AI Fintech Startups Offer Loans on New Credit

Table of contents

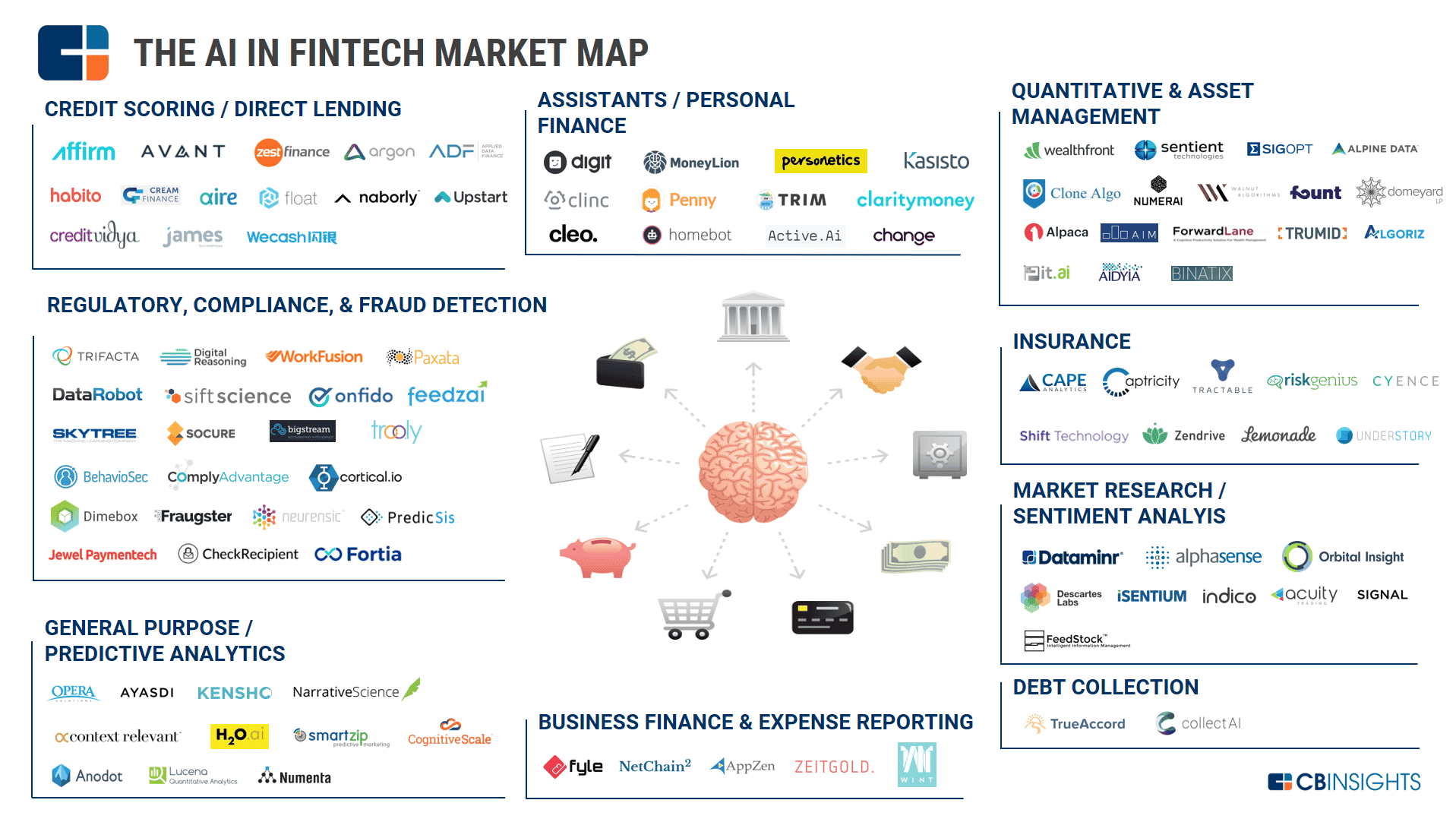

Last month we told you about a fintech startup called DemystData that uses reams of information from various sources—big data—to generate a different type of credit score for 21st century borrowing. It’s a new wrinkle in the digital lender landscape that’s currently led by companies like Lending Club and Prosper. We also said it was only a matter of time before someone decides to insert a little artificial intelligence into the equation. Apparently we’re well past that time: We’ve found more than a dozen AI fintech firms through our friends at CB Insights that claim their machine-learning algorithms can evaluate loan applications in milliseconds while minimizing defaults.

Many of these companies target so-called thin-file borrowers—people with little credit history—who are usually trying to consolidate debt from high-interest credit cards. Think millennials looking to dig themselves out of student loan and credit card debt while financing a $150-a-week cold-pressed coffee habit. Weddings and home improvement projects are among the other top reasons why people borrow money online. (Based on our experience, we can only assume divorce is No. 4 on the list.)

While fintech has been a hot category in recent years, 2016 was something of a downer in terms of venture capital dollars in play. CB Insights reported in its 2016 Global Fintech report that investments dropped from an all-time high of $14.6 billion in 2015 to $12.7 billion last year. Online loan companies, in particular, took something of a hit in 2016. That was largely thanks to an accounting scandal that rocked Lending Club, which eventually led to the resignation of founder and CEO Renaud Laplanche in May. S&P Global Market Intelligence reported that loan originations for the industry’s top six personal loan digital lenders dropped about 9 percent from 2015 to 2016. The last quarter was particularly tough, with a 31 percent tumble in loan originations. (However, overall, the top online loan sharks companies tracked by S&P Global Market Intelligence improved their bottom-dollar on loan originations by 15 percent from year-to-year, mostly on the backs of small businesses and students. It’s the American way. See the chart below.)

An AI Fintech Unicorn

