Are You Better Off Investing with Betterment?

Table of contents

In a recent article titled “The Truth Behind the Rise of Robo-Advisors“, we talked about how a “robo-advisor” is only similar to a robot because it is automated. It does not use any sort of artificial intelligence (at the moment) which means the strategy itself is very similar to what a traditional wealth management advisor would offer. It’s really just the traditional wealth management offering at a lower price point and with lowered required minimums. The “low cost” aspect of the offering is particularly appealing to retail investors planning for retirement, because that low fee structure is most likely better than what they are currently paying for their retirement accounts. While we’ve talked about robo-advisory offerings in the context of large well-established wealth management firms, there are “robo-advisor” startups that are starting to steal assets under management (AUM) from traditional wealth management advisors. One of the largest, if not the largest robo-advisor startup at the moment is Betterment.

About Betterment

![]()

Founded in 2008, New York-based Betterment has taken in 5 rounds of funding totaling $105 million so far from firms like Citi, Bessemer Venture Partners, and Northwestern Mutual. The Company claims to have over $3 billion under management with +125,000 users which would mean an average investment portfolio size of around $24,000. While some of the reviews we’ve read on Betterment simply elaborate on all the marketing literature provided by the Company, we’re more interested in understanding their business model, investment methodology, and most importantly fees. What are they doing to earn their money?

Update 09/30/2021: Betterment has raised $160 million to accelerate growth across its core retail investment products and advisor solutions, and particularly its rapidly growing 401(k) offering for small and medium-sized businesses. This brings the company’s total funding to $435 million to date.

First, let’s talk about Betterment’s methodology which they say is “built on decades of Nobel-prize winning research“. One basic question to ask candidates in a finance interview is if they know the difference between an “active” money manager and a “passive” money manager. The difference is this. A passive manager simply tracks the performance of a benchmark like the S&P 500 while an active manager tries to beat the benchmark by overweighting or underweighting certain stocks, industries, or factors. Betterment uses a passive investment strategy that allocates your funds across fixed income and equity using a variety of ETFs. This means the process is almost completely objective. Like every single other wealth management strategy out there, it is indeed “built on decades of Nobel-prize winning research“, or as finance professionals would call it “modern portfolio theory“.

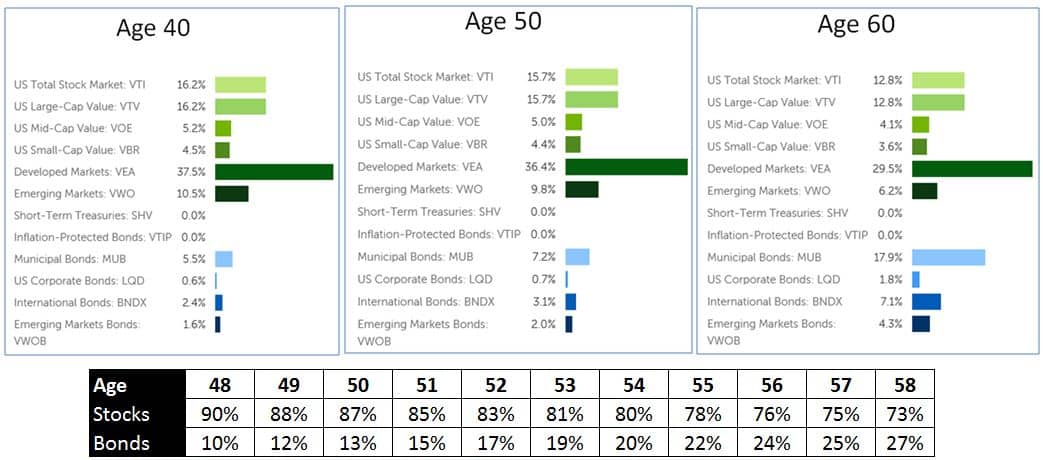

When you first look at the Betterment investment offerings, the only 3 things they want to know about you are your age, whether or not you are retired, and the amount of money you make per year. They then use this information to allocate your money across a basket of fixed income and equity ETFs. The amount of money you earn per year makes no difference to the allocations but is simply used to estimate how much money you might have when you retire. From age 18 to 48, the allocations don’t change but from 48 years old onwards the allocation percentages change every year. You can see how the allocations change based on your age:

