What Institutional Ownership Really Means

Table of contents

If you’re a hiring manager in finance who recruits fresh grads, here’s a great thing to tell them. “Take the most sophisticated financial concept you know and explain it to me like I’m your grandmother.” The effectiveness is the psychological challenge. Explain a simple concept perfectly and it implies their depth of knowledge might be lacking. Explain a sophisticated concept poorly and it implies they didn’t truly understand the material. For the interviewer, it’s perfect because few hiring managers spend their time studying financial concepts they promptly forgot upon exiting university. If it’s a solid candidate, you just might learn something.

Of course, you don’t bring out the big guns in the first five minutes. You soften the mood first and tell them how impressed you are they accomplished some meaningless academic feat. Then, you start out with a simple question like, “tell me the difference between a passive manager and an active manager?”

Passive vs. Active Management

Let’s start by talking about stock indices which are simply baskets of stocks selected and maintained based on a published methodology. For example, MSCI produces a collection of global indices that constitute nearly all publicly traded companies in the world with sufficient liquidity and size. Once that universe is compiled, then you can slice and dice it into sub-indices such as country, size, growth vs. value, and the list goes on.

The Index Industry Association (IIA) counts more than 3 million indices being produced by its members and there are between 40,000 and 100,000 publicly traded companies globally (depending on who you ask). That means there are now 30X as many indices as there are stocks. Why so many? According to the IIA:

The results show that benchmarking is clearly the predominant use for indexes around the world. With over three million indexes available, asset managers and investors want choices when choosing a benchmark that best represents their portfolio and the underlying market.

Credit: IIA

Ah yes, the old create your own benchmark trick. It’s just another way investment managers try to convince their clients they’re creating alpha when only 5% manage to over the long run. You see, active managers are judged by how well they can beat the performance of a benchmark index, so choosing or creating various indices may yield more favorable results. We have an actively managed portfolio, but we don’t spend much time analyzing our performance because we can always torture the data and make it tell you we’re the second coming of Nostradamus. We’d rather spend our time providing you with quality research than working on window dressing.

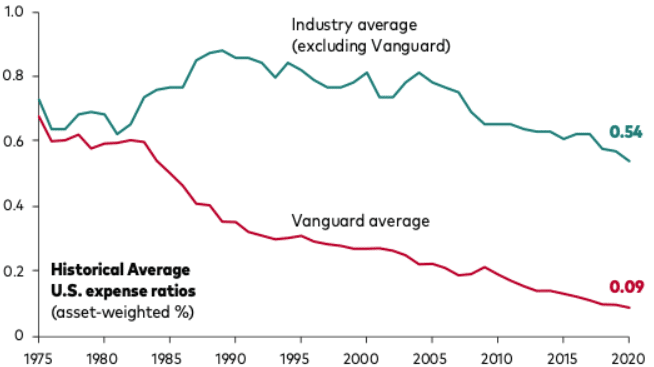

The proliferation of indices means there are also plenty of ETFs and funds tracking them passively. When you’re a passive manager, your job is to match the performance of a benchmark index. Mimicking the returns of an index is not as simple as just buying all the stocks and then holding them. It’s much more difficult than it sounds, and the job of a passive manager is to reduce tracking error, a common measure that shows how they deviate from the index benchmark they’re tracking. Nowadays, low-fee ETFs that track large indices are highly automated so little human intervention is required. In other words, stick with Vanguard ETFs and you’ll do just fine.

So, let’s review what we learned. Passive managers hold stocks because they have no choice, while active managers choose to hold stocks. This means institutional ownership doesn’t always mean firms are bullish on a particular stock, it just means they’re holding it.

Institutional ownership is the amount of a company’s available stock owned by mutual or pension funds, insurance companies, investment firms, private foundations, endowments or other large entities that manage funds on behalf of others.

Credit: Investopedia

“Institutional ownership percentage” is the percentage of shares outstanding that is owned by financial institutions and can easily be looked up at Nasdaq’s website (see below example).

The Meaning of Institutional Ownership

Today, institutional investors hold 41% of global market capitalization, much of which is in the form of passive indexing. For these investors, it may be quite rational to give little attention to risks and opportunities in individual companies. And as a consequence, not enough resources may be dedicated to the capital markets’ key functions, which are to scrutinize individual corporate performance and provide new promising companies with capital that help them grow.

Credit: OECD

When analyzing institutional ownership for any stock of a reasonable size, a certain percentage will be attributed to passive ownership (Nasdaq’s percentage does not distinguish between active or passive). Companies like BlackRock and Vanguard don’t hold shares of MicroVision (MVIS) because they believe there’s loads of alpha to be generated from companies with several decades of failed promises, they do so because it happens to be part of an index they’re tracking. Now we see why size matters, and index inclusion is such a big deal for companies.

When you’re examining institutional ownership for a stock, expect the world’s largest asset managers to occupy the top spots. Here’s a list of the largest asset managers in the world by assets under management (AUM) for reference.

Now, look at the largest institutional owners in Microsoft.

