Bloom Energy Stock on Offer in a Planned IPO

Table of contents

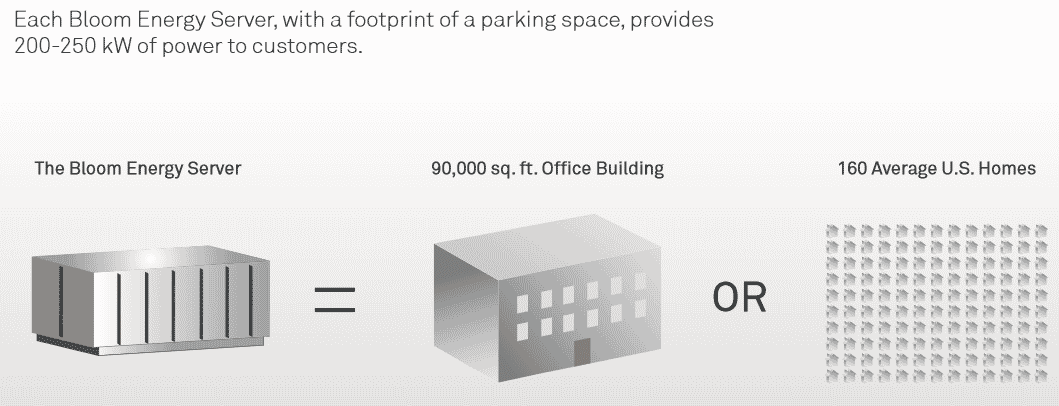

For whatever reason, people seem to be extremely interested in Bloom Energy’s value proposition – large scale fuel cells called “Bloom Energy Servers” that turn natural gas into electricity at a cheaper cost than market rates. While fuel cells are commonly thought of for use cases like propelling vehicles or powering smartphones, Bloom Energy appears to have successfully commercialized “30-foot shipping container sized fuel cells” that convert natural gas to electricity, enough to power a big box retailer:

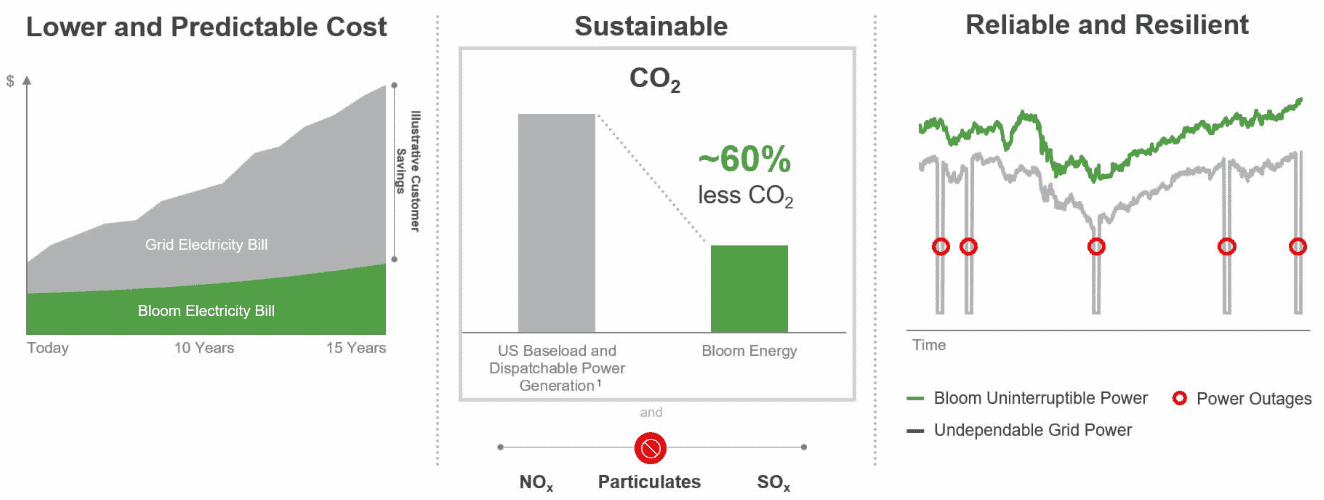

Generating electricity completely off the grid also resolves a lot of worries for the Business Continuity Planning (BCP) folks who previously needed to be concerned about backup electricity planning. (BCP people are responsible for making sure that when an earthquake goes off in San Francisco at the same time a typhoon happens in Manila, you can still service your customers.) Another benefit is that fuel cells are environmentally friendly, which means your marketing team can talk about how much you give back to the community.