So far this is a textbook wealth management strategy; as you age, your portfolio’s allocation to equities decreases and the allocation to fixed income increases. Nothing too special so far. So what fees are we paying for this strategy? Here are the fees for all the investment products (red text) in a sample Betterment portfolio along with Betterment’s fees (green text):

Many of the ETFs in this portfolio are from Vanguard who claims to have some of the lowest investment fees in the industry. The entire portfolio has very low fees, so the question becomes whether or not Betterment’s fees are reasonable. Why couldn’t we just replicate this strategy ourselves by buying this portfolio of ETFs? Using Motif Investing, we can buy up to 30 ETFs for the flat fee of $9.95 per trade and weight them as seen above. This means we’re paying a transaction cost of around 4 basis points to buy an average-sized Betterment portfolio of $24,000. We would have to pay an additional 4 basis points every time we want to rebalance the portfolio, perhaps once per year. We would also have to pay 4 basis points every time we sell some or all of our position. On the other hand, Betterment allows you to invest one time or a fixed amount per month with no fees ever. Betterment also allows you to withdraw your money at any time for no fees and they always sell your shares in a way that minimizes tax for you.

Conclusion

So are you better off investing in Betterment? We think so. The real value add behind Betterment is the fact that by using their product you are saving money, not only in fees, but in the fact that you are actually saving money. Americans, the people who make of the majority of our audience, don’t tend to invest much of their discretionary income. Betterment is selling an investment product with low fees, an objective “passive” methodology based on widely accepted principles of investing, and an automatic rebalancing function. Is charging 15/25/35 basis points for that platform acceptable? It is certainly a fair price, since if you have a very small amount to invest, you can get access to this platform by investing just $100 a month. If you have $100,000 to invest, then fees at 15 basis points seem reasonable and are certainly less than what you can expect from a traditional wealth management advisor.

Share

Given that the only input they want is your age/retirement date and all you are really getting here is a reallocation formula, I’d say you are better off just buying a Vanguard target date fund at 18bps? That is, if you buy into the idea of a gradual reallocation from equities to fixed income as the appropriate retirement investment strategy, which it is not (See Zvi Brodie’s work among others on this).

Thank you for the comment PAH. A Vanguard target date fund at 18 bps is cheaper no doubt but unless you’re going to be living off the eventual income stream, you’ll have to sell shares on a frequent basis when you retire which incurs transaction costs. Betterment doesn’t.

The gradual allocation from equity to fixed income seems primitive. I’ve read papers that claimed it was the single most important determiner of performance and then others like Brodie that say it’s all rubbish.

Personally, I think that a portfolio of +30 DGI stocks with appropriate sector allocation will outperform any FI/equity allocation strategy in the long run. “Dividends were responsible For 42% Of Stock Market Returns Since 1930” and similar statements make dividend paying stocks compelling. Try to see how well bond income stands up against inflation as opposed to a ~7% growth every year in your income stream with a well diversified DGI portfolio of stocks that have a track record of not only paying but increasing dividends for 25+ years.

Vanguard does not charge any transaction costs for the purchase or redemption of its target date funds. And I agree with you that gradual allocation from equities to fixed income is pretty basic. But that is what Betterment provides (based on your description and charts). My point was that if automatic reallocation and systematic saving is what you are looking for you don’t need to pay 15-35bps wrap fees to Betterment.

I’m not sure what DGI stocks have to do with whether Betterment is a good deal. But since you brought it up, I have not seen any hard research that shows dividend-paying stocks outperform the market (except perhaps to the degree that they tend to be value stocks, which have over some periods outperformed). Perhaps you can point to some. That said, I’m not against dividends but would remind folks to hold these stocks in tax deferred accounts.

Finally, to your last point, beating inflation is exactly what Brodie and others are focused on, which is why they recommend TIPS and i-Bonds as core retirement holdings. These will keep up with inflation, guaranteed, with zero expense.

Apologies for the delayed response PAH but I’m just seeing your comment now.

DGI stocks don’t have much to do with Betterment except that it’s one retirement strategy that focuses on an income stream that grows to beat inflation, not just keep up with it. I think you’ll find studies that support DGI as offering superior returns and ones that claim it’s based on survivorship bias. My personal retirement strategy is based on a portfolio of ~30 DGI stocks so I’m a bit biased in my views.

A basic asset allocation strategy is sufficient for most people who are planning for retirement. Whether they sacrifice some bps to Betterment or do their own asset class allocations, investors who actually save while paying minimal fees are on the right track.