Why Has the Guggenheim Solar ETF (TAN) Underperformed?

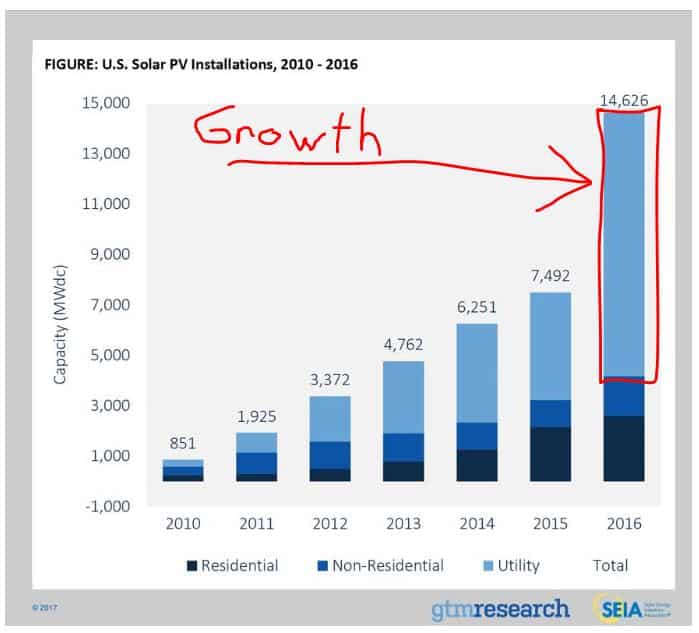

In a recent article, we were raving about the incredible growth of the US solar industry over the past year. With a +95% growth in installations mainly driven by photovoltaics (PV), last year was truly record-breaking for solar energy. For those of you unfamiliar with the term, PV is what usually comes to mind when thinking about solar power – panels that directly convert sunlight into electricity. If we add the rest of the world, global capacity growth still remains above a whopping +50% with the U.S. first and China second. The U.S. is clearly leading the growth charge as seen below:

Given the fact we’ve been invested in the Guggenheim Solar ETF (NYSEARCA:TAN) for the past 5 years, we happily started eyeing yacht catalogs and booking trips to over-priced all-inclusive resorts in the Bahamas. Checking on our investments though, we found TAN had a dismal -26% performance. Now, before we start chastising ourselves for making such poor investment decisions, we need to know how the overall market performed. It’s actually way worse than we originally thought:

- If we held a NASDAQ tracker ETF for the las