Are the Biggest Robo Advisors the Best?

Table of contents

The United States may be called the “land of opportunity”, but most of its citizens seem to take that for granted. If you are lucky enough to live in a country where you have the means to make a decent salary, you should make hay while the sun shines because those nice salaries may very well be going the way of the robot. We’ve all heard the “69% of Americans have less than $1,000 in savings” statistic, but that means very little if everyone they polled flips burgers at Mickey D’s (a job that is also going to the robots). That’s where charts like this one come in handy:

So almost 30% of people who make $150,000 or more a year have no savings? Priorities people. If you make 6-figures and you’re not driving a used Toyota that’s paid off, there’s your first problem.

Of course, saving money is just half the battle. The next difficult part is figuring out how to invest the money you save. We are constantly being asked by our readers about which stocks we believe are the best ways to play particular themes. Our answer is always the same. Before you even think about trying to “find the next Microsoft“, you first need to make sure the majority of your investment dollars are in, diversified, low-fee investment products. While our core strategy is “dividend growth investing“, most people will not want to manage their own portfolios. Some individuals will go engage the services of an investment advisor who will use a software tool to determine “optimal asset class allocation“. This advisor will charge fees, and the products you’re asked to invest in charge fees.

As we discussed before in an article called “The Truth About Robo Advisors“, the software tools used by investment advisors have now been externalized and given the name “robo advisor”. A robo-advisory service like Betterment charges a reasonable fee to invest your dollars across some of the lowest-fee assets out there. We feel very confident in recommending Betterment to everyone who wants a low-risk way of investing their savings (though more sophisticated investors may be better off using Motif Investing). Since we last touched on this topic, robo advisors have been sprouting up like weeds. Take a look at this market map from our clever friends over at CB Insights:

There are invariably all kinds of gimmicks innovations that are probably being used to differentiate all of the above robo advisors, and while some of these may have some actual merit, we’re going to stick with the age old adage – “follow the money”. In the world of finance, we refer to this as “AUM” which means “assets under management” which means “how much money have people entrusted to this firm to invest for them”. Here’s a look at the biggest robo advisors today by AUM:

In the era of fake news, you need to validate everything with at least a few sources. We spot checked the above numbers and they seem to be roughly inline with reality, and the reality is this. Vanguard is kicking the isht out of everyone else when it comes to AUM. Why is that? It’s probably because of the name they’ve built for themselves in the industry as one of the lowest-fee providers of ETFs there is. Generally across the ETF industry, there has been a “race to the bottom” by ETF providers to offer the lowest fees possible. We can see that from the below table of the 10 biggest ETFs as of February 2017 (of which Vanguard runs four):

Understanding why fees are plummeting is pretty simple. It’s something we call “economies of scale” which is why Walmart can charge such low prices. The more AUM that these ETFs amass, the lower fees they can charge. The lower the fees they charge, the better value they offer investors. Common sense tells us that the low-fee, high-volume robo advisors are where we’ll get the most bang for our buck.

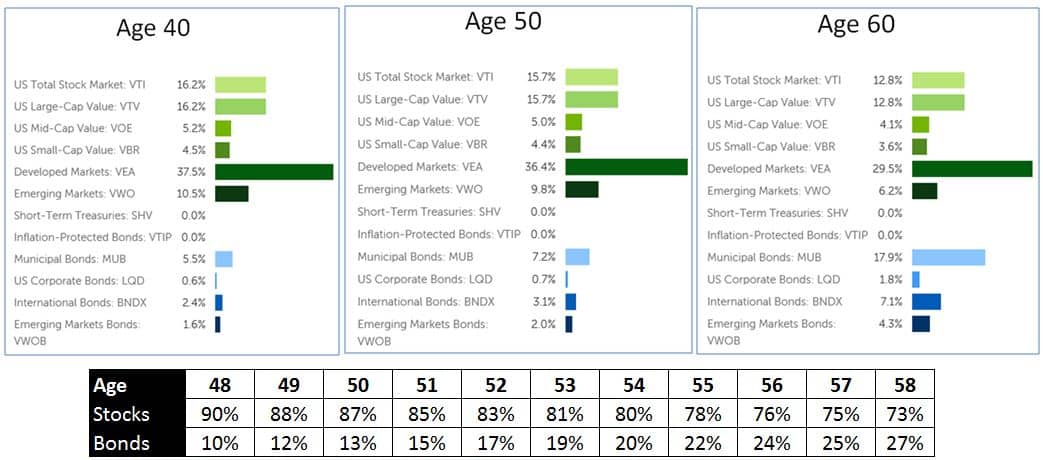

As we talked about before, these robo advisors basically just allocate your assets across a broad range of ETFs and then adjust these “asset class allocations” as you grow older. The below is an example of this allocation method provided by Betterment:

Of the above 12 ETFs listed above that Betterment uses, 8 are provided by Vanguard. As robo advisors started gaining in popularity, Vanguard thought to themselves, why not cut out the middle man person here and just offer a robo advisor ourselves? That’s exactly what they did, except that they set a required minimum of $50,000. At those amounts they could then offer their product as “Vanguard Personal Advisory Services” which focuses on the personal interactions you’ll have with people like these:

Notice how they avoid associating themselves with the term “robo advisor”. So for .30% (compared to Betterment’s .20%) you get a human to talk to in order to make you feel more comfortable. Since the industry average for talking to humans is 1.02%, you’re getting a pretty good deal. Betterment countered this by offering up someone to talk to once a year if you come to the table with $100,000 or more. Of course, then, fees go up to .40%. If you want to talk to someone as much as you like, it’s .50%. (You can talk to us here at Nanalyze as much as you like and we’ll charge you just .05%. And we have MBAs.)

For those of us who don’t have $50,000 burning a hole in our wallets for Vanguard’s “Personal Advisory Services”, the next offering on our list is Schwab with their “Intelligent Portfolios“. With an account minimum of $5,000, Schwab is offering “no fees” which may seem puzzling. How can you offer no fees to manage people’s money?

The answer is probably because Schwab is one of the largest banks in the United States and also one of the largest brokerage firms. Once you can get someone to open a brokerage account, banking account, or robo advisory account, you can easily cross-sell them all your product offerings. It would be interesting to know how much AUM in these intelligent portfolios came from people who were already clients of Schwab. The other thing to note here is that Schwab uses their own ETFs (or they get a commission on third party ETFs) with average fees being fairly high:

Based on data as of December 2015, the average OER for Schwab Intelligent Portfolios ETFs in all asset classes is 0.27%. This compares to an average OER of 0.41% for all ETFs in similar Morningstar categories (a difference of 0.14%).

We already know that most people don’t have $50,000 in savings laying around, or even $5,000. Most people want to get started with $750 from their tax return and then contribute $50 a month going forward. That’s where Betterment comes in.

With Betterment, there is no minimum account balance and no minimum required to open an account. If you’re one of those people who is just now thinking about starting to save, you cannot go wrong with Betterment. There are other providers as we go down the list, like Wealthfront, but they came into the picture 3 years after Betterment and have taken in a lot less funding. While there is room for all in the “robo advisor space”, Betterment appears to now have more than $9 billion in AUM having blown past Wealthfront who used to be the leader.

It turns out that Wealthfront has had some growing pains as described in this November 2016 article by Investopedia titled “Why Wealthfront Replaced Its CEO“. That article talks about how “one of the reasons why Wealthfront has fallen behind its original rival Betterment is because Betterment also serves financial advisors in addition to retail customers“.

So, are the biggest robo advisors the best? Based on the old adage of “following the money”, it appears that they are. If you have $50,000 or more to invest, then Vanguard seems to make sense. If you have $5,000 or more to invest, and you’re happy with being cross-sold banking products, go with Schwab. If you just want a basic robo advisor with no minimums, tax loss harvesting, and some of the lowest-fee ETFs around, go with Betterment.

Conclusion

As for all you Americans who make 6 figures and can’t manage to save any of it, here’s what you should do. Go into the office tomorrow morning and ask your local HR representative what fees your retirement plan charges you. The HR person will look at you like you just asked them to prove Einstein’s theory of relativity, so go back to your desk and figure it out yourself. We can almost guarantee you that the fees you’re being charged are exorbitant. That means that whenever you can, get that isht rolled over to Betterment. If your plan is locked, don’t wait until you get fired because the robots took your job. Open a Betterment account now and start contributing $100 a month to it. No excuses. In less than a year, you’ll be one less person who falls into the sad statistic of having less than $1,000 in savings.

Share