![]() Leading the AI fintech pack is a certified unicorn named Avant, founded only five years ago and valued at $2 billion. Total equity funding to the Chicago-based startup is more than $650 million, with the last round a robust $325 million Series E led by General Atlantic during the 2015 boom year for fintech. Other investors have included RRE Ventures, Tiger Global, August Capital and billionaire Peter Thiel, a particularly savvy tech investor. Avant has also tapped into hundreds of millions of dollars in debt financing to power its business, bringing total funding to $1.78 billion.

Leading the AI fintech pack is a certified unicorn named Avant, founded only five years ago and valued at $2 billion. Total equity funding to the Chicago-based startup is more than $650 million, with the last round a robust $325 million Series E led by General Atlantic during the 2015 boom year for fintech. Other investors have included RRE Ventures, Tiger Global, August Capital and billionaire Peter Thiel, a particularly savvy tech investor. Avant has also tapped into hundreds of millions of dollars in debt financing to power its business, bringing total funding to $1.78 billion.

Avant offers direct unsecured personal loans ranging from $1,000-$35,000 with funding delivered as soon as the next business day. It has served more than 500,000 customers worldwide, though last year’s downturn for digital lenders also hit Avant. Its year-to-year loan originations were down 12 percent to about $1.7 billion.

So, what differentiates Avant and other AI fintech startups from “simple” big-data companies like DemystData? Well, in the case of Avant, its machine-learning platform reportedly considers 10,000 variables and learns how to predict default rates. That allows the company to price loans appropriately.

As Avant’s director of engineering, Gabe Lerner, told the website Built in Chicago: “Our main advantage is how quickly we’re able to adapt to the market. When there are changes, like an oil crisis, we’re able to deploy our models and retrain them in a matter of days or weeks, which is faster than a lot of our competition.” The company also employs its AI algorithms for fraud detection by analyzing transactional data, such as how much time applicants actually read contracts or look at pricing options, according to Built in Chicago. It also searches metadata in files submitted for a loan application. That accumulation of data helps pinpoint outliers and minimize risk.

