Senseonics Stock: Overvalued and Struggling to Compete

Table of contents

Whenever one of your friends starts asking certain questions, you know what’s coming next. “Wouldn’t you rather work a lot less than you do?” “Could you use more money?” “Are you worried about your financial future?” These are all primer questions leading up to a pitch for whatever multi-level marketing Kool-Aid was pitched to them by someone else. “How much do you spend on cleaning products every month?” Nothing mate. Here in Hong Kong, we use the age-old cleaning method that’s worry free – indentured servitude.

In the same fashion, we’ll often see similar comments ambulance chasing some insightful piece our analysts wrote. Some punter will pop by with the setup question. “Say, completely random thought here, but which stock would you invest in – Dexcom (DXCM) or Senseonics (SENS)?” Then their wanker friend will smash it out of the park with their “Senseonics is a no-brainer if you want a 69 bagger mate!” reply. We see right through that rubbish, and it was the first sign we’d possibly encountered another meme stock.

The people who cheerlead stocks like Senseonics don’t realize they’re damaging the company’s reputation by engaging in such behavior. It usually ends up with some volatile overpriced stock that scares away serious investors.

About Senseonics Stock

Let’s start with the bull thesis. Constant glucose monitoring (CGM) has proved to be quite the windfall for firms like Dexcom (G6) and Abbott (Freestyle Libre 2) that peddle their devices ubiquitously on American television. “Tired of diabetes getting in the way of your wingsuit aspirations mate? Try this CGM device.” These two firms dominate the airwaves and market share for CGM solutions. One of the biggest medical device companies in the world, Medtronic, hasn’t been able to make progress stealing market share from Dexcom and Abbott because both are so well entrenched, but there’s more to the story than that.

Spend some time investigating what people say about these three CGM devices and the Medtronic Guardian 3 CGM monitor stands out because it requires two pinpricks a day to calibrate which defeats the purpose. CGM devices are supposed to be replacing the need for finger pricks. That’s the whole point. Saying that your CGM device is more accurate because patients who use it need to calibrate the device twice a day with finger pricks isn’t a competitive advantage. Medtronic seems to have recognized this as the latest product they’ve developed – the Guardian 4 sensor – doesn’t require calibration.

Review after review talk about how Dexcom is just so much easier to use. And that’s where Senseonics comes in with their “implant every 180 days” sensor, but the problem is that it requires two finger pricks a day as well – at least for the first 21 days, then it moves to one finger prick a day. Well, that’s what it says on the tin, but digging deeper shows us how variable this result is based on each individual with the number of calibrations potentially varying from day to day.

In the Eversense E3 pivotal clinical trial (PROMISE Study), the system required primarily 1 cal/day, prompting for a median of one-calibration per day 62% of the time, and two calibrations per day 38% of the time, after day 21.

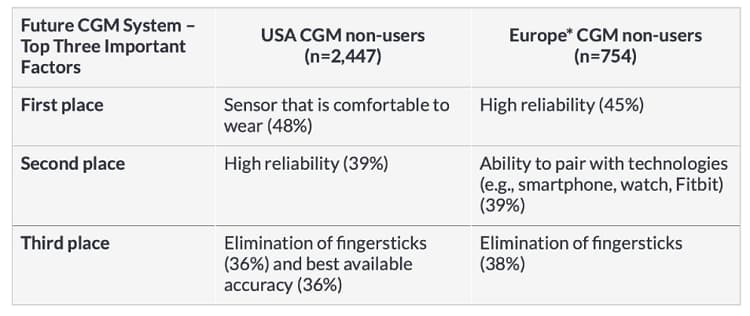

Sure, people want a longer-lasting sensor. It’s one of the top functionality requests made by CGM users who were surveyed. But people also don’t want to continue pricking their fingers. For potential CGM users, not having to prick your finger was an important factor when visualizing the ideal CGM solution of the future.

In looking back at the Senseonics roadmap they provided in their 2015 10-K we see they planned to remove the need for calibration and begin clinical studies for that feature in 2017. That doesn’t seem to have happened.