It’s almost a given that the top two asset managers in the world – Vanguard and BlackRock – will be the largest institutional owners of the world’s largest companies because of all the passive investment products they offer. But it’s a bit more complicated than that. For example, in looking at the five largest U.S. tech companies, you’ll notice something odd. See if you can spot the outlier.

| Company | Institutional Ownership | Beta |

| Microsoft | 70% | 0.93 |

| 65% | 1.08 | |

| Apple | 59% | 1.24 |

| Amazon | 59% | 1.33 |

| Tesla | 42% | 2.18 |

Tesla has much lower active institutional ownership because it’s a particularly risky stock. That’s evident by beta (a measure of volatility), but there’s also a more subjective explanation that’s apparent if you follow Elon Musk on Twitter.

The Tesla Example

Tesla may have lower institutional ownership because of its controversial leader. That’s precisely why we never dabbled in the firm even though we have it listed as a “like.” Yes, it’s possible to lob praise at Elon Musk and not be a Tesla investor or drive one. We can also say that he’s an arrogant, pot-smoking, egomaniac who thinks his crazy ideas can change the world and procreates faster than the media can keep track of.

But enough about Mr. Musk’s finer qualities. There are numerous reasons why Tesla investors should lose sleep at night over the volatile individual who dominates the organization – and the other half a dozen organizations he runs. Five years ago, Mr. Musk lost his Chairman of the Board seat because he pissed off the SEC by doing naughty things on Twitter. Anyone who hints that the Russians are going to kill him while promoting cryptocurrencies on Twitter and posting memes like the one below is going to turn off risk-averse investors.

Yes, the man who said he’s going to start a university called the Texas Institute of Technology and Science (TITS) is a powder keg. Imagine how uncomfortable he makes Tesla’s legal team feel, then realize how his behavior turns off many strait-laced fund managers who already despise the fact they have to hold passive ownership in the first place. Of the largest technology firms in the world, Tesla’s institutional ownership is the lowest. Contrast that to active managers like ARK Invest that believe Tesla is only just getting started.

Aping Active Managers

It’s never advisable to mimic the actions of an active manager, yet people do it all the time. In our world, the most notable active manager is ARK Invest, a firm that dominates institutional ownership for a number of stocks we wouldn’t touch with a ten-foot pole – like Nano Dimension (NNDM).

The investment decisions ARK makes aren’t cut and dry. They might reduce a position because of an opportunity cost they’re incurring, or it could be because their thesis changed, or they just might need to sell some assets as active managers do when there are outflows. Retail investors should always enter a position based on their own convictions so they’re not left wondering when to sell. When you have formed a thesis based on your chosen methodology, you’re then able to assess when it changes. Every investment we make is documented as to why we went long. Every time we sell a stock, it’s because either our thesis changed, or revenue growth stalled. Key takeaway: don’t put too much stake in what active institutional investors do.

The same holds true for corporate ownership. You’ll often hear cheerleaders offer up some large corporate investment as a vote of confidence, but reading the fine print tells a different story. Amazon made out like a bandit with their investment in Plug Power (PLUG) because they were given terms so favorable they couldn’t possibly lose. Beware of firms that give away chunks of equity to BSDs in exchange for validation. Also, watch out for related party action. When Palantir (PLTR) purchased shares in several dozen unrelated SPACs in exchange for usage of their platform, it wasn’t the vote of confidence it seemed to be.

We’ll finish this off with one final thought. Companies that have a high percentage of institutional ownership – let’s say 80% or higher – have some inherent characteristics that institutions find desirable. You’ll never be able to figure out the reason for the high ownership, but it’s usually a good sign. Proceed with cautious optimism.

Conclusion

Passive institutional ownership says very little about company quality, while active ownership tells us that some firm is bullish for some reason we often don’t know. A high percentage of distributed institutional ownership – let’s say 80% or above – can be a good sign, but that shouldn’t inform your own investment decisions which should always be based on your own due diligence and thesis. Those who choose to mimic what successful active managers do won’t sleep well at night. More importantly, they’ll never learn how to become better investors by attending the school of hard knocks.

Share

This is a great article. Whatever prompted you to write it. I learned a lot especially since I use that metrics after I decide on a stock.

Regards

Eva

Good question Eva. You’re quite observant. The idea was prompted by a Bloomberg article that was discussing Tesla’s lower level of institutional ownership relative to other large tech players. That led down a rabbit hole from this piece emerged. Really glad you found it useful.

Out of curiosity Q: for ETFs that are purely index based, are there rules or guidelines over the ratio of stocks they invest in? Another way to ask if there was a pure top 100 index ETF from Vanguard and Blackrock (ie same product) a do they invest the same % for the stocks?

Great question. Each firm will have a different way of providing exposure as there are different methods such as full replication, optimization (or sampling), or synthetic replication. It’s more complicated than most people think. A passive manager needs to have an excellent understanding of the index methodology to anticipate changes as well. A lot of that should be automated now but maybe a passive manager will pop by and let us know if that’s the case 🙂