Avant is reportedly expanding its business model by offering its platform to brick-and-mortar banks interested in growing their online lending business.

A Zest for AI Fintech

![]() That’s pretty much what ZestFinance is already doing. The Los Angeles-based startup uses the same mix of big data and machine learning to help lenders make better (i.e., less risky and more lucrative) underwriting decisions. Led by a bevy of former Google-ites, including former Google CIO and ZestFinance CEO and founder Douglass Merrill, ZestFinance has raised $62 million in equity financing, including an undisclosed amount last July. Total funding is $262 million thanks to a couple of additional rounds of debt financing. Peter Thiel’s name again appears on the long list of investors.

That’s pretty much what ZestFinance is already doing. The Los Angeles-based startup uses the same mix of big data and machine learning to help lenders make better (i.e., less risky and more lucrative) underwriting decisions. Led by a bevy of former Google-ites, including former Google CIO and ZestFinance CEO and founder Douglass Merrill, ZestFinance has raised $62 million in equity financing, including an undisclosed amount last July. Total funding is $262 million thanks to a couple of additional rounds of debt financing. Peter Thiel’s name again appears on the long list of investors.

Just last month it rolled out its Zest Automated Machine Learning (ZAML) platform. ZAML can analyze vast amounts of a lender’s in-house data and combine that traditional credit information with a number of other variables similar to Avant. The company recently partnered with Baidu, a Chinese language Internet search provider, to turn Baidu’s search, location and payment data into credit scores.

AI Fintech in China and India

The ability of these AI fintech startups to turn nontraditional data available online into a credit score is particularly appealing to countries like China and India where hundreds of millions of people not only don’t have access to clean air but no ability to get deeply into debt. In India, engineers at a startup called CreditVidya hopes to turn $2 million in funding from a Series A last year into a viable system to provide credit scores for up to 800 million of its fellow citizens. Meanwhile, in China, startup WeCash has a lot more cash on hand after an $80 million Series C this month brought total financing to about $107 million for the three-year-old company. WeCash mines public mobile data from about 600 million mobile internet users and three minutes later assesses a customer’s credit risk.