The Origins of Senseonics

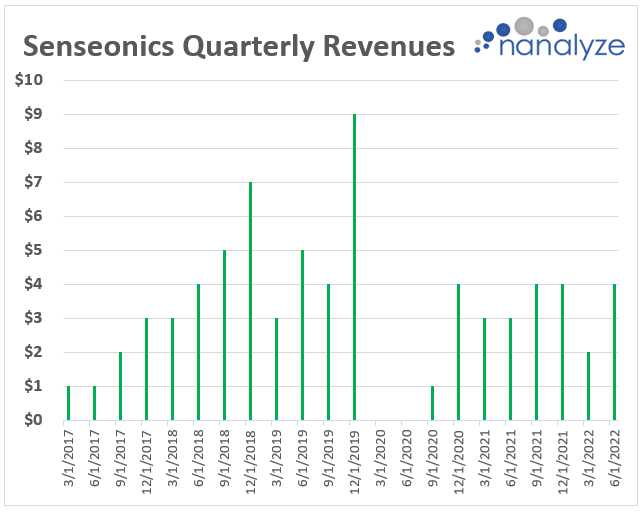

From its inception in 1996 until 2010, Senseonics Incorporated devoted substantially all of its resources to researching various sensor technologies and platforms. Beginning in 2010, the company narrowed its focus to designing, developing, and refining a commercially viable glucose monitoring system – Eversense. (That was four years after Dexcom launched their first device.) Six years later, Senseonics had an initial public offering which was followed by commercialization in 2017. Over the next five years, they spun wheels and never managed to gain much traction. Here’s what quarterly revenues look like for Senseonics.

The drop in revenues for 2020 is well documented by a Healthline article published at the time which describes how the company “laid off about half of their workforce, retaining only researchers, quality control experts, and a few salespeople — while they search for new investors, partners, and/or a possible acquisition.” The old restructuring kiss of death, and that same article goes on to talk about challenges they’ve faced. “The need for surgical insertion and removal procedures was a hard sell for many patients and doctors alike,” says Healthline, and “Eversense couldn’t compete with the FreeStyle Libre, and as a result, Roche had a stockpile of Eversense CGMs it couldn’t sell because of lower-than-expected demand.” That’s a good segue into talking about customer concentration risk.

Roche and Ascensia

Customer concentration risk isn’t the only concern we see when looking at the history of partnerships Senseonics has had, starting with Roche. Here’s the timeline:

- In May 2016, we entered into a distribution agreement with Roche which granted Roche the exclusive right to market, sell, and distribute Eversense in the EMEA, excluding Scandinavia and Israel and 17 additional countries. Roche was obligated to purchase from us specified minimum volumes of Eversense XL CGM components at pre-determined prices.

- On December 12, 2019, we further amended the distribution agreement to lower minimum volumes for 2020 and increase pricing for the remaining period of the contract.

- On November 30, 2020, we entered into a final amendment and settlement agreement with Roche to facilitate the transition of distribution to Ascensia as sales concluded on January 31, 2021

If the terms of the Roche agreement sound familiar that’s because the current contract Senseonics has with Ascencia offers similar terms. With the recent FDA approval received by Senseonics this past February, one would think that means revenue growth is finally here. Think again, because Senseonics nearly halved their revenue guidance when the approval took place which left analysts scratching their heads. An excellent article by Medtech Dive talks about how there’s a puzzling disconnect between what Senseonics sells and what patients are actually using.

The excess inventory theory is underpinned by a disconnect between the number of patients who are using Senseonics’ devices and the company’s revenues. As the Craig-Hallum analysts explained, installed patients fell from 5,000 at the end of 2020 to 3,200 at the end of 2021. Yet, sales rose from $5 million to $14 million, suggesting Ascensia has excess inventory.

The key metric to watch here is “installed patients.” That number should not be falling as this demonstrates poor retention. If customers don’t want to use the Senseonics platform, it doesn’t matter how long sensor life is. In fact, investors are probably starting to see the problem with this business model. Dexcom commands the value it does today because more than 80% of their revenues come from disposables. Just how successful would Dexcom be if those sensors lasted six months or a year? Hard to say, but their stock wouldn’t have nearly the same valuation, which is why the Senseonics business model will never hold the same appeal as Dexcom, no matter how snazzy they make their product which has been under development now for 12 years.

