Protolabs Stock vs. Xometry Stock. And the Winner Is?

Table of contents

Here’s a thought exercise. Let’s say you invested in a stock that you believed was the market leader. Later, another company goes public which looks attractive – high growth and challenging the leader. The leader’s growth stalls and share price plummets. You’re underwater holding the “leader” and missing out on the upside of the challenger. What do you do?

You do not sell a quality company when shares are depressed. In other words, you don’t lock in the losses on the “leader” to then invest in the challenger. In a situation like this, you might hedge, and also start accumulating a position in the challenger. That’s exactly what we’re considering doing with Protolabs (PRLB) and Xometry (XMTR).

The Distributed Manufacturing Opportunity

Let’s start by talking about the opportunity for distributed manufacturing which is a subset of the $35 trillion global manufacturing industry, $5 trillion of which can be found in the United States. It’s tough to conceptualize just how big a trillion dollars is, so maybe this diagram will help.

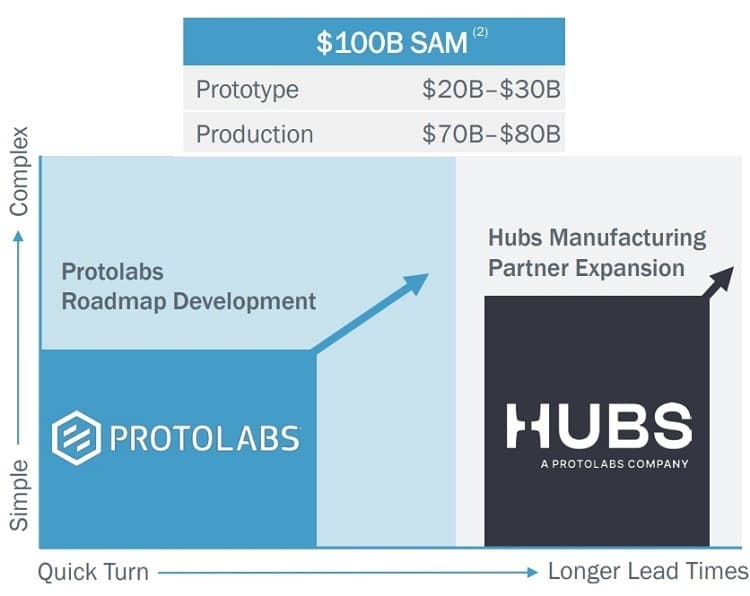

Of the $35 trillion manufacturing pie, $260 billion of that involves “custom manufacturing” of the type that companies like Protolabs and Xometry might address with their distributed manufacturing solutions. Protolabs is a bit more conservative in their estimates, putting their serviceable addressable market at around $100 billion.

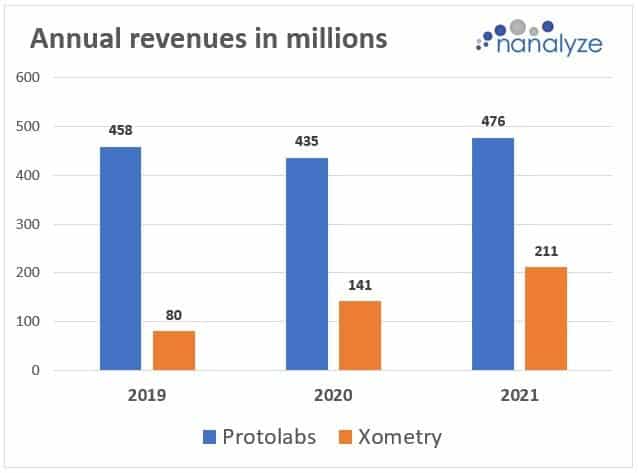

The combined revenues for both companies in 2021 won’t even come close to clearing $1 billion, so there’s a lot of room for growth here. It’s not a zero-sum game, and there’s plenty of blue ocean total addressable market (TAM) such that Protolabs and Xometry can grow for quite a while without stepping on one another’s toes.

When we approach any disruptive technology theme, our goal is to find the leader and invest in them. Prior to the emergence of Xometry, Protolabs was the undisputed leader in distributed manufacturing, at least when it came to publicly traded pure-play stocks. Then, Xometry came into the picture.