Shop ‘til You Drop with AI Fintech

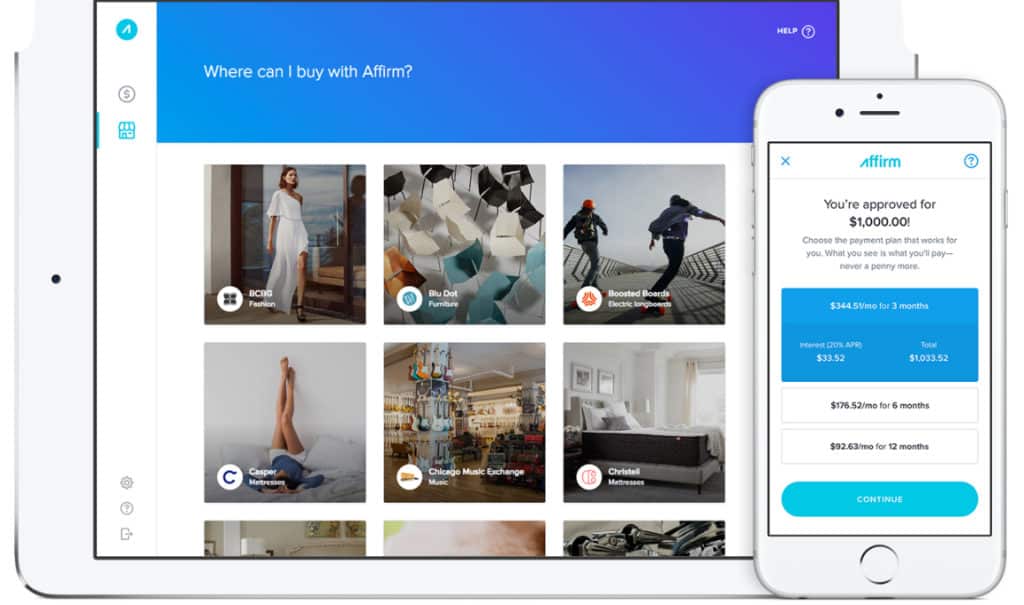

![]() San Francisco-based Affirm plays with a different model in helping the consumer economy go around. Some of you of a certain generation would call it a mobile version of a layaway plan. Key VC tech investors like Andreessen Horowitz and Khosla Ventures have helped pour $320 million of equity into Affirm, bringing total funding to $420 million after a $100 million round of debt financing from Morgan Stanley. The company is led by PayPal co-founder Max Levchin.

San Francisco-based Affirm plays with a different model in helping the consumer economy go around. Some of you of a certain generation would call it a mobile version of a layaway plan. Key VC tech investors like Andreessen Horowitz and Khosla Ventures have helped pour $320 million of equity into Affirm, bringing total funding to $420 million after a $100 million round of debt financing from Morgan Stanley. The company is led by PayPal co-founder Max Levchin.

Need to buy that $1, 000 futon online but all of your credit cards are, shall we say, maxed out? Simply check out at participating merchants using Affirm, which provides instant financing options using big data and machine learning. It assumes all the risk. Affirm claims vendors will see average order value increase by 75 percent. Customers include companies like Expedia and Motorola.

Update 09/17/2020: Affirm has raised $500 million in Series G funding to advance their mission to build honest financial products that improve lives. This brings the company’s total funding to $1.5 billion to date.