The Extreme Valuation of Senseonics

The great thing about our simple valuation ratio is that it provides a great litmus test as to whether or not a stock is overvalued. In the heydays of the technology boom, we decided that anything over 40 was too rich for our blood. These days, anything above 20 would be considered overvalued relative to a broader universe of tech stocks. Here’s a look at the ratio for a handful of stocks in our tech stock catalog.

| Company | Simple Valuation Ratio |

| Senseonics | 66 |

| Snowflake Inc | 32 |

| Butterfly Network | 27 |

| CrowdStrike | 24 |

| Guardant Health | 15 |

| Dexcom | 14 |

| 10X Genomics | 12 |

| Schrodinger | 12 |

| Dynatrace | 12 |

| C3 | 8 |

| Illumina | 7 |

| Splunk | 7 |

| Pure Storage | 4 |

| Teladoc Health | 3 |

| Invitae | 2 |

Can anyone find the outlier? That’s right little Johnny. Senseonics has a simple valuation ratio of 66 which is simply absurd. Here’s how the stock price would look at various valuations.

- Senseonics is valued same as Snowflake: $1.05 per share

- Senseonics is valued same as Dexcom: 46 cents a share

- Senseonics is valued around universe average of 10: 33 cents a share

Buying shares in a firm that’s extremely overvalued is a recipe for disaster, and it’s precisely why serious investors dislike firms whose investors stir up hype based on a cursory look at the bull thesis. Poke around social media and it’s easy to see why Senseonics is overvalued. From Reddit to Twitter you’ll find cheerleaders pumping the prospects of a life sciences stock that’s always on the cusp of greatness.

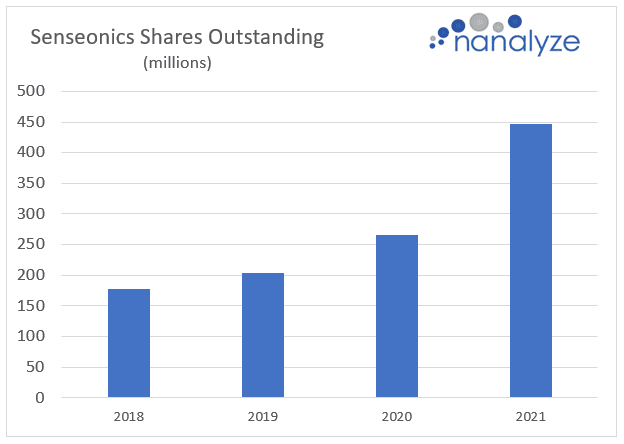

That last article is what we probed today. Turns out Senseonics isn’t being held back by their meme stock status, they’re being held back by their inability to grow sales for a product they’ve been working on for over a decade. Now we’re led to believe that the recent FDA approval is the panacea for all the problems they’ve encountered thus far. The firm’s weak guidance for 2022 implies that there’s more than just pending FDA that’s keeping adoption progress at a snail’s pace. Investors who decide to get on board with Senseonics’ promises of future riches should pay very close attention to the “installed patients” metric. If that number doesn’t trend upwards, it doesn’t matter how many units they can pre-sell to their key partner du jour. And while they’re struggling to gain traction, shareholders are being diluted at a faster rate than ever. Just look at how much dilution has taken place over the last four years.

Until this company can consistently grow revenues and their install base, there’s absolutely nothing to see here.

Conclusion

Investors are spoiled for choice these days when it comes to quality stocks that are more reasonably valued as a result of today’s bear market. Investing in an overvalued meme stock that’s struggled to commercialize their products for over a decade isn’t a good idea when that money could be invested in solid growth companies like Dexcom. Even if Senseonics stock wasn’t extremely overvalued, there’s nothing to see here until they start growing revenues and their install base.

Share