A Tale of Two Business Models

When Xometry announced their IPO in June 2021, we compared the business model of the two companies in a piece titled Xometry Stock – An On-Demand Manufacturing Marketplace. We proposed that the Protolabs business model – to do all the manufacturing in-house – was superior because it gave them a closed-loop that would produce loads of valuable big data and allow them to control quality. Xometry’s “asset light” business model simply farms out all the production jobs to over 1,400 contract manufacturers, using artificial intelligence to perform predictive analytics and provide instant price quotes. Some of our readers challenged us on this, proposing that Xometry’s business model was superior.

Operating a curated platform that allows for working with first-class suppliers while making use of their respective core competencies and different cost structures will ultimately lead to better results in terms of pricing and quality than manufacturing everything-in-house. Isn’t this the reason why Protolabs acquired 3D Hubs?

Credit: Nanalyze reader Adrian

Our community moderator gave some wishy-washy response to the above comment because that’s their job, but the point Adrian makes is a good one. The specialization on offer from 5,000 contract manufacturers should allow you to offer better pricing, while a sufficient rating system should ensure that quality assurance is maintained over time. Furthermore, the move Protolabs made to acquire 3D Hubs – a company with a similar business model to Xometry – further supports this notion. Indeed, the most recent investor deck by Protolabs is riddled with references to 3D hubs suggesting they’ll play a key role in the company’s growth going forward.

Protolabs Stock vs. Xometry Stock

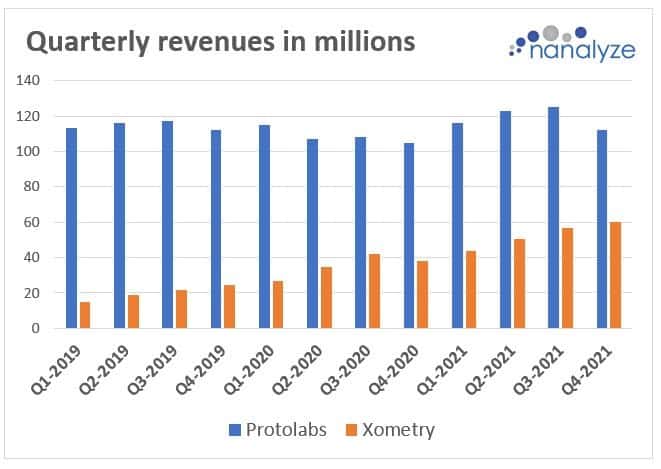

As we approach the end of the year, we’re able to see just how each company might fare based on three quarters’ worth of results, plus each company’s fourth-quarter estimates. We used the lower range of the Q4-2021 guidance provided by each company to produce the below chart.

Xometry is clearly growing much quicker than Protolabs over time. It’s also clear that growth for Protolabs has stalled. Let’s talk about how they might turn that around.

Protolabs Stock

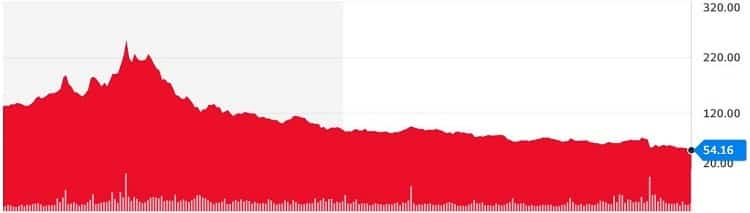

We’ve had some subscribers ask us about purchasing Protlabs wondering if they’re catching a falling knife. And who could blame them for asking such a question when the stock price performance chart looks like this.

We can only say that investing in a profitable company with a broad customer base with growing revenue growth, albeit slow growth, means there’s some implied support for the share price. If the company’s share price becomes too depressed, they might be acquired by another company, or a private equity firm might see value and acquire them. That implied support should alleviate some of those falling knife concerns. As we’re currently sitting on a fully realized position in Protolabs that’s down (checks with broker) -40%, we’re more concerned with how they’ll resume growth.

