Is Infineon Better than Wolfspeed for EV Chip Exposure?

We recently released our revamped Nanalyze Disruptive Tech Report that is only available to annual subscribers. It is now leaner but meatier, grouped by technology themes under each of the 12 tech categories – like Electric Vehicles under Green Technology. In theory, that should make it easier for retail investors to find succinct analyses on their favorite tech themes. This works pretty well when we cover pure-play stocks but can get a bit messier when we consider pick-and-shovel plays on a theme.

An example that is especially pertinent to today’s article is a company we recently covered – Wolfspeed (WOLF). The Durham, North Carolina company specializes in manufacturing semiconductors using silicon carbide (SiC), a material especially suited for applications that require higher efficiency and power density chips such as electric vehicles (EVs). Wolfspeed sounds like a company we would normally cover under Computing or Artificial Intelligence, yet our interest in WOLF stock is actually as a green tech stock. Huh?

Investing in EV Chips

The writing is on the roadway: Electric vehicles are the future, even if that road is a little bumpy right now, especially after Tesla (TSLA) just announced it would cut 10% of its workforce amid slumping sales. Its biggest competitor, China’s BYD (1211.HK), is in some ways a more compelling long-term investment in the EV theme, with added exposure to emerging markets and the world’s second largest economy. While both of these EV companies are compelling, there’s also another angle to take here – chips. We’re in the midst of investigating a pick-and-shovel play on electric vehicles by investing in EV chips.

These components are essential to EVs, as well as modern autos, especially a type of chip known as a power semiconductor. Power chips are specialized integrated circuits designed to handle high voltages and large currents, making them suitable for power electronics applications such as home appliances, automobiles, and industrial machinery. Materials like SiC and gallium nitride (GaN) are seen as the future of power semiconductors because they offer better performance, higher efficiency, and higher power density compared to silicon. This is particularly the case in green tech markets like EVs and renewable energy systems.

Hence our interest in Wolfspeed, which indeed represents significant exposure to EV chips, as well as an emerging material technology like silicon carbide. The downside is that management has been consistently missing guidance and burning huge piles of cash trying to ramp up production at its spiffy new silicon carbide factory in New Yawk. That’s had a knock-on effect across gross margins and other key indicators of financial health, which we do not see improving any time soon.

About Infineon Stock

So we’re moving on to Infineon Technologies (IFX.DE), a $43.5 billion German company that also specializes in manufacturing power semiconductors to meet demand in green energy sectors like electric cars, charging stations, and renewable energy systems. And, like Wolfspeed, Infineon is rapidly scaling production to capture more of the SiC market. Is Infineon stock the best bet for EV chips?

To answer that question, we need to understand a bit more about the company and how it generates revenue.

A brief history of Infineon Stock

Until 1999, Infineon was a subsidiary of Siemens AG, the German technology conglomerate with a history that dates back to the 1840s. Its founders – including, of course, a guy named Siemens – commercialized a new type of telegraph and never looked back. Name a decade and Siemens was likely involved in the latest and greatest technology at the time, from electric streetlights and electric tramways to electrical components for Nazi death camps to washing machines and pacemakers. And, of course, computer hardware, including a short-lived venture in the 1970s with Advanced Micro Devices (AMD).

Management reportedly decided to spin off Siemens Semiconductors because of the heavy volatility and losses that the division had suffered in 1998, despite posting $3.8 billion in sales – back when a billion dollars was worth something. It was reportedly the largest high-tech spin-off in European history at the time. The new company, Infineon, IPO’d in 2000 during the same year when the dot-com bubble peaked. Whatever happened during the succeeding years is lost in the mists of time, so in the interest of time, let’s fast forward to recent revenue history:

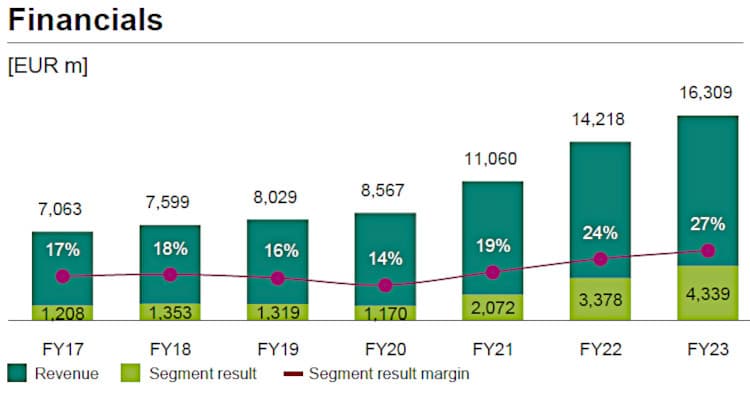

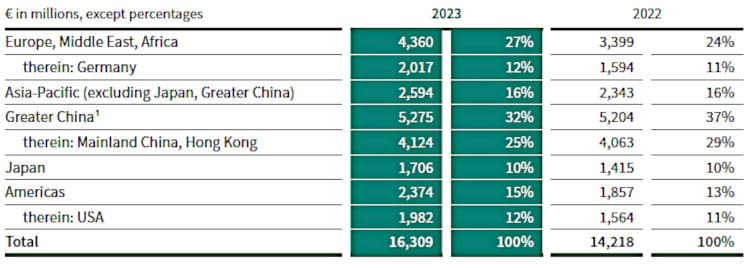

A couple of things to note: Numbers are in euros, so last year the company had revenues of about $17.3 billion in U.S. greenbacks. (We’ll be quoting U.S. dollars throughout but the charts are in euros.) The percentage represents the increase in net profit (called segment result), not revenue growth, which was about 15% between 2022 and 2023. (Infineon management noted that global semiconductor sales over the same period are estimated to have shrunk by around 13%.) While Infineon profiles more as a value stock – such as being profitable and a steadily increasing dividend over the last decade – the recent revenue surge suggests the company has hit another gear.

How Does Infineon Make Money?

While history is fun, we’re mainly here to learn more about how the sausage is made – how does modern-day Infineon generate revenue. Being German, management has made that job pretty easy for us by methodically breaking revenue down into four segments and then into the four main products within those revenue segments.

We immediately see that automotive accounts for more than half of the company’s revenues. Sliced and diced by product category, power semiconductors account for 55% of revenues. To understand the big picture, let’s briefly introduce each of the segments:

- Automotive: Infineon claims to be the market leader in automotive semiconductors (more on that shortly). Its products and solutions cover powertrain, energy management, connectivity, infotainment, safety, and data security.

- Green Industrial Power: Formerly called Industrial Power Control, this segment reflects the company’s hard pivot to green industries like renewable energy. Power semiconductors dominate here, especially based on SiC technology. Applications include inverters for renewable energy systems, industrial power supplies, and EV charging infrastructure.

- Power & Sensor Systems: This segment also focuses on power semiconductors, along with radio frequency (RF) and sensors, for various applications like power supplies, lighting systems, mobile devices, and renewable energy solutions.

- Connected Secure Systems: As the name implies, this segment is focused on Internet of Things (IoT) solutions for ensuring secure connectivity for smart home appliances, IT equipment, consumer electronics, and more.

Market Leader and Expanding Markets

We generally only invest in market leaders, and we find that Infineon owns about 14% of the automotive semiconductor market. That’s good enough to qualify as the leader in a market valued at more than $69 billion in 2023, according to research by TechInsights. The company is also the lead manufacturer of power semiconductors at more than 20% of that market.

As a major manufacturer of a key technology for enabling not only electrification of vehicles but the energy grid, Infineon certainly checks the pick-and-shovel box for EVs and other green technologies. The sizable exposure to IoT is an added bonus. Last year, Infineon acquired a Swiss startup, 3db Access, to boost the company’s capabilities in energy-efficient ultra-wideband (UWB) technology. UWB tech can be used to precisely determine positions and distances while protecting against signal interference. IoT applications include secure access to vehicles and buildings, indoor navigation, and presence detection of people in rooms.

Other future revenue growth drivers include artificial intelligence (of course) and data centers. Infineon acquired a small Swedish startup, Imagimob, for its platform to enable machine learning solutions for IoT edge devices. Applications include audio event detection, voice control, gesture recognition, predictive maintenance, signal classification, and material detection.

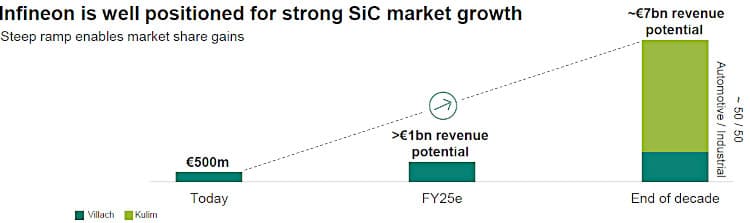

Infineon Targets 30% SiC Market Share

We’re also looking for exposure to new chip materials like SiC and GaN. Infineon receives another big checkmark, as the company announced just last year a major investment of up to about $5 billion at its manufacturing facilities in Kulim, Malaysia. That follows a roughly $2 billion commitment in 2022. Combined with the conversion of existing SiC manufacturing lines at the company’s factory in Villach, Austria, Infineon believes it can capture 30% of the SiC market by the end of the decade. In 2023 alone, the company grew silicon carbide revenue by 65% to more than $500 million.

