Challenges Ahead for Twist Bioscience Stock

There’s always a delicate balance between being too hands on with a stock and not paying close enough attention to how its business evolves. Revenue growth is the one metric that cuts through all the noise and distills it down to what’s most important for a disruptive technology stock. Is a company able to monetize their technology and capture market share in a large total addressable market (TAM)?

In addition to monitoring revenue growth, it’s good to have an elevator pitch that quickly articulates your bull thesis. For example, Twist Bioscience Corporation (TWST) is a company that produces synthetic DNA strands on demand for their clients. The need for this service has expanded significantly with the emergence of synthetic biology. Therefore, Twist Bioscience is a pick-and-shovel play on synthetic biology tools that should grow along with the entire synbio industry. Indeed, we see this to be the case over time.

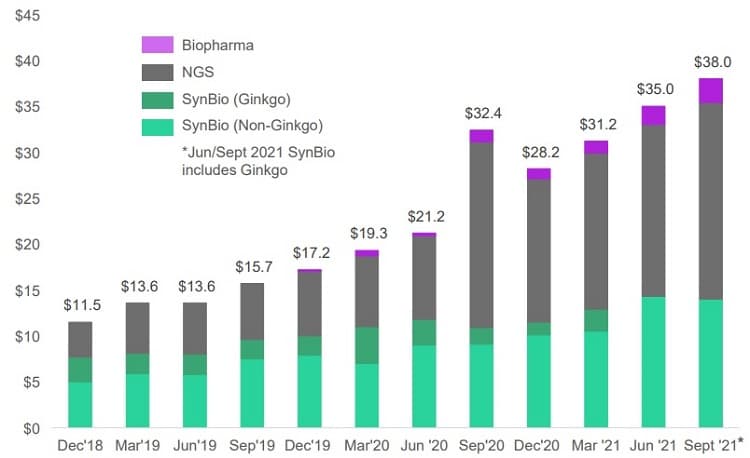

Aside from showing consistent quarterly revenue growth over the past three years, this chart contains other useful insights. Notice how they recently stopped breaking out revenues for Ginkgo Bioworks – one of their biggest customers – something that was useful to know. They’ve also removed any mention of Ginkgo Bioworks being a key customer in their SEC filings, and don’t even mention that as a risk factor anymore per their recently filed 10-K. Here’s what they do tell us:

- No major customer accounted for 10% or more of our revenue for the fiscal year ended September 30, 2021.

- There were two major customers who accounted for 12% and 10% of our revenue for the fiscal year ended September 30, 2020.

- There was one major customer who accounted for 17% of our revenue for the financial year ended September 30, 2019.

From these bullet points, we can deduce that Ginkgo’s business is decreasing as a percentage of Twist Bioscience’s total revenues which is great (reduced customer concentration risk). But why are SynBio revenues growing much slower than NGS revenues? Here are the compound annual growth rates (CAGRs) for each of Twist’s defined revenue segments over the past several years – synthetic genes, oligo pools, DNA and biopharma libraries, and next-generation sequencing (NGS) tools.

As it turns out, creating synthetic DNA isn’t nearly in demand as much as creating NGS tools which Twist sells through a direct sales team focused on the NGS tools market which is entirely separate from their synthetic DNA sales force. Twist attributes the growth of their NGS tools segment to emerging use cases such as population-scale sequencing, liquid biopsies, minimal residual disease testing, and single-cell sequencing. Here’s how Twist explains it:

- A significant constraint in many NGS applications has been the high cost and long turnaround time of oligonucleotide production.

- Highly accurate and reproducible oligonucleotide production is required to produce high-quality target enrichment data.

- The ability of the Twist DNA synthesis platform to precisely manufacture target enrichment probes at large scale has dramatically increased the types of projects that can now be addressed using NGS technologies.

So, it all comes down to the value of oligonucleotide production. (Oligonucleotides are short DNA or RNA molecules, oligomers, that have a wide range of applications in genetic testing, research, and forensics.) If you’re a firm that’s performing lots of genetic sequencing work, you’ll find Twist’s platform to be a critical part of your workflow. Unless of course you use any of the other firms offering similar sample preparation services for NGS such as Thermo Fisher Scientific, Illumina, Integrated DNA Technologies, Agilent, or Roche NimbleGen. In other words, Twist is competing against some very established companies and spending a ton of money to do so, particularly on the sales side.