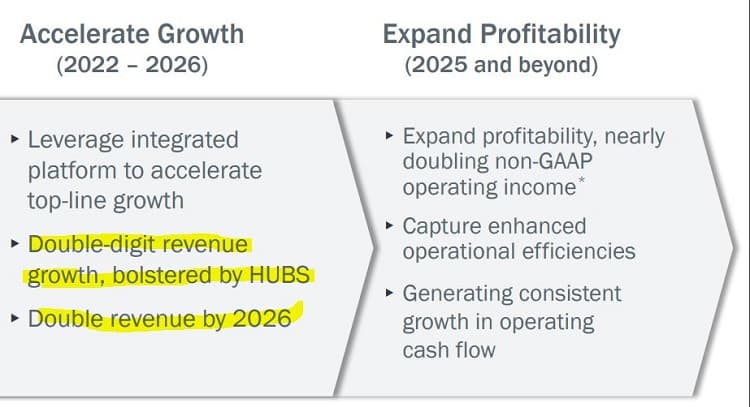

The Protolabs management team articulates their plan for growth in a May 2021 investor deck that’s riddled with mentions of 3D Hubs. An accompanying fact sheet talks about how 3D Hubs grew revenues at a +200% compound annual growth rate (CAGR) from 2017 to 2020 with 2020 revs for 3D Hubs being $25 million. That’s some crazy growth, but without any detail, tough to analyze. We do know that Hubs generated $8.8 million of revenue in Q3-2021, so that’s $35.2 million annualized. PRLB had $125 million in revs for Q3-2021 and Hubs made up $8.8 million of that – about 7%. The aforementioned 112-page investor deck makes multiple mentions of 3D Hubs playing a key role in the resumption of growth.

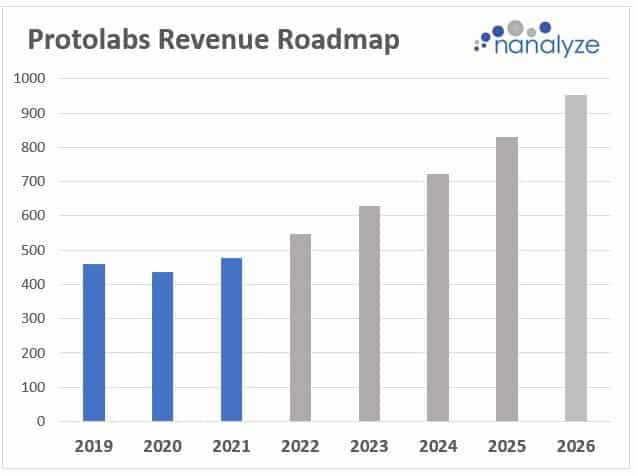

Multiple mentions are made of an internal Protolabs roadmap that expects revenues to double over the next five years. We’ve teased that projected growth out in the below chart which shows a revenue CAGR of 14.85% over the next five years.

If you have no dog in the race, and you’re looking to make a punt on distributed manufacturing, you might consider a company that’s growing at a faster pace – like Xometry.

Xometry Stock

When we look at quarterly revenue growth for both companies, it’s clear that Xometry is dominating.

In our last article on this topic, we talked about how “we’ll be keeping a close eye on Xometry going forward.” We also said that “we can expect Xometry to offer shares at a richer valuation than Protolabs.” When Xometry finally had their initial public offering (IPO), shares were moderately valued with a simple valuation ratio of 23 (3.87 / 0.168). Today, that valuation ratio has halved, sitting at around 11 (2.56 / 0.227) because of a falling share price and increasing quarterly revenues. The Xometry IPO was priced at $44 per share but closed at nearly twice that on the first day of trading. Today, shares are trading around the mid-50s.

We’re only given three years of historical revenues for Xometry, so we can examine quarterly growth instead which shows some consistency over time growing at a compound rate of 12.25%. If Xometry maintains that growth, they’ll hit just over $2 billion in revenues by 2026, more than double what Protolabs expects. We cannot justify ignoring this growth in hopes that Protolabs eventually comes out ahead.

