3 Things to Note About Nanoco

Table of contents

![]()

In a previous article published in July, we highlighted Nanoco (LON:NANO), a pure-play publicly traded company for investors looking for exposure to the quantum dot story. Since our last article, Nanoco has made several significant announcements and released their preliminary results just several weeks ago.

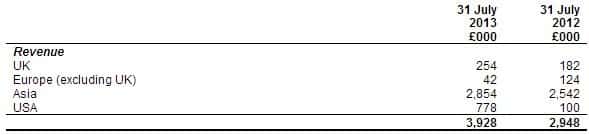

Mid-Year Revenue Analysis

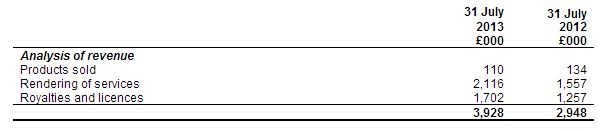

Revenue for the first 6 months of the year increased by 33% to $6.3 million USD compared to the same period in 2012. Included within this revenue was $1 million USD from Dow Chemical earned under the license agreement signed in January 2013. A breakdown of Nanoco’s 2013 revenues so far this year can be seen below in British pounds:

Included within the “rendering of services” revenue category is revenue from two material customers amounting to £1,573,000. Included within “royalties and licences” is revenue from two material customers amounting to £1,702,000.

Increased Production Capacity

Nanoco has completed the expansion of its quantum dot production facility with the installation of two Semi-Tech lines at a planned cost of approximately $2 million USD. The company also announced that the terms of its global licensing agreement with DOW have been amended to waive the requirement for Nanoco to contribute capital to the production plant Dow is preparing to build in Asia. In return, the royalty rate that Nanoco would receive from Dow’s sale of quantum dots has been reduced.

Recent Fund Raising

As of the end of 2012, Nanoco had around $16 million USD cash available. In the preliminary results issued on October 14, management stated that based on forecasts made up to 31 December 2014 the company would not need to raise equity finance. These forecasts assumed that Dow received a customer commitment, commissioned its production facility and would be able to start shipping CFQD material in the first half of 2014. Management stated that in the event that there were delays in a customer commitment or in the commissioning of Dow’s new production facility or no customer commitment was achieved, the Group would either find cost or capital savings or would need to raise equity finance. Just a day after these statements were released along with the preliminary results, Nanoco announced the closing of a $16 million share placement. Based on the prior statements made, it could be assumed that there have been delays in Dow securing a customer commitment and/or delays in commissioning the new production facility.

On the other hand, in a October 14th article published by Investor’s Chronicle, Nanoco’s chief executive, Michael Edelman, is quoted as saying Nanoco expects their first commercial contract – probably with the big Korean TV manufacturers – “soon”. In this same article, Liberum Capital expects Nanoco to achieve a $5.6 million pre-tax profit in 2015. Liberium also expects LED lighting projects, high-tech solar film and cancer imaging are also likely to make big contributions further down the line. Nanoco has a joint development agreement with Osram, one of the world’s largest lighting companies, and an agreement with Tokyo Electron for the on-going development of a printable, nanomaterial-based solar film. Nanoco recently announced achieving a solar cell efficiency of 12-13% nearing the 15% mark which is deemed commercially viable. Nanoco is stated by Investor’s Chronicle to be currently a “speculative buy”.

Share