AI Fintech for Peer-to-Peer Lending

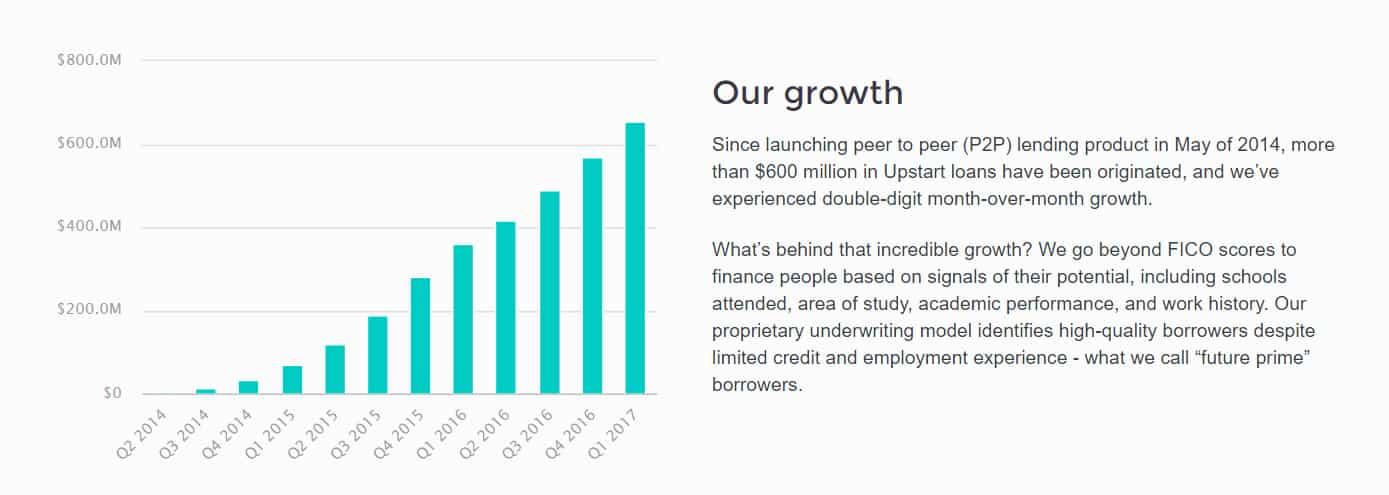

![]() We’ll round out this group of AI fintech startups with UpStart, if only because trillionaire wannabe Mark Cuban is among its investors. The Silicon Valley company has raised $85.65 million, and is probably still counting the crisp bills from its $32.5M Series D last month. Upstart is an AI fintech version of Lending Club. Meaning it provides peer-to-peer lending. Like ZestFinance, it particularly markets to the skinny jeans crowd, offering loans of up to $50,000 to help consolidate debt, pay off student loans and build credit history for those living in hipster cities like Portland and Brooklyn. The machine learning bit involves taking less tangible variables like education, college major and astrological sign into account. (Tip: Never lend money to a Cancer.)

We’ll round out this group of AI fintech startups with UpStart, if only because trillionaire wannabe Mark Cuban is among its investors. The Silicon Valley company has raised $85.65 million, and is probably still counting the crisp bills from its $32.5M Series D last month. Upstart is an AI fintech version of Lending Club. Meaning it provides peer-to-peer lending. Like ZestFinance, it particularly markets to the skinny jeans crowd, offering loans of up to $50,000 to help consolidate debt, pay off student loans and build credit history for those living in hipster cities like Portland and Brooklyn. The machine learning bit involves taking less tangible variables like education, college major and astrological sign into account. (Tip: Never lend money to a Cancer.)

Investors have a couple of investing options here. One particularly interesting choice is to invest via a peer-to-peer lending retirement account. That allows you to enjoy the tax advantages of managing a self-directed IRA while also playing out fantasies of being a mafia don offering loans to overeducated, underemployed graduates just like in the Godfather movies. Upstart CEO (and former president of Google Enterprise) Dave Girouard told TechCrunch he expects his company to become profitable this year. He predicts Upstart will originate about $1 billion in loans this year after doing about $650 million in loans in its first 2½ years.

Conclusion

Is AI fintech ready to make the startup world of digital financing an offer it can’t refuse? There are some big names with some big-time financing behind many of these ventures. It’s still too early to see where this will lead, though the number of zeroes behind those dollar signs suggest this segment might be prime for some primetime exits someday. Other companies may find they’re just living on borrowed time (and money).

Share

Would be interesting to know how these companies report adverse actions to consumers based on machine learning algorithms.

So that’s a good question.

For Avant, we received the below for a rejected application:

If you would like a statement of specific reasons why your application was denied, please contact the Application Review Manager shown below within 60 days of the date of this letter. We will provide you with the statement of reasons within 30 days after receiving your request.

You have to actually pick up the phone and call someone in Chicago (or write them) so it’s not likely that many people would go to the trouble of doing that. We were told by Avant that they’re targeting higher credit scores so it’s pretty easy to just say your credit score wasn’t high enough.

Also note the below Stacy.

Just a bit more. The writer who filed for a loan and received a rejection is living outside the USA and received the additional rejection reason with a credit score of 781:

Key factors that adversely affected your credit score: “Lack of recent installment loan information, No recent non- mortgage balance information, No recent bank/national revolving balances, No recent revolving balances”

This is a person that works as an officer at a publicly traded firm, has zero debt, and has significant assets to back that loan. Clearly the AI algorithms aren’t that sharp.

It’s likely you would not get much more color than the above if you called or mailed them.

I assume machine learning would be random forests, SVMs, GBMs, etc., algorithms beyond logistic regression and a decision tree. I know overall variable importances can be obtained from some of these more advanced methods, but I do not see how the exact individual adverse attributes can be obtained from them. . Black box algorithmic methods do not appear to identify individual attributes. .

All good points. Ultimately the AI needs to improve the “underperforming loan” metric and optimize the risk versus return for each loan issued. If it’s not doing this, then it fails. In this case, the attributes that failed for this app could have been basic up-front checks before even getting to the AI algorithms.