Investing in Xometry and Protolabs

We’ve invested 3% of our capital allocated for tech stocks in Protolabs. We’re not committing any more because that’s our rule – establish a thesis and open a position where maximum capital committed = 1 / X where “X” is the number of positions in our portfolio. We’re certainly not selling our Protolabs position because our thesis has not changed. We’re going to hope that management executes on their vision of doubling revenues, something that ought to help the languishing stock price.

This brings us to Xometry, a company we’ve been keeping an eye on. Now that the valuation has halved since we last checked, opening a position is just too tempting. We always say that people who use memes are poor communicators, but this sums up where we’re at.

Distributed manufacturing is a massive opportunity, no matter whose estimates you believe. If our investment in Protolabs underperforms over time, that would be a bad thing, but the opportunity costs of missing out on the growth of distributed manufacturing are even more concerning. Of the five distributed manufacturing stocks available, three are special purpose acquisition companies (SPACs) that aren’t on our radar.

| Company | Ticker | SPAC | SPAC Finalized |

| Protolabs | PRLB | No | |

| Shapeways | GLEO | Yes | Yes |

| Xometry | XMTR | No | |

| Fathom | ATMR | Yes | No |

| Fast Radius | ENNV | Yes | No |

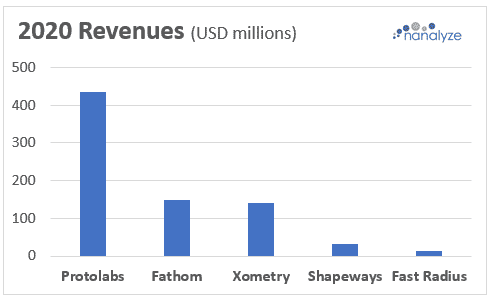

When it comes to revenues, Xometry and Protolabs are ahead. While Fathom and Xometry were head-to-head in 2020, the latter has pulled out in front with an estimated $211 million for 2021 vs. Fathom’s estimated 2021 revenues of $168 million.

We haven’t invested in a single SPAC yet after covering over 70, and Fathom won’t be the first. As for any new contenders coming out of the woodwork that may provide a formidable challenge to Protolabs and/or Xometry, there are some that still remain private, like Fictiv. But we’re confident that investing in the two leading distributed manufacturing companies today, Xometry and Protolabs, should provide sufficient coverage for this theme going forward.

Conclusion

While Protolabs stock may be flailing, their 2021 Investor Deck seems like management has a plan. Sure, they’re competing against Xometry, but there’s plenty of blue ocean for everyone. We can leave our Protolabs position as is. Regarding Xometry, we’ve now started accumulating. (Nanalyze Premium annual subscribers were alerted to this earlier.) The distributed manufacturing opportunity is so vast that we don’t mind having two position sizes’ worth of capital committed.

Share

Any updated opinion on IONQ ?

Probably not a relevant comment for this article but we’ll bite.

You mean the SPAC that that told investors to expect $5 million in revenues for 2021? Here’s how that’s going:

Q1 2021: $125,00

Q2 2021: $93,000

Q3 2021: $233,000

Yeah, avoid the company until they’re producing meaningful revenues as defined by $2.5 million in a single quarter.

Thanks, very much appreciated. As a recent subscriber I wasn’t sure where, how I post a question.

You are very welcome Robert. It’s you who deserves the thanks for supporting us financially. We’re always here to answer your questions.

We see a lot of meme stock types on Twitter pumping quantum stocks lately so be careful. Do not confuse price action with the quality of the underlying business.

In the future, you can search for a ticker using the magnifying glass icon in the upper-right corner of our homepage. Then you’ll be able to pull up articles about various stocks. Thanks again!

I am a new subscriber too, thanks for the sharing. Xometry looks good based on the qtrly growth as you highlighted.

Wonder if you can share its investor deck or powerpoint for me to do further research?

Hey James. Welcome to our closely-knit group of investors who pursue a risk-averse approach to tech investing. No hero-or-zero FOMO ape-into-the-latest-crypto-token stuff happening around here.

This is a good deck to check out: https://investors.xometry.com/static-files/8eee2200-58b1-45ac-8973-0c92ae5b7cac

Thank you for the financial support! Questions, feel free to email us or ask in the comments section as you did.