Competing with Infineon for the title of the world’s largest SiC semiconductor factory using 200-millimeter manufacturing technology is Wolfspeed. The latter recently announced plans to build a facility in Infineon’s home turf of Germany, even while struggling to ramp up production at its new fab factory in Mohawk Valley, New Yawk. Despite the rivalry, the two companies are also business partners: Earlier this year, they announced plans to expand and extend an existing supply agreement in which Wolfspeed provides base silicon carbide material to Infineon.

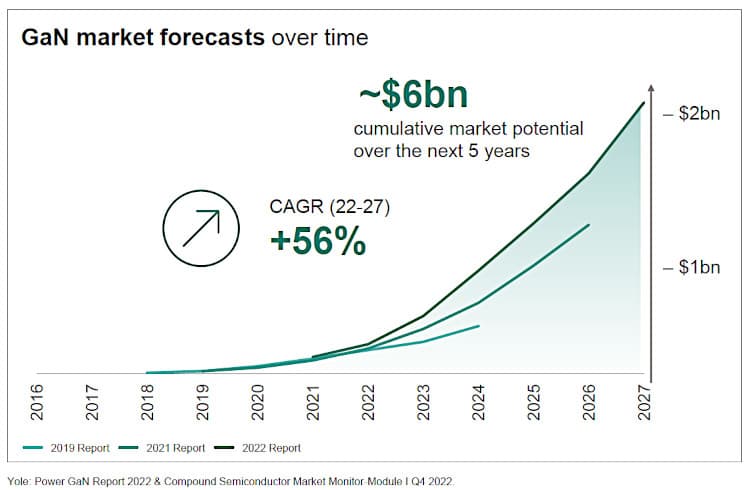

In addition to SiC, Infineon is also focusing on gallium nitride for power semiconductors, particularly for applications with higher switching frequencies, such as mobile charging, power supplies for data centers, solar inverters for private households, and onboard chargers for electric vehicles. Toward that end, Infineon acquired a third startup in 2023, GaN Systems, for $830 million to add the Canadian company’s technical expertise into its portfolio.

Infineon Stock: One Big Red Flag

Infineon stock: What’s not to love, right? The company offers exposure to both EVs and conventional vehicles, diversifying risk as countries make the shift to decarbonize their economies. More broadly, it is a pick-and-shovel play on green technologies. Infineon also provides exposure to both IoT and AI, particularly in the area of edge computing. In addition, revenues are geographically dispersed, with a healthy amount coming from China. For example, Infineon earns between $500 and $1,300 per car from its Chinese customers across more than 10 different models.

Regular readers of Nanalyze know that no company we review is perfect – and that includes Infineon. We found one red flag, the original sin of Nanalyze’s simple rules of investing. Infineon is guiding to zero revenue growth in 2024. Worse: At the revised midpoint forecast, revenue will potentially decrease 2% this year compared to last year. In its 2023 year-end wrap-up, management had guided to about $18 billion +/- $500 million but downgraded its estimate to roughly $17 billion +/- $500 million in Q1-2024. Gross and net margins are also expected to dip. Management blames half the decline in the forecast revenue on the euro-to-dollar exchange rate. The other half appears to be related to the usual macroeconomic headwinds – soft demand amid excess inventories.

One reason we would drop a stock is if revenue stalled for a prolonged period of time. In this case, we it’s hard to consider going long any disruptive growth stock that’s seeing stalling revenue growth. Based on EV sale trends and the current state of renewable energy – SolarEdge, a key customer in the Kulim factory expansion, is floundering badly – seems like 2024 is probably going to be a wash for Infineon.

Conclusion

We found a lot to like about Infineon stock. However, we would need to dig even deeper if we decided that it represents the best bet on EV chip technology. Mainly, that involves examining other EV chip stocks on our short list. Sporting a low simple valuation ratio (market cap/annualized revenue) of less than 3, Infineon stock should remain a bargain bin buy for the foreseeable future, so there is no rush to grab it now. Famous last words.