While revenue growth proves Twist’s platform is capturing market share in the various segments they’re dabbling in, we have some concerns around their business model taking a services approach as opposed to a hardware product/consumables approach.

Products vs. Services

In a recent piece on proteomics player SomaLogic, we described our preference for companies that sell life sciences platforms to customers who then provide recurring revenues in the form of consumables – the old razor and blades model. As a services company, Twist can only scale their platform in a linear fashion. They need to worry about their capacity meeting the demands of their clients who are also restricted by the need to invoke a service. The answer could be the benchtop DNA printer that’s now on offer from a firm called DNA Script.

We first came across DNA Script back in 2018 when we wrote about 9 DNA Data Storage Companies to Watch and more recently in last year’s piece on 7 Companies Doing DNA Synthesis for Medical R&D. Instead of using traditional methods of DNA synthesis that were developed in the 1980s, DNA Script employed first principles thinking and turned towards nature for the answer (something referred to as biomimetics). The company engineered enzymes to naturally perform DNA synthesis faster, cheaper, and more environmentally friendly than existing methods of writing DNA like those used by Twist. More importantly, they’ve packaged the whole thing in a benchtop machine that’s clearly being marketed as a replacement to the services being offered by Twist Bioscience and others of their ilk.

Illumina (ILMN) knows a thing or two about what’s unfolding having backed both Twist Bioscience and DNA Script. In a blog post last year, Illumina talks about how Twist relies on “a capital-intensive and centralized model using traditional phosphoramidite chemistry,” while DNA Script uses “very efficient enzymes called polymerases” which perform DNA synthesis at the speed of nature. It’s something we wrote about in a piece titled DNA Script Develops World’s First Enzymatic DNA Printer, also noting that there are others working on desktop instruments for DNA synthesis. Regarding the new approach using enzymes, Twist Bioscience says the following:

If, in the future, enzymatic synthesis proves commercially scalable, we have the ability to include this chemistry within our established commercial infrastructure.

Credit: Twist Bioscience

So will every other company out there that decides to pony up the money for a benchtop instrument that can do the work in house.

UPDATE 01/18/2022: Last week Twist Bioscience unveiled their own novel approach to synthesize strands of DNA enzymatically which was developed over the past 18 months. They also announced they’ll be enabling NGS workflows for PacBio and Singular Genomics. Maybe next they’ll get into bed with the market leader in NGS tools – Illumina.

DNA Script has now raised nearly $480 million in funding, $200 million of which was a Series C that closed just weeks ago. They’re using that money to scale as quickly as possible, and an exit could be in the cards before the IPO mania music stops. If that happens, we’ll be keen to look under the kimono and see if a stock swap might be in order.

Investing in Twist Bioscience Stock

We’re presently holding a very small position in Twist Bioscience that’s now fallen below our cost basis. Should the price of shares continue to fall, then this would be when we typically add to any position we’re holding. However, our thesis for Twist Bioscience has evolved a bit from when we first established it as a pure-play on the growth of synthetic biology. If Twist is becoming more of a play on the growth of NGS, then we already have similar exposure with our Illumina position – one of the largest positions we’re holding at the moment. While Twist appears to be firing on all cylinders when it comes to revenue growth, they’re also facing what appears to be a formidable threat from the likes of DNA Script.

The latest Twist Bioscience investor deck shows 2022 revenue guidance between $173-$181 million. That number could jump about $10 million more if they close the acquisition of Abveris, a firm that applies proprietary antibody discovery technologies and techniques to build platforms to quickly develop diverse panels of antibodies. Twist also spun out a company, Revelar Biotherapeutics, and both these corporate events telegraph expansion beyond their core DNA synthesis capabilities.

With almost $480 million in cash on their books, Twist can survive at least a few more years of heavy losses before needing to raise capital which will result in shareholder dilution or increased debt.

For now, we’re leaving our Twist Bioscience position as a placeholder so we can keep track of what happens in this space. Our biggest concern surrounds Twist’s services business model which we believe could be displaced by a hardware business model such as the one on offer from DNA Script.

Conclusion

With a limited number of available slots in our tech stock portfolio, we want to have strong convictions for every stock we’re holding. Twist Bioscience doesn’t appear to be showing signs of weakness, but we’re growing increasingly nervous about how the DNA Script benchtop instrument might put pressure on their services business model. Or maybe the blue ocean TAM is so large that both companies can thrive without stepping on each other’s toes.