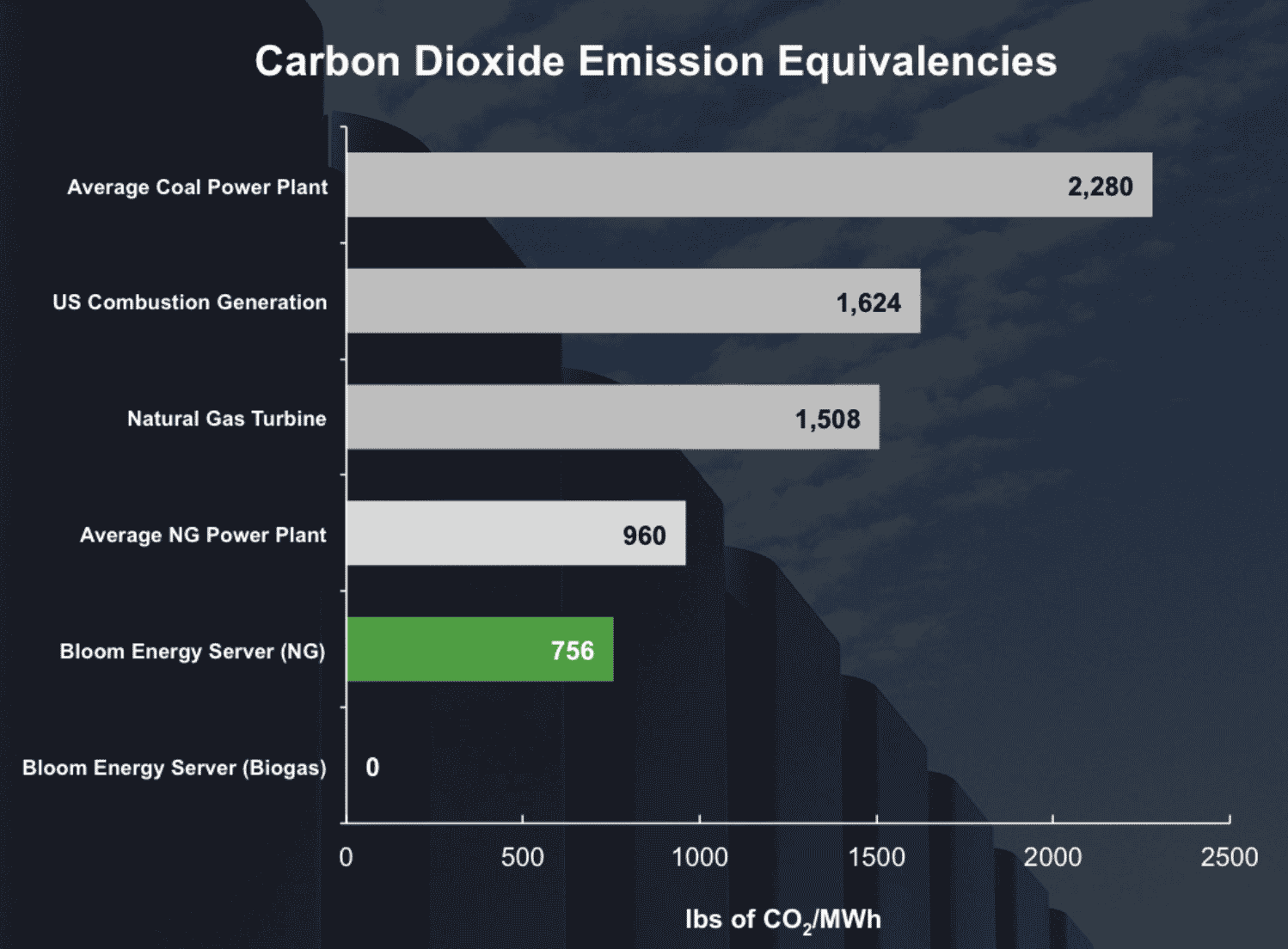

Fuel cells are different from batteries in that they require a continuous source of fuel and oxygen (usually from air) to sustain the chemical reaction that generates electricity, whereas in a battery, the chemical energy comes from chemicals already present in the battery. Fuel cells remain relevant for commercial and industrial use cases because they provide a cheap and eco-friendly power generation alternative to coal, oil, and gas combustion or nuclear methods. The technology is also more efficient, converting fuel with more than 60% efficiency compared to 32-43% for traditional approaches. In summary, Bloom’s value proposition is threefold:

Now, the Silicon Valley unicorn that wants to disrupt the energy market with their proprietary technology, has just filed for an IPO on the New York Stock Exchange, four years after rumors of its intention to go public.

About Bloom Energy

![]() Founded in 2001, Sunnyvale, California startup Bloom Energy has raised $1.6 billion from investors like Goldman Sachs, Credit Suisse, and energy giant E.ON to develop their solid oxide fuel cell technology. Unlike other fuel cells, no precious metals, corrosive acids, or molten components are required in their manufacturing process. The cells are powered by natural gas or biogas and come in scalable modules, assembled to cover a client’s required energy output.

Founded in 2001, Sunnyvale, California startup Bloom Energy has raised $1.6 billion from investors like Goldman Sachs, Credit Suisse, and energy giant E.ON to develop their solid oxide fuel cell technology. Unlike other fuel cells, no precious metals, corrosive acids, or molten components are required in their manufacturing process. The cells are powered by natural gas or biogas and come in scalable modules, assembled to cover a client’s required energy output.

These so-called Bloom Energy Servers are deployed at the client’s location and cost less than grid electricity because they shave off the cost of grid maintenance and the transmission and distribution of electricity. After installing their fuel cells to partially cover electricity consumption, IKEA in Connecticut saw energy costs fall by half. The system has integrated batteries as well, solving the common issue of energy storage and helping to smooth the load curve during peak demand. When used with natural gas, it produces 60% less carbon emissions than combustion-based power generation in the US, and with biogas this falls to zero (about 9% of their installed Energy Servers use biogas). Clients can opt to buy the hardware outright, or go for an energy service contract financed by partner institutions like Bank of America or Wells Fargo. Regarding the number of Energy Servers being adopted regardless of the purchase method, the company refers to these as “acceptances” and states “the number of product acceptances achieved in 2017 was 622 systems, a decrease of 9.5% as compared to 687 acceptances for 2016.”

The value proposition must be compelling because since their first commercial installation back in 2003, Bloom Energy has now installed Energy Servers with a total output of more than 312 megawatts for clients like Google, NASA, Softbank, Coca-Cola, Walmart, and the list goes on. 312 megawatts is roughly the equivalent of 115 wind turbines, or the annual consumption of 172,500 households in the European Union. Bloom’s customer base includes 25 of the Fortune 100 companies as of March 31, 2018.

Bloom Energy Financials

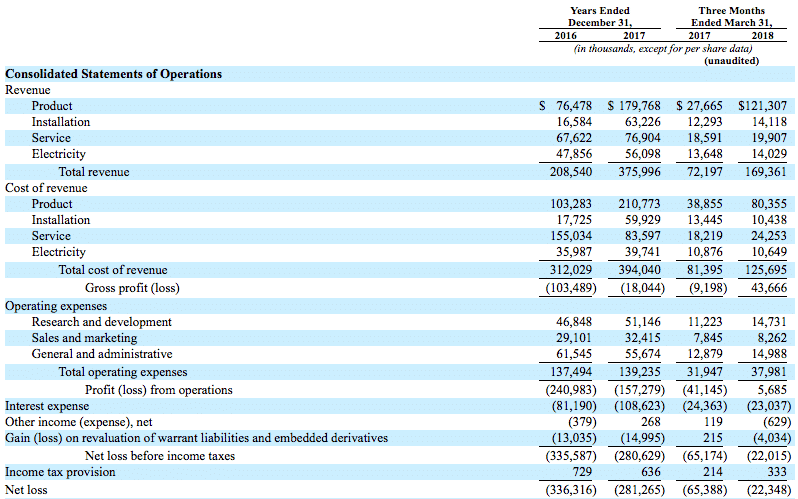

As a result of all that selling, the company’s revenues have grown +135% year-on-year to 2017 and in addition to that, the company has been very successful in Q1 2018, earning 67% of the full 2017 revenue in just one quarter.

This spike in revenues can be attributed to the US government reinstating tax credits for fuel cells just this February which is a key point to make here. Bloom was in a world of hurt when the tax credits expired in 2016. Here’s a statement they made in the the S-1 filing:

In order to offset the negative economic impact of that lost benefit to our customers and financing partners, in 2017, we lowered our selling price to customers. Because many customers or financing partners would monetize the tax credit upfront, the actual impact to our selling price was generally greater than 30%.

What this means is that if the tax credit expires again (it’s expected to expire in 2022), it will need to be renewed else Bloom will need to discount the price of their energy servers in a similar fashion. Bloom can counter this of course by steadily decreasing the cost of their revenue generating line items and growing their margins, which they have been successful in doing so far, achieving a $43.6 million gross profit in Q1 2018 for the first time. They still need to work on cost of their services as it’s creating negative margin, but Bloom is working on increasing the lifespan of their products to achieve profitability in this subcategory as well.

Bloom has significant interest expenses as well, since their total consolidated debt as of the close of Q1 2018 was around $950 million which will require them to dedicate a substantial portion of their cash flow to interest and principal repayment. $250 million of this debt will convert automatically to Class B common stock after a successful IPO, but the remaining portion will limit their growth, financing options, and profitability going forward.

The company is planning to maintain its technology leadership by increasing their fuel cell efficiency (which is already high at 65%), and driving down production costs. Lower costs will open up new markets and increase the spend of current clients, according to Bloom. Their SEC filing doesn’t outline how they are planning to use the proceeds of a successful IPO, so they could use part of the proceeds to decrease indebtedness and balance their financing which is the single riskiest factor in Bloom’s short-term future. A long-term risk factor is the US government tax credits for fuel cell implementation, which were recently reinstated and which have a planned expiration date of 2022.

Bloom Energy Economics

Recently we wrote about the effect that the cost of electricity has on the profitability of mining bitcoin. In that article, we talked about how electricity prices around the world vary, and the same is true within the United States. While the average American pays 12 cents a kilowatt hour for electricity, the number ranges from 8 cents in states like Idaho (lots of cheap hydroelectric power) to 33 cents in states like Hawaii where crude oil generates electricity. That’s all based on findings published in 2011 by NPR which show this breakdown across states, and it also happens to coincide with the same year these statements were made by Greentech Media regarding the economics of Bloom Energy Servers:

Bloom claims its “server” generates power for 7 cents to 10 cents per kilowatt-hour after incentives, a calculation that includes fuel, maintenance, hardware expenses and, most importantly, government incentives. Sometimes the cost is even lower. Adobe installed 12 Bloom Boxes and produces power for 8.5 cents per kilowatt hour — and it uses more expensive biogas. Adobe traditionally has to pay PG&E 13 cents a kilowatt hour at its headquarters.

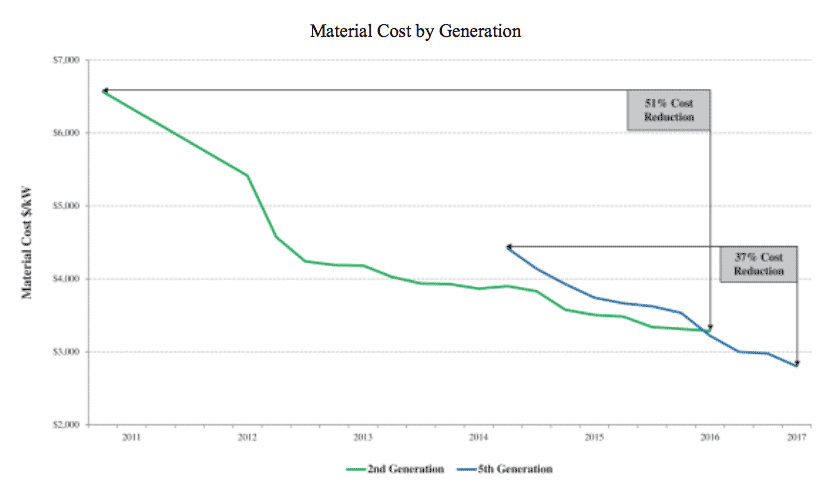

While seven years have passed since those numbers were published, it still gives us a good idea of what a benchmark might look like. We would expect those numbers to be lower based on increased efficiency and lower costs. Bloom has managed to drive down materials cost of their Energy Servers by 75% since 2009. In regard to efficiency, the current generation Energy Server is 14% to 31% more efficient than natural gas power plants. As efficiency increases and costs fall, Bloom Energy’s potential market will grow over time, especially internationally. Regarding international expansion, Bloom states:

Today, we have installations or purchase orders in the United States, Japan, India, and South Korea, and we are actively targeting additional international markets such as Ireland and Great Britain.

Conclusion

Government tax credits for fuel cells will most certainly push growth in the US market, and their efforts to cut production costs and increase fuel cell efficiency will assist international expansion. Besides the pressing issue of debt, Bloom Energy has a strong value proposition combining the highest fuel efficiency on the market with low costs and attractive energy-as-a-service financing options.

Update 05/20/2020: Fuel cell stocks have performed poorly at the beginning of their hype cycle back in 2015, and it doesn’t seem like the technology has taken off yet. In February 2020, Forbes published a lengthy investigative piece on Bloom titled “How Bloom Energy Blew Through Billions Promising Cheap, Green Tech That Falls Short,” which claims the technology is “too dirty and too costly.” This is partly because solar and wind energy are so cheap now. Niche use cases like fuel cells for urban air mobility keep popping up but providers like Bloom Energy face a tough market for widespread adoption.

Share