How Much Solar Exposure is there in Tesla Stock?

Table of contents

Solar is in a peculiar position right now. While it’s an incredibly promising segment of the energy sector, short-term outlook is clouded by oversupply, dropping margins and a grim 2017 with governments axing installation incentives and the US withdrawing from the Paris Agreement. These circumstances have caused investment sentiment to turn bearish in Q4 2016 and market perception hasn’t changed since. This concerns us because we’ve been invested in the Guggenheim Solar ETF (NYSEARCA:TAN) for about 5 years now and these are the sort of rubbish returns we’ve realized:

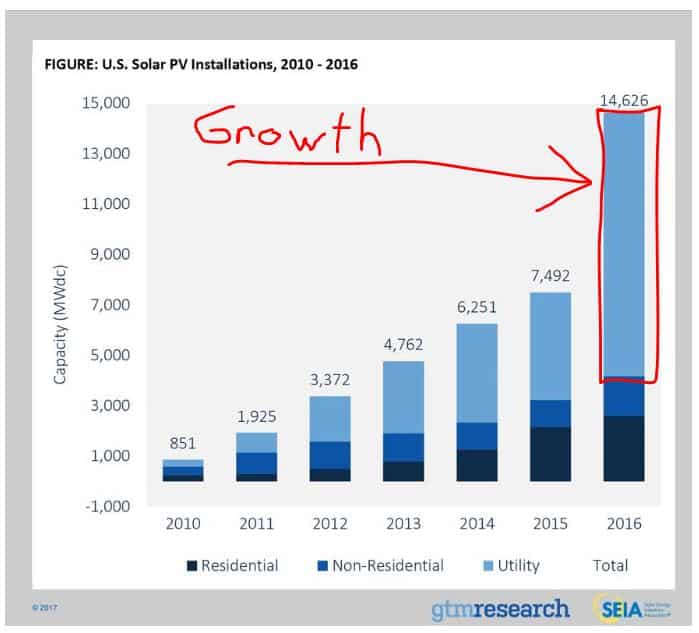

So if we would have held a relatively safe Nasdaq ETF over the past 5 years we would have realized returns of+117%. If you’re like us and you made a diversified investment in solar with TAN hoping that it would outperform the market over the past 5 years, then you would have had your arse handed to you with a measly +6.84% return. That is ridiculous when you look at how much solar has grown over the same time frame:

Needless to say, we’ve come to the realization that investing in solar using a diversified ETF isn’t working for some of the reasons we pointed out before. This made us think that somewhere out there is a viable investment to be made in solar. Elon Musk, our current go-to person for global vision, seems to have found one. He pushed through a merger between Tesla (NASDAQ:TSLA) and SolarCity and is fully committed to capitalize on the synergies between solar, his power storage solutions and electric vehicles. He’s even leaving his US governmental advisory roles after Mr. Trump’s administration announced the exit from the Paris Treaty to underline his commitment to sustainable energy so now he should have 2 hours a month more to work on “making solar great”. As investors, we want to know just how much solar exposure we get from investing in shares of TSLA. Let’s take a closer look at what exactly SolarCity is, and how it fits in the Tesla portfolio.

About SolarCity

![]()

SolarCity is admittedly the #1 full-service solar provider in the US. They provide a turnkey solution from reviewing and optimizing customer energy usage, through arranging permissions and installation, to system maintenance. Serving residential, commercial and utility companies, SolarCity’s services are scalable to a high degree.

The company was established in 2006 by Musk, who says it is a “mere accident of history” that became a separate company to Tesla. He was chairman and largest shareholder of both companies, with SolarCity managed by his cousins, Lyndon and Peter Rive. The $2.6 billion merger happened on 21 November 2016, days after Tesla shareholders gave their approval and consequently SolarCity Corp stopped trading as NASDAQ:SCTY and is now listed under TSLA as a subsidiary.

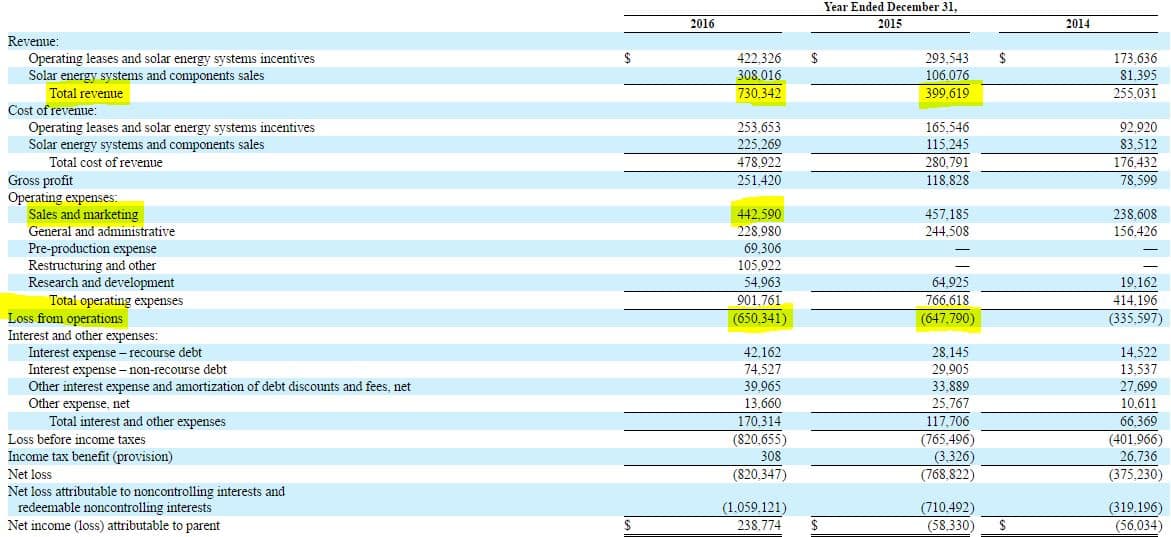

If we look at the last 10-K filed by SolarCity, we see that their revenue grew by +55% to $730.3 million in 2016 which means they’re selling lots of solar installations which is expected. Of course if you spend $422 million on Sales and Marketing alone, that sort of growth is expected along with a very steep loss from operations of $650 million (about the same amount they lost in 2015):

With a leading 25-33% of residential market share in the U.S. (depending on who you ask), SolarCity buys their solar panels and inverters directly from multiple manufacturers, all of which are being pressured by the plummeting cost of solar. They then take that solar equipment and either lease it, sell it for cash, or sell it with financing. For homeowners, this presents a very good deal since as of today, the IRS allows a taxpayer to “claim a credit for a residential solar energy system that is owned by the homeowner” in the amount of 30%. This also applies to commercial solar installations and even if you finance them through SolarCity (which is probably why SolarCity is issuing “solar bonds” left and right). It’s also probably why Elon Musk became a little bit irate when President Trump didn’t play ball on the Paris Agreement because that could hint that these subsidies may be in question as well. We’re not trying to be political in any way, but wouldn’t you want to stay on this guy’s good side with that hanging over your head? For now, this big fat discount is available until the end of 2019, after which it declines to 10% for commercial in 2022 and straight up expires for residential in 2022. Let’s hope that doesn’t change.

Now let’s consider SolarCity in the context of Tesla. This makes operations more complicated compared to simply transferring ownership, but also allows for more potential synergies with other Tesla products. We imagine Tesla is going for a subscription based solution in the mid-to-long term, where customers can pick elements of the product portfolio and set up a payment plan. How cool would it be to just ring your local sales rep and get a monthly rental bill for your car and power equipment while you get the bottom line reduced by feeding the extra power you generated in the grid? Plus you won’t pay for your electricity consumption or fuel ever again. This is where the real synergies will come from.

To top this off, Tesla has just launched the next generation of solar roofing tiles, which will be stylish as well as durable, and Musk plans to sell them cheaper than normal roofing tiles without electricity gains taken into account. A typical Musk venture – he came up with a solution which is better quality than the original, added significant technology advancement and now planning to sell it cheaper in absolute terms. Who’d go for the traditional version after that? These will fit in the Tesla product portfolio seamlessly where every product is so far ahead of its competition that basically it has its own league. At least that’s the story we’re being told, but it has yet to be executed upon such that your neighborhood starts to look this cool:

Let’s hope that chimney is a natural gas fireplace. The financial press has been voicing skeptical opinions regarding the merger, with markets noncommittal after the day it happened (Tesla’s share price was largely unchanged). There are valid arguments voiced on the side of caution: both component companies are still posting bottom line losses annually because of high sales, marketing and admin costs according to their respective annual reports. SolarCity is deeply in debt which is becoming harder to refinance because it’s owning and renting a large part of its solar assets – this is another reason why Tesla stepped in. On top of this, Tesla has to integrate SolarCity after a relatively recent restructuring and do so quickly to be able to deal with the Model 3 car launch and further development of Autopilot this year. Despite all these challenges, investors are looking favorably at TSLA with a +58.6% return over the past 12 months as seen below:

It is interesting to see that all criticism is touching on potential short-term issues, while long-term vision, market position and potential is never questioned. So the big question we originally started by asking was just how much exposure do we get to solar by investing in shares of Tesla?

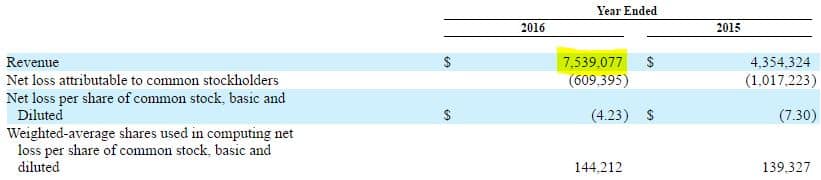

Tesla provided their total revenues for 2016 as if they acquired SolarCity on January 1, 2015 (these are referred to as “pro-forma” statements).

These “pro-forma revenues” came in at $7.54 billion while the actual revenue for Tesla in 2016 came in at $7 billion on the dot. Back of the napkin math puts SolarCity’s revenue contributions to Tesla in 2016 at around 7.7%. With the solar segment being far from profitable, it’s hard to think that the acquisition will have a positive effect on the bottom line (for now that is). Let’s hope Mr. Musk has plenty of MBAs on hand to identify all those synergies.

The Tesla acquisition of SolarCity is definitely in line with the vision of sustainable transport that Tesla represents, not to mention the certain synergies to be realized. On the other hand, we’ve also pointed out some additional risks that have cropped up recently for solar that Elon Musk is keenly aware of. Provided the subsidies stay in place, and with a careful focus on debt-to-equity and refinancing deals, Tesla should have every opportunity to make solar a much bigger piece of their pie.

Share