “lower profitability on certain projects in USA and Africa” which sounds temporary, but the remainder of the deck is riddled with mentions of cost inflation and supply chain issues. Chinese firms that sell domestically won’t need to deal with the sort of complexity Vestas deals with as they conduct business across numerous geographies. Over half of 2021 deliveries were to the EMEA region across a broad number of countries as seen below:

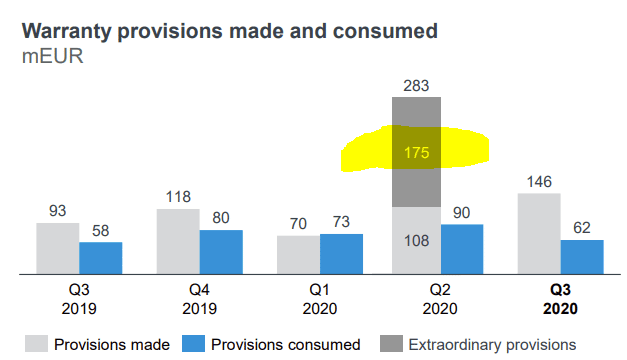

Vestas’s tight margins mean investors should pay attention to metrics like “warranty provisions” which are increasing alongside inflation. Selling a wind turbine means you need to service it when there are problems, and Vestas saw lightning strikes wreak havoc on their warranty claims several years back.

The taller the wind turbine, the more likely it is to be damaged by lightning, says an article by Power Technology which claims “around 70% of all the strikes measured in turbines are actually starting on the blade and triggered by the turbine.” In Q2-2020, Vestas recorded 175 million euros in exceptional warranty costs to address an issue with “high intensity lightning” damaging blades, something the company didn’t elaborate upon much. It also raises concerns about commitments Vestas has made regarding the availability of their turbines.

Lost Production Factor (LPF) measures “potential energy production not captured by Vestas’ wind turbines.” The higher the number, the more inefficient the turbines are. When LPF started rising in late 2020, Vestas said that “it continues at a low level for the wind power plants where Vestas guarantees the performance.” Since then, it’s continued to rise and we’re no longer provided assurance as to how this impacts guaranteed performance contracts. Somehow the idea of guaranteeing performance in the face of nature for a relatively new technology sounds foolhardy.

Every company is running into problems in today’s bear market as corporations around the globe tighten their purse strings. There is no shortage of ESG investors lining up to buy green bonds from Vestas if more funding is needed. We’re just not convinced that the wind turbine business is a compelling way to play the wind energy thesis. If you’re a utility like NextEra Energy (NEE) and the company selling you wind turbines guarantees performance, or provides warranty coverage for lightning strike damage, that’s a nice place to be in. Maybe the 18-billion-euro backlog is because Vestas sweetened the pot quite a bit to land sales, and the reality of those commitments is coming to fruition. Or maybe these are all temporary problems that will eventually go away, but Vestas doesn’t appear to offer the potential upside needed to offset their seemingly risky business model.

Invest in Vestas?

If you’re bullish on wind energy infrastructure then Vestas is clearly a leader in this space with great international diversification, but not much wiggle room when it comes to operating profitably. The high-margin Services division is expected to carry the Products division, but both are suffering from cost inflation and supply chain problems. These headwinds may be temporary, but they show just how quickly a low-margin capital-intensive business can run into problems.

With our largest technology stock holding being the largest producer of wind energy in the world, we’re not looking for more exposure to wind. Given the increasing pressure on margins being faced by Vestas, we’re not convinced they’ll thrive in the face of a sustained bear market. Consequently, we’re removing Vestas from our tech stock report and leaving it in our catalog as an “avoid.”

Conclusion

Ideally, we like to see hardware products offered alongside high-margin services so a business can operate sustainably when hardware growth subsides. With a large backlog of orders, Vestas will be busy for some time. With average turbine life expectancy of 20 to 25 years, there’s always replacement hardware to consider as well. We’re just not convinced that this will be a profitable cash-generating enterprise of the type we’d like to own.

Share

Superb piece! The logic connecting the dots flows impeccably. Thanks for this! 🙂

You are quite welcome Ken, glad